Trading biases are decision distortions that can affect how a trader reads evidence, handles risk, reacts to losses, sizes confidence, or reviews outcomes after the fact.

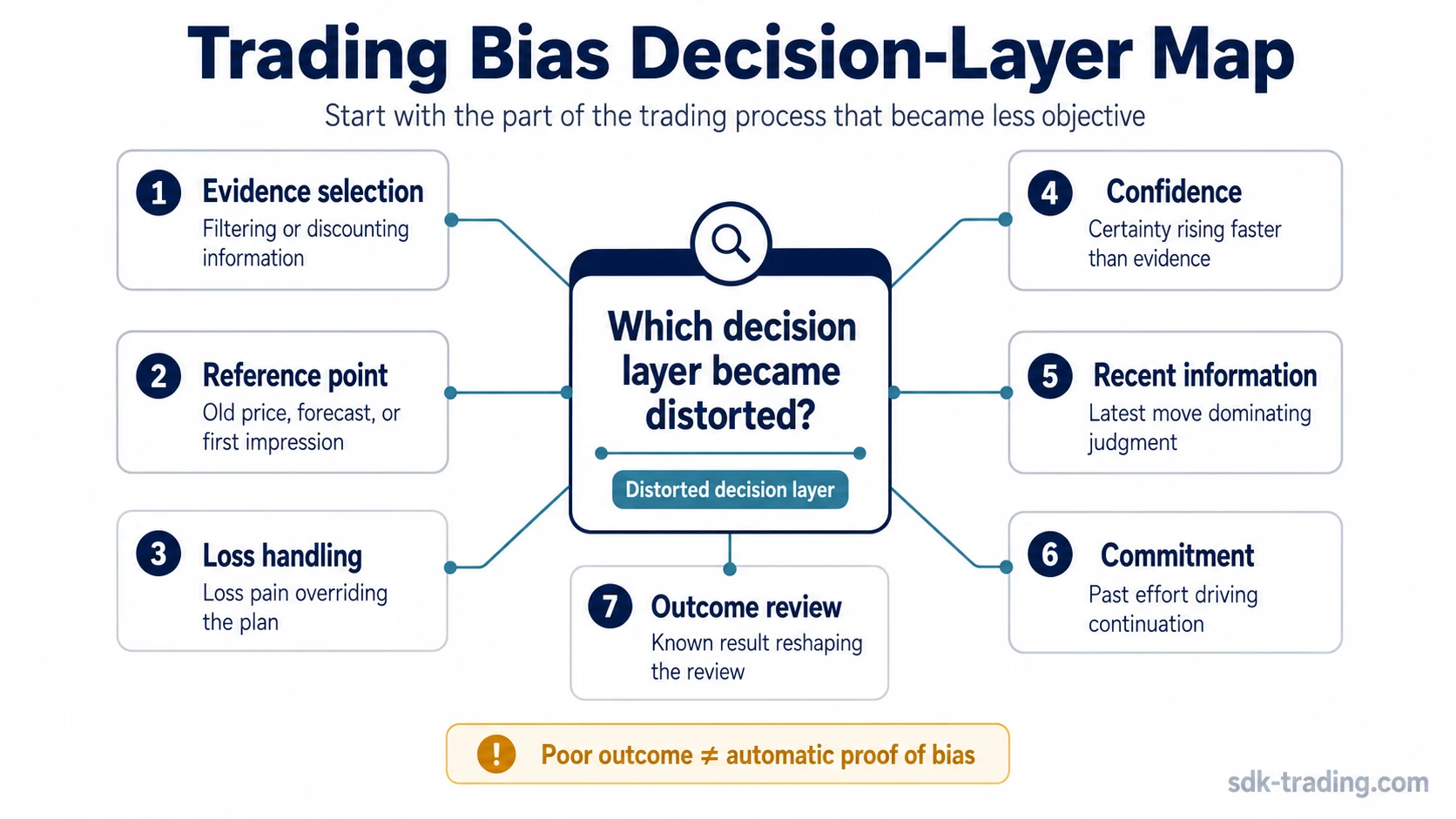

The most useful starting point is the part of the trading decision that became less objective: evidence selection, reference-point fixation, risk perception, loss handling, confidence, recent-information weighting, commitment pressure, or outcome review.

Core idea: A trading bias is most useful to identify by the decision process it distorts, not by the emotional discomfort of the trade outcome. The question is not only “Was the trade good or bad?” but “Which part of the process became less objective?”

Key Points

- Trading biases can distort evidence selection, reference points, risk perception, loss handling, confidence, recent-information weighting, and outcome review.

- Bias classification becomes clearer when the distorted decision layer is identified before the label is chosen.

- A poor result is not automatically proof of bias; markets can produce uncertain outcomes even when the process was disciplined.

- Each bias needs its own explanation because similar trading behavior can come from different process errors.

What Trading Biases Distort

Trading biases usually show up as process distortions before they show up as visible mistakes. A trader may give more weight to evidence that supports an existing view, stay attached to an old reference point, avoid accepting a defined loss, or become too confident after a recent sequence of favorable outcomes.

The same trade outcome can come from different process problems. A late exit may involve loss aversion, disposition effect, sunk-cost thinking, or simple plan failure. A strong opinion after a few recent examples may involve recency bias, overconfidence, or confirmation bias. The useful step is to locate the distorted decision layer before assigning the label.

Classification principle: Start with the part of the trading process that became distorted, then match the label to that specific process error.

Bias Route Classifier

The classifier below separates common trading distortions by the process they affect. It is not a certainty tool or a psychological diagnosis.

| Trading distortion | Likely bias concept | When to start there |

|---|---|---|

| Fixating on an earlier price, forecast, level, or first impression | anchoring bias | Start here when the decision keeps revolving around an old reference point even after new evidence appears. |

| Selecting evidence that supports the preferred view while discounting conflicting information | confirmation bias | Start here when the trader is defending a view more than testing it. |

| Handling winners and losers differently because the realized outcome feels more important than the plan | disposition effect | Start here when the problem is tied to realizing gains, holding losses, or treating open P/L as the main decision driver. |

| Judging the old decision as obvious only after the outcome is known | hindsight bias | Start here when review becomes “I should have known” instead of a fair comparison between available evidence and later outcome. |

| Reacting to the pain of loss more strongly than the structure of the plan supports | loss aversion | Start here when avoiding loss, accepting loss, or recovering from loss becomes the dominant decision pressure. |

| Treating confidence, recent success, or familiarity as stronger evidence than the setup quality supports | overconfidence bias | Start here when confidence rises faster than evidence quality, risk control, or invalidation discipline. |

| Overweighting the most recent move, headline, setup, or trade sequence | recency bias | Start here when the latest information dominates the decision more than the broader structure or sample size justifies. |

| Continuing a decision because time, effort, money, or attention has already been committed | sunk cost fallacy | Start here when the reason for staying involved is past commitment rather than current evidence. |

How to Choose the Right Bias Label

Choose the bias label by asking what changed in the decision process. A trader who ignores contradictory evidence should usually start with confirmation bias. A trader who cannot move away from an old level or thesis should usually start with anchoring bias. A trader who keeps escalating commitment because of prior effort should usually start with sunk cost fallacy.

When several labels seem possible, avoid choosing the one that sounds most dramatic. Separate the problem into the decision stage that was affected:

- Evidence stage: Was the trader selecting, ignoring, or overweighting information?

- Reference stage: Was the decision tied to an old price, forecast, or prior belief?

- Risk stage: Did loss pain, confidence, or commitment override the plan?

- Review stage: Did the known outcome distort how the original decision was judged?

Illustrative scenario: A trader reviews a losing setup and says the mistake was “bad discipline.” That may be too broad. If the trader ignored conflicting evidence, confirmation bias may be the right starting point. If the trader held the position mainly because the loss felt hard to accept, loss aversion may be more relevant. If the trader stayed because too much time and attention had already been invested, sunk cost fallacy may explain the process more precisely.

Trading Biases by Decision Layer

Trading biases can be grouped by the decision layer they usually affect. The categories are not rigid, but they help separate similar mistakes that can look alike in a trade review.

| Decision layer | What becomes distorted | Bias concepts to check first |

|---|---|---|

| Evidence selection | The trader gives too much weight to supportive information or recent information. | Confirmation bias, recency bias |

| Reference point | The trader remains tied to an old price, thesis, forecast, or first impression. | Anchoring bias |

| Loss handling | The trader changes behavior because realizing or accepting a loss feels harder than following the plan. | Loss aversion, disposition effect |

| Confidence calibration | The trader treats confidence as evidence or assumes skill is stronger than the data supports. | Overconfidence bias |

| Commitment pressure | The trader stays with a decision because of prior time, money, effort, or emotional investment. | Sunk cost fallacy |

| Outcome review | The trader lets the known result rewrite how obvious the original decision looked. | Hindsight bias |

What Trading Biases Do Not Cover

Trading-bias classification should stay inside market interpretation, risk handling, execution discipline, and outcome review. Broad psychology categories that do not affect the trading decision process should not drive the label.

A separate bias explanation is needed when the same visible behavior can come from different process errors. Holding a losing position, for example, may involve loss aversion, disposition effect, sunk-cost thinking, or a plan that was never clearly defined.

Important boundary: A bad trade outcome is not automatically evidence of bias. A disciplined decision can still lose, and a biased decision can still produce a favorable result. Bias analysis should focus on the decision process, not only the result.

Common Mistake: Treating Every Bad Trade as the Same Bias

The broad label “bias” can become unhelpful when it is used for every mistake. A trader who exits early, holds too long, ignores evidence, or overreacts to recent information may be dealing with different distortions. Compressing all of those problems into one label makes review less useful.

| Weak review label | Better classification question | Possible starting concept |

|---|---|---|

| “I was biased.” | Which evidence did I ignore or overvalue? | Confirmation bias or recency bias |

| “I could not take the loss.” | Was the issue loss pain, holding behavior, or prior commitment? | Loss aversion, disposition effect, or sunk cost fallacy |

| “I should have known.” | Was that actually clear before the outcome was known? | Hindsight bias |

| “I was too sure.” | Did confidence exceed the evidence and risk definition? | Overconfidence bias |

Where to Go Next

When the distorted part of the decision process is already clear, move directly to the most specific bias concept. When the problem still feels broad, start with the decision layer that became least objective.

- Start with evidence: If the issue is selective information, begin with confirmation bias. If the issue is recent information dominating the decision, begin with recency bias.

- Start with reference points: If the decision is tied to an earlier level, forecast, or first impression, begin with anchoring bias.

- Start with loss behavior: If the issue is accepting, realizing, or avoiding loss, compare loss aversion and disposition effect.

- Start with commitment: If the reason for continuing is past investment rather than current evidence, begin with sunk cost fallacy.

- Start with review quality: If the outcome makes the past decision look obvious, begin with hindsight bias.

- Start with confidence calibration: If confidence is stronger than the available evidence, begin with overconfidence bias.

FAQ

Are trading biases the same as emotions?

No. Emotions can influence trading decisions, but a bias is a distortion in how evidence, risk, confidence, loss, or outcomes are interpreted. The same emotion can lead to different process distortions.

Does a losing trade prove that a trader was biased?

No. A losing outcome can happen even when the decision process was disciplined. Bias analysis should compare the decision against the evidence and plan available at the time, not only against the final result.

How should a trader choose between similar bias labels?

Start with the decision layer that became distorted. Evidence problems often point toward confirmation bias or recency bias, loss-handling problems may point toward loss aversion or disposition effect, and outcome-review problems may point toward hindsight bias.