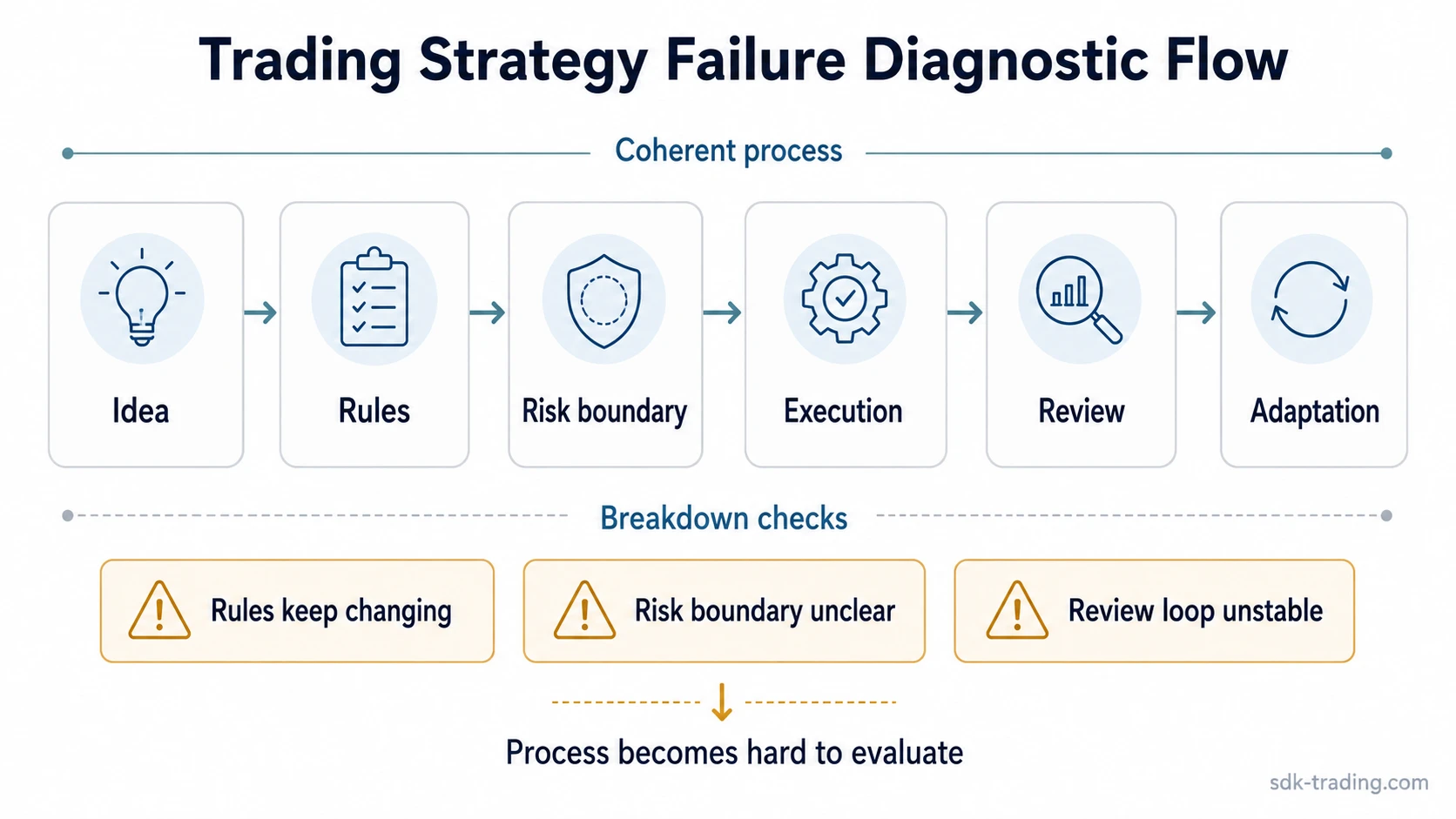

Trading strategies usually fail when the idea, rules, risk boundary, execution behavior, market conditions, and review criteria stop matching each other.

A losing trade does not automatically mean a strategy has failed. A trading strategy becomes fragile when it cannot be tested, repeated, reviewed, or adjusted without changing the rules after every result.

The failure often begins before any single trade is evaluated. A setup label, preferred indicator, market opinion, or performance goal may look like a strategy, but it does not become one until the conditions, risk boundary, execution behavior, and review criteria are stable enough to examine.

Key Points

- Trading strategies fail when rules, risk, execution, and review criteria lose alignment.

- A setup label is not a complete strategy unless it defines repeatable conditions and boundaries.

- Backtested rules can weaken in live conditions when friction, timing, liquidity, or behavior changes.

- Overfitting, regime change, and strategy switching can make results difficult to evaluate.

- A review process helps separate a temporary drawdown from a broken trading process.

Why Trading Strategies Fail

Trading strategies fail for different reasons, but the common thread is process incoherence. The idea may still sound logical, yet the rules may be vague, the risk boundary may be unstable, execution may drift, or market behavior may stop matching the original conditions.

A strategy also becomes difficult to judge when each result changes the method. If filters, holding time, risk size, and evaluation standards keep shifting, the trader is no longer reviewing one process. The method has become a moving target.

Definition: A failed trading strategy is not simply a strategy with losses. It is a trading process whose rules, risk assumptions, execution behavior, or review criteria no longer support repeatable evaluation.

When a Strategy Is Only a Setup Label

A setup label can describe a condition, but it does not define the whole strategy. “Breakout,” “pullback,” “mean reversion,” or “momentum” can identify a pattern family without explaining when the condition is valid, what would invalidate it, how risk is constrained, or how results will be reviewed.

The gap matters because many failures are blamed on the setup when the real issue is missing structure around the setup. A trader may say that a breakout strategy failed, while the actual process changed from trade to trade: different confirmation filters, different holding periods, different risk assumptions, and no stable review standard.

Stable evaluation requires a defined relationship between market condition, rule set, risk boundary, execution behavior, and review criteria. Without that relationship, results may reflect improvisation rather than the quality of the original idea.

Strategy Failure Conditions: Implication and Limitation

The most useful failure diagnosis is not a single cause list. It is a condition check that separates what the failure may imply from what it does not prove.

This condition, implication, and limitation frame keeps the diagnosis testable because each failure signal is paired with a boundary on what can be concluded from it.

| Condition | Possible implication | Limitation |

|---|---|---|

| Rules change after every short losing sequence | The process may no longer be stable enough to evaluate | A short weak period does not prove the original idea was invalid |

| The setup label is clear but risk boundaries are unclear | The strategy may be underdefined even if the chart condition is recognizable | Risk boundaries should be treated as process constraints, not as tactical advice |

| Backtest results look strong but live execution differs | The historical test may not reflect friction, delay, liquidity, or behavior under pressure | A weak live period does not automatically prove the backtest was useless |

| The market environment changes | The original rule set may no longer match current volatility, trend, liquidity, or participation conditions | Regime change is a review trigger, not proof that all similar strategies fail |

| Results depend on narrow historical conditions | The strategy may be overfit or too sensitive to one sample | Overfitting is one possible explanation, not the only reason a strategy weakens |

| The trader keeps adding filters after each failure | Complexity may be replacing a clean review process | More rules can improve structure only if they are defined before evaluation |

Why Backtests Can Fail in Live Conditions

A backtest can help examine historical rule behavior, but it is still a controlled reconstruction. Live conditions add friction, timing uncertainty, execution delay, changing liquidity, emotional pressure, and decisions that may not appear in the historical test.

The backtest/live gap becomes larger when the test was built around a narrow sample, excessive filters, or assumptions that are hard to reproduce. A strategy may appear durable in historical data because the rules were shaped around that data, not because the process is durable across different environments.

Backtesting weakness should be interpreted carefully. Historical testing does not prove future performance, but a poorly designed review process can still hide whether the strategy ever had repeatable logic.

Execution Drift, Risk Rules, and Review Criteria

Execution drift appears when the trader no longer follows the same process that the strategy was designed to evaluate. The entry condition may be similar, but the filter, time horizon, size relationship, or exit behavior may change under pressure.

Risk rules are part of the strategy structure because they define whether the method can survive enough observations to be reviewed. If risk expands when confidence rises and contracts only after losses, the strategy’s results may reflect reactionary behavior rather than the original rule set.

The evaluation standard keeps the process testable. It separates ordinary variation from structural failure by asking whether the same conditions are still present, whether execution followed the defined rules, and whether the risk boundary remained consistent.

Market Regime Change and Strategy Drift

A trading strategy can stop fitting the market when volatility, trend behavior, liquidity, correlation, or participation changes. A method designed for one environment may become less coherent when the surrounding conditions no longer resemble the environment where the rules were developed.

This is especially important when a strategy is tied to horizon and style. A process built around short holding periods may fail if it starts behaving like a longer-horizon method without changing its review criteria. A swing trading style also needs rules that fit its intermediate horizon rather than borrowing assumptions from scalping, day trading, or position trading.

Regime change does not mean a strategy must be abandoned immediately. It means the rules, assumptions, and review criteria need to be checked against the current environment before the same label is treated as the same process.

Common Mistakes That Make a Strategy Untestable

Many strategy failures become harder to diagnose because the process stops being testable before the trader notices. The result may look like a market problem, but the deeper issue is often unstable evaluation.

| Mistake | Why it creates failure risk |

|---|---|

| Changing filters after every small drawdown | The strategy never receives enough stable observations to evaluate |

| Treating a setup name as a full process | The label hides missing rules, risk boundaries, and review criteria |

| Trusting a narrow backtest too heavily | The rules may fit one historical sample better than a range of conditions |

| Ignoring execution friction | Live results can differ when spreads, delay, fills, and liquidity matter |

| Reviewing outcomes without checking rule compliance | The trader may blame the strategy for results produced by inconsistent behavior |

Example of a Basic Strategy Failure Reading

A trader uses the same setup label for several weeks, but the process changes after each short losing sequence. One week the trader adds a confirmation filter. The next week the holding period changes. Later, risk size changes before any stable review has been completed.

The problem is not only the setup. The rules are no longer stable enough to evaluate. A stronger review would separate three questions: whether the original market condition is still present, whether the defined process was actually followed, and whether the risk boundary remained consistent.

If those checks are missing, the trader may keep replacing the strategy before knowing whether the strategy failed, the market environment changed, or execution drift created the result.

How to Diagnose Strategy Failure Without Overcorrecting

A useful diagnosis starts with the process, not with the last result. It checks whether the strategy was applied as designed, whether the market condition still matches the rule set, and whether the risk boundary and review criteria were consistent enough to make the result meaningful.

Overcorrection creates a second problem. Adding new filters, changing horizons, or rewriting rules after every weak period may reduce discomfort, but it can also destroy the evidence needed to decide what actually failed.

Limitation: No diagnostic checklist can prove that a strategy will work later. The useful role of the review process is narrower: it helps separate a broken idea, mismatched conditions, weak risk structure, inconsistent execution, and normal performance variation.

FAQ

Why do trading strategies fail even after a good backtest?

A backtest can fail in live conditions when historical assumptions do not match friction, liquidity, execution timing, emotional pressure, or changing market behavior.

Does one losing trade mean a trading strategy failed?

No. One losing trade is not enough to diagnose strategy failure. The stronger question is whether the rules, risk boundary, execution behavior, and review process remained stable.

Can a trading strategy stop working because the market changes?

Yes. A strategy can become less coherent when volatility, trend behavior, liquidity, or participation changes enough that the original rule set no longer fits the environment.

Is overfitting the main reason trading strategies fail?

Overfitting is one common failure mode, especially when rules are shaped around a narrow sample. It is not the only cause; risk structure, execution drift, and review failure can also weaken a strategy.