Sunk cost fallacy in trading is a decision bias where already-spent capital, time, research effort, or emotional commitment receives more weight than live market evidence. The problem is not effort itself. The problem appears when past commitment starts replacing fresh reassessment.

Definition: Sunk cost fallacy in trading means continuing to defend a trading idea mainly because resources have already been committed, even though the conditions now present no longer support the same level of conviction.

Key Points

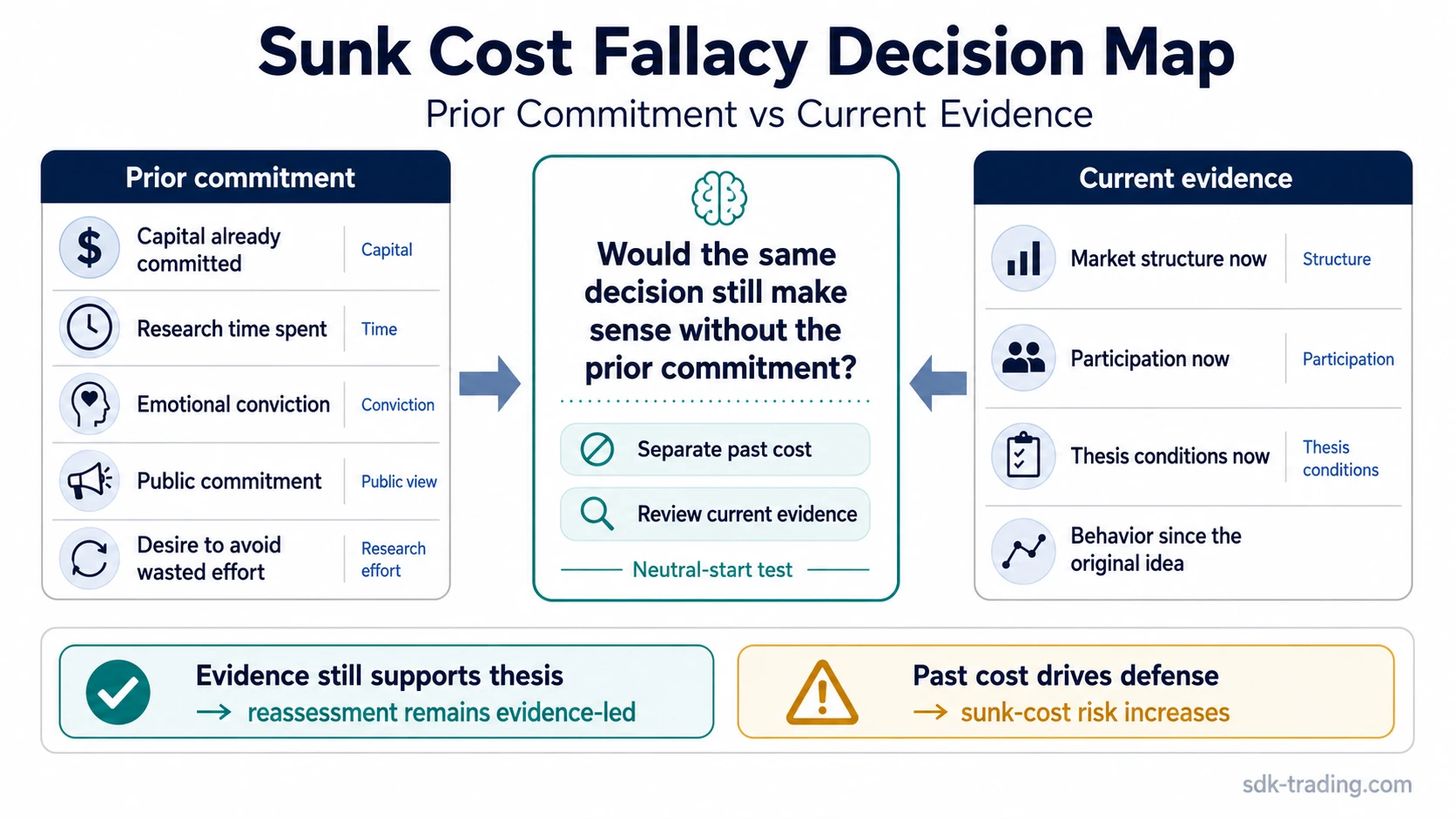

- Sunk cost fallacy is about prior commitment receiving too much weight in a current trading decision.

- The committed resource can be capital, time, research effort, emotional energy, or public conviction.

- The cleanest boundary is prior commitment versus the evidence now visible.

- It differs from loss aversion, disposition effect, recency bias, and anchoring because the driver is irrecoverable commitment.

- A delayed reassessment or remaining in a position through volatility is not automatically sunk cost fallacy.

What Is Sunk Cost Fallacy in Trading?

In trading psychology, sunk cost fallacy appears when a trader gives too much weight to what has already been spent. The past cost cannot be recovered, but it can still influence the next decision if abandoning the original idea feels emotionally difficult.

The practical boundary is simple: past effort explains why the trade idea feels important, but live evidence determines whether the idea still deserves attention. A trader can spend hours on research, absorb a drawdown, or defend a thesis publicly. None of those factors automatically make the idea stronger after market behavior changes.

Core boundary: The question is not “How much has already been spent?” The useful question is whether the same decision would still make sense if the prior cost, effort, and emotional commitment were removed from the evaluation.

How Sunk Cost Fallacy Forms in Trading Decisions

The bias usually forms through a sequence of commitment, defense, and reduced sensitivity to new information. A trader starts with a thesis, invests time or capital into it, and then begins treating that investment as a reason to keep defending the original view.

That process can make weak evidence feel more acceptable than it would look from a neutral starting point. A failed recovery attempt, weakening structure, lower participation, or loss of the original thesis condition may be discounted because abandoning the idea would make the prior effort feel wasted.

| Commitment source | How it can distort reassessment | Cleaner trading question |

|---|---|---|

| Capital already committed | The position feels harder to reassess because the prior cost is emotionally salient. | What does the evidence support from the current point forward? |

| Research time already spent | The original thesis feels more valuable because it required effort to build. | Has new evidence weakened the assumptions behind the idea? |

| Emotional conviction | The trader starts defending being right instead of reviewing the market structure. | Is the decision based on evidence or on protecting the original view? |

| Public commitment | Changing the view feels uncomfortable because the earlier opinion was visible. | Would the decision look the same without the pressure to defend consistency? |

Sunk Cost Fallacy Diagnostic Checklist

A sunk-cost reading becomes more defensible when prior commitment is doing more work than the evidence available now. The checklist below separates the past cost from the live reassessment.

- Identify what has already been spent: capital, time, analysis, emotional effort, or public conviction.

- Separate past cost from current conditions: review structure, behavior, participation, and thesis conditions as they stand now.

- Test the neutral-start decision: ask whether the same decision would still look reasonable without the prior commitment.

- Look for thesis defense: check whether the trader is explaining away new evidence mainly to protect the original idea.

- Define the failure condition: the bias is less likely if the current setup still supports the original thesis; it is more likely if prior commitment is replacing reassessment.

Boundary: A trader can remain patient without falling into sunk cost fallacy. Patience becomes suspect only when the reason for staying committed is the cost already paid rather than the evidence still visible in the market.

Trading Example: Prior Commitment vs Current Evidence

A trader builds a bullish thesis after several hours of research and commits capital. Later, price fails to reclaim the area that supported the original view, recovery attempts stall below the same area, and the conditions used to justify the thesis are no longer visible. The trader still gives more weight to the research time, the drawdown already absorbed, and the desire for the original idea to work than to the evidence now available.

The sunk-cost problem is not the drawdown by itself. It appears when the earlier investment of time, capital, and conviction receives more weight than the current structure. A cleaner reassessment separates what has already happened from the evidence available now.

Sunk Cost Fallacy vs Related Trading Biases

Sunk cost fallacy overlaps with other trading biases, but it has a narrower driver. The central issue is irrecoverable prior commitment. Other biases can reinforce the same behavior, but they do not explain it in the same way.

| Bias | Main driver | How it differs from sunk cost fallacy |

|---|---|---|

| Loss aversion | Pain of realizing a loss | Loss aversion centers on the discomfort of loss realization, while sunk cost fallacy centers on defending resources already committed. |

| Disposition effect | Tendency to realize gains and delay losses | Disposition effect describes a winners-versus-losers pattern, while sunk cost fallacy explains one reason a trader may keep defending a deteriorating idea. |

| Recency bias | Newest information receives too much weight | Recency bias overweights what just happened; sunk cost fallacy overweights what has already been committed. |

| Anchoring | Fixation on a reference point | Anchoring may involve a price, level, or earlier forecast, while sunk cost fallacy involves the emotional weight of prior investment. |

Common Misunderstanding

Misreading the bias: A long reassessment, an uncomfortable drawdown, or remaining exposed through volatility does not automatically prove sunk cost fallacy. The key test is whether the current decision depends mainly on evidence still present in the market or on the difficulty of accepting that prior effort may not be recoverable.

A valid thesis can survive temporary adverse movement if the underlying evidence remains intact. A sunk-cost pattern becomes more likely when the trader keeps adding explanations for why the original idea must still be right while the evidence that justified it has materially weakened.

FAQ

What is sunk cost fallacy in trading?

Sunk cost fallacy in trading is a bias where already-spent capital, time, research effort, or emotional commitment receives more weight than current market evidence.

How can sunk cost fallacy affect trading decisions?

It can make a trader defend an old thesis after the evidence has weakened, especially when abandoning the idea would make prior effort or capital feel wasted.

Is every losing position an example of sunk cost fallacy?

No. The bias appears only when prior commitment dominates reassessment. A position can remain logically valid if current evidence still supports the original thesis.

How is sunk cost fallacy different from loss aversion?

Loss aversion centers on the pain of realizing a loss. Sunk cost fallacy centers on defending capital, effort, or conviction already committed to an idea.