Trading psychology is the behavioral layer of trading decisions. It covers the emotions, cognitive biases, discipline problems, and crowd-behavior pressures that can change how a trader reads market information and follows a process under pressure.

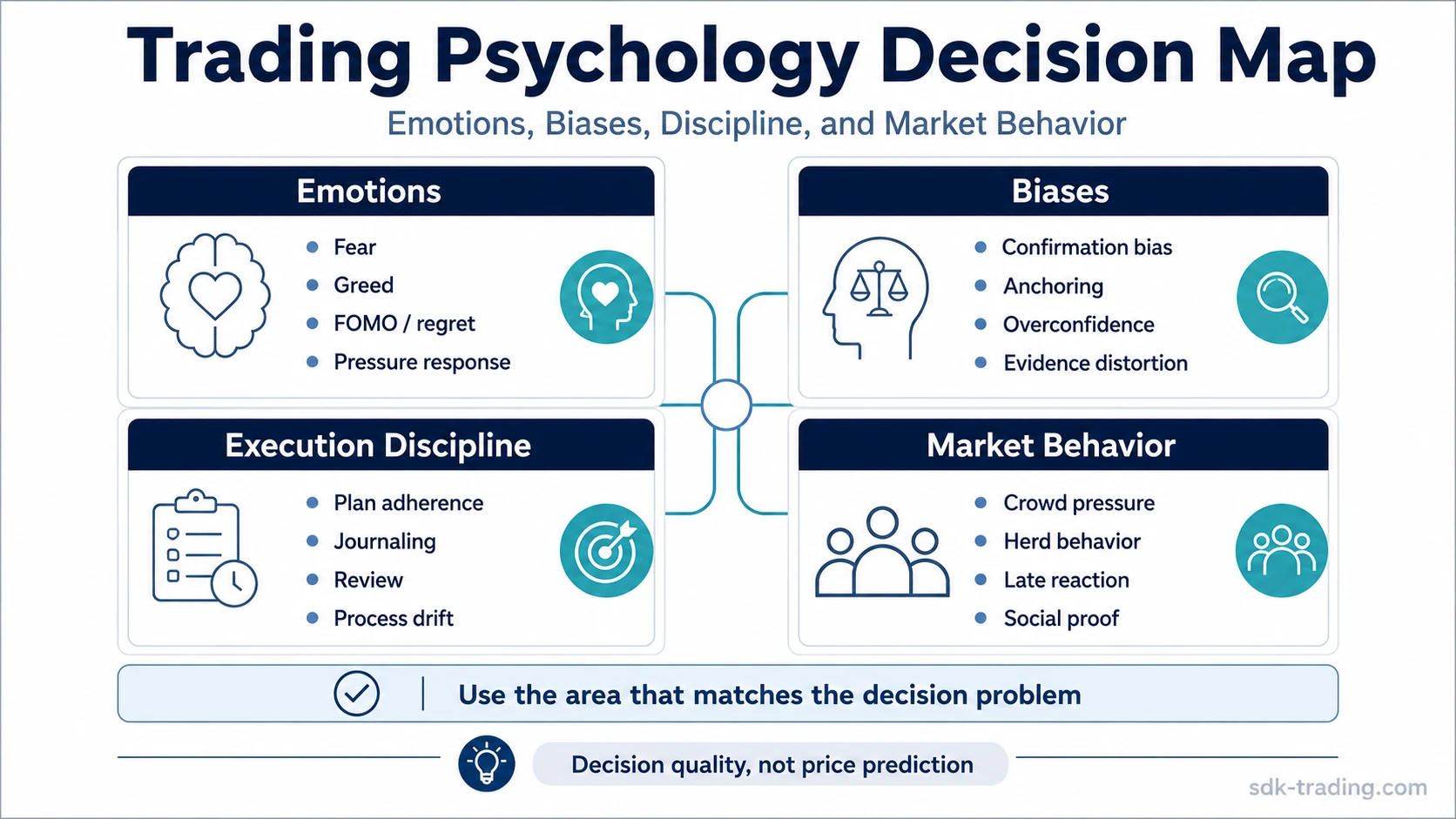

The useful starting point is separation. Fear, greed, regret, and FOMO are emotional pressure states. Confirmation bias, anchoring, overconfidence, and loss aversion are recurring interpretation errors. Execution discipline covers whether a trader can follow a plan, review decisions, and avoid process drift. Market behavior covers how crowd pressure can influence participation, reaction, and decision quality.

For the core definition, start with trading psychology, then move into the specific area that matches the problem: emotion control, bias recognition, execution discipline, or crowd behavior.

Key Points

- Trading psychology is about decision quality under uncertainty, not about proving what price will do next.

- Emotions are pressure states; biases are recurring thinking errors; discipline problems are process failures.

- A clearer psychology process can help reduce impulsive decisions, but it does not replace market structure, risk awareness, or review.

- The topic is best understood through four areas: emotions, biases, execution discipline, and market behavior.

What Trading Psychology Covers

Trading psychology covers the behavioral factors that shape trading decisions: emotional pressure, cognitive bias, process discipline, and the influence of market participation on interpretation.

The topic is broad, but it should not become vague motivation. A useful framework asks a narrower question: what changed the trader’s decision process? The answer usually sits in one of four areas.

| Area | What it explains | Typical problem | Best next topic |

|---|---|---|---|

| Emotions | Pressure states that affect timing, patience, and reaction. | Fear, greed, regret, FOMO, anxiety, frustration. | Emotional discipline |

| Biases | Recurring thinking errors that distort interpretation. | Confirmation bias, anchoring, overconfidence, loss aversion, herd behavior. | Trading biases |

| Execution discipline | Whether decisions stay aligned with a defined process. | Overtrading, revenge trading, plan drift, poor review habits. | Execution discipline |

| Market behavior | How crowd pressure can shape participation and reactions. | Following the crowd, reacting late, mistaking emotion for evidence. | Market behavior |

Trading Psychology Decision Map

Start with the area that matches the actual decision problem. A trader who understands the definition but keeps reacting emotionally needs a different path from a trader who keeps interpreting evidence through a fixed belief.

| Reader problem | Best starting point | Why this area fits |

|---|---|---|

| “I understand the setup, but pressure changes my behavior.” | How to control emotions in trading | The main pressure is emotional regulation, not another market concept. |

| “I keep finding evidence that supports what I already believe.” | Biases | The main distortion is interpretation quality and mental filtering. |

| “I know the plan, but I do not follow it consistently.” | Execution discipline | The main gap is process adherence and review, not just knowledge. |

| “I react to the crowd and then reassess too late.” | Market behavior | The problem usually sits in participant pressure and crowd-driven interpretation. |

| “I want to identify the recurring errors that damage decisions.” | Psychological mistakes in trading | The main pattern is repeated decision error. |

| “I want to understand why losses can repeat even when a trader knows the theory.” | Why traders lose money | The problem may combine emotion, bias, discipline, and process failure. |

Emotions, Biases, Discipline, and Market Behavior

Emotions are fast pressure responses. Fear can make a trader hesitate. Greed can make the trader ignore restraint. Regret can pull attention back to a missed move. FOMO can create urgency where the process has not confirmed enough information.

Biases work differently. A bias is not just a feeling; it is a recurring distortion in how evidence is selected or interpreted. Confirmation bias looks for support. Anchoring fixes attention on one reference point. Overconfidence reduces skepticism. Loss aversion can make a trader manage pain instead of information.

Discipline problems appear when the trader’s process and behavior separate. A trader can understand the setup, the context, and the risk, yet still drift if the review process is weak or if emotional pressure overrides the plan.

Market behavior adds the crowd layer. A trader is not only interpreting price and volume; the trader is also reacting to other participants, visible momentum, social pressure, and the discomfort of being early, late, or wrong. That pressure can make weak evidence feel stronger than it is.

What Belongs in Trading Psychology

Trading psychology belongs where the main issue is the decision process. That includes emotional control, bias recognition, discipline, journaling, review, crowd pressure, and the difference between a planned decision and a reactive decision.

| Belongs here | Does not belong here as the main topic |

|---|---|

| Fear, greed, FOMO, regret, anxiety, frustration. | Detailed market-structure classification. |

| Confirmation bias, anchoring, overconfidence, loss aversion. | Indicator mechanics or pattern identification. |

| Overtrading, revenge trading, plan drift, weak journaling. | Portfolio construction or company valuation. |

| Crowd pressure, herd behavior, late reaction, emotional participation. | Macro regime analysis or stock-specific thesis work. |

This boundary matters because psychology can explain why a trader misreads or mishandles information, but it should not replace the information itself. A better mental process still needs a clear market framework and disciplined review.

How Emotions and Biases Differ

Emotions are pressure states that can change behavior quickly. Biases are repeatable thinking patterns that can change interpretation even when the trader feels calm. Both can appear together, but they are not the same problem.

Practical scenario: A trader may feel fear after several losses and close decisions too quickly. That is an emotional pressure problem. Another trader may ignore conflicting evidence because it does not fit the original view. That is closer to a bias problem. In both cases, the issue is decision quality, but the corrective work is different.

Emotional discipline focuses on pressure management. Bias work focuses on evidence quality. Execution discipline connects both to a repeatable process.

Execution Discipline and Process Drift

Execution discipline is the bridge between knowledge and behavior. It asks whether the trader can follow a defined process when the market becomes uncomfortable, noisy, or fast-moving.

Process drift often appears gradually. The trader may skip review, change rules after a loss, take weaker decisions after frustration, or treat a recent outcome as more important than the full decision history. The issue is not always lack of knowledge. Often it is a gap between the process written down and the process actually followed.

Useful distinction: A mistake is not only a losing decision. A mistake is a decision that breaks the process, ignores the evidence standard, or turns emotional pressure into action.

Market Behavior and Crowd Pressure

Trading psychology also includes the pressure created by other participants. Strong visible movement can make a trader feel late. Fast reversals can make the trader feel wrong before the full context is clear. Social proof can make a weak idea feel safer because many people appear to believe it.

Crowd pressure does not automatically make the crowd wrong. The point is narrower: a trader needs to separate observed market behavior from emotional participation. Without that separation, the trader may react to urgency rather than evaluate structure, evidence, and process.

What Trading Psychology Does Not Prove

Trading psychology does not prove future price behavior. It does not replace market structure, risk evaluation, technical context, or a review process. It helps explain how decision quality can weaken under pressure.

A calm trader can still be wrong. A disciplined trader can still face uncertainty. A well-reviewed process can still produce losing outcomes. The value of trading psychology is not certainty; it is cleaner behavior, better evidence handling, and fewer avoidable process errors.

The safest use is diagnostic. When a decision goes wrong, ask whether the issue came from the market read, the risk framework, the emotional state, the bias pattern, or the execution process. That separation makes review more useful than a general statement such as “psychology was the problem.”

Where to Go Next

Choose the next topic by the decision problem you are trying to isolate.

| Next topic | Use it when |

|---|---|

| Emotional discipline | You want to understand fear, greed, FOMO, regret, and pressure-driven behavior. |

| Trading biases | You want to understand repeated thinking errors that distort evidence. |

| Execution discipline | You want to understand plan adherence, review, journaling, and process drift. |

| Market behavior | You want to understand crowd pressure, participant behavior, and reaction patterns. |