Risk management in trading is the process of defining exposure, loss boundaries, and decision constraints before market uncertainty turns into emotional action. It does not predict direction or make a trade safe. It limits how much damage one decision, one sequence of losses, or one emotional override can create.

Core idea: risk management turns an uncertain market decision into a bounded decision. The trader defines what can be lost, how large the position can be, what would make the idea invalid, and when participation should stop before the position becomes controlled by hope, urgency, or recovery thinking.

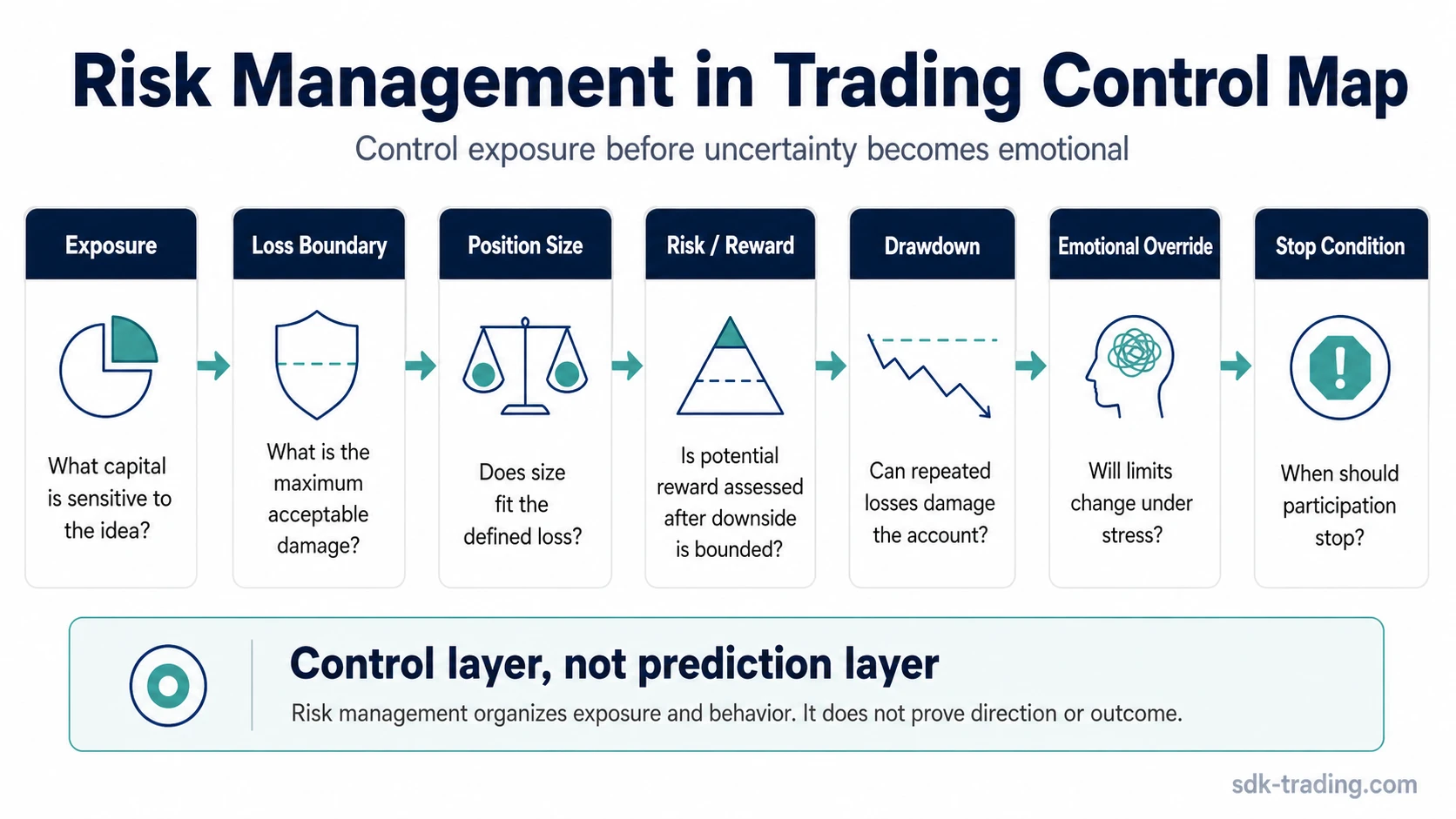

Key Points

- Risk management starts before the trade, not after price begins moving against the position.

- The main control is the acceptable loss, not the desired profit.

- Position size is valid only when it fits the predefined loss limit.

- A stop-loss can be part of risk management, but it is not the whole process.

- Risk control fails when limits expand after emotion enters the decision.

What Risk Management in Trading Means

Risk management in trading means deciding the maximum acceptable damage before exposure is taken. That damage can come from one trade, a same-day sequence, a drawdown period, or repeated decisions that become too large for the account to absorb.

The concept is not only about avoiding loss. Loss is part of trading because outcomes are uncertain. The purpose is to keep loss inside a defined limit so that one idea does not become an account-level problem.

A risk-managed trade has three basic parts: the exposure taken, the condition that proves the idea is no longer acceptable, and the amount of capital that can be lost if that condition occurs. Without those parts, the trader may have an opinion, but the risk is not yet defined.

Control layer, not prediction layer: risk management does not answer where price will go. It answers how much exposure is allowed while the outcome is unknown.

The Risk Boundary Behind Every Trade

The risk boundary is the point where the trade idea stops being acceptable. It may be based on invalidation, maximum loss, session limit, account limit, or a combination of those controls. The important point is that the limit must exist before the position begins affecting emotion.

Once the limit is defined, position sizing in trading translates that limit into exposure. A wider stop condition usually requires smaller size. A larger size requires a tighter and more defensible stop condition. If both size and acceptable loss expand at the same time, risk is no longer being contained.

The same logic applies beyond one position. A trader can define risk per trade but still expose the account to repeated damage if losses cluster, size increases after a loss, or the trader keeps participating after the session has already crossed a reasonable limit.

| Risk question | What must be defined before exposure | What becomes unsafe if undefined |

|---|---|---|

| How much can one trade lose? | The maximum acceptable loss if the idea fails. | A normal loss can become an improvised decision. |

| How large can the position be? | The size that fits the defined loss. | Exposure can become too large for the account or plan. |

| What proves the idea wrong? | The condition that invalidates the trade. | The trader may hold because the loss is uncomfortable rather than because the idea remains valid. |

| When should participation stop? | A trade, session, or account-level stop condition. | Loss recovery can replace process discipline. |

Core Components of Trading Risk Management

Trading risk management works through connected controls. None of them is enough alone. A stop without position size can still be too large. A small position without a defined exit condition can still become uncontrolled. A good reward target without loss containment can create a distorted decision.

| Component | Role in risk control | Failure condition |

|---|---|---|

| Position exposure | Defines how much capital is sensitive to the trade idea. | Exposure grows because of urgency, confidence, or loss recovery rather than defined risk. |

| Loss boundary | Defines the maximum damage allowed before the idea must be abandoned or reassessed. | The limit moves after price has already challenged the idea. |

| Position size | Connects the loss boundary to the amount of capital actually at risk. | Size is chosen first and the risk explanation is added afterward. |

| Risk/reward relationship | Compares the possible loss with the potential reward before participation. | The upside story becomes large enough to excuse poor downside control. |

| Drawdown awareness | Tracks whether repeated losses are damaging the account beyond one trade. | Small losses accumulate into a larger account problem without a stopping rule. |

| Emotional override control | Prevents revenge trading, over-sizing, and limit changes after stress enters. | The plan changes because the trader wants to recover, prove the idea right, or avoid realizing the loss. |

The risk/reward ratio helps organize the relationship between potential loss and potential reward, but it cannot rescue a trade where the loss limit is unrealistic or the position size is too large.

What Risk Management Does Not Do

Risk management does not remove uncertainty. A trade can be planned carefully and still lose. The difference is that the loss remains part of the plan instead of becoming a new decision made under pressure.

Important limitation: risk management controls exposure, not outcome. It does not guarantee safety, profit, accuracy, or emotional discipline. It only creates the conditions where a wrong idea can be contained before it becomes a larger account problem.

A fixed percentage rule is also not complete risk management. A percentage can be useful as a limit, but it does not explain whether the trade idea has a valid invalidation point, whether the position size fits the market structure, whether repeated losses are accumulating, or whether the trader can still follow the rule when pressure increases.

A stop-loss is not the same as risk management either. A stop can define one exit condition, but risk management also includes position size, maximum loss, repeated-loss exposure, account vulnerability, and the decision to stop participating when behavior becomes unstable.

Diagnostic Boundary Map

A risk plan is useful only if it can be checked. The cleanest test is whether the trader can separate the defined limit from the emotional desire to keep the idea alive.

| Diagnostic area | Risk-managed version | Not risk management | Invalidates the control |

|---|---|---|---|

| Before entry | Exposure, acceptable loss, and invalidation are defined before participation. | The trader enters first and decides the risk after the position moves. | The loss limit changes because the trade is already uncomfortable. |

| During adverse movement | The trader compares price behavior with the predefined stop condition. | The trader waits because closing the loss feels unpleasant. | The position is increased to make recovery easier rather than because risk is still controlled. |

| After several losses | Participation slows or stops when the planned loss sequence is reached. | The trader treats the next trade as a way to recover the prior loss. | Trade frequency or size expands after losses. |

| At account level | Losses are measured against broader account vulnerability. | Each trade is viewed in isolation even as account damage grows. | Maximum drawdown becomes an after-the-fact observation instead of a controlled limit. |

Risk Management Example in Context

A trader defines a loss boundary before entering a position. Price then moves against the idea faster than expected. The original limit is close to being reached, but the trader decides to widen it because the move feels temporary. A few minutes later, the trader adds size to reduce the distance needed to recover.

The problem is not that the first trade was wrong. The problem is that the loss limit stopped controlling the decision. The position became larger while the evidence became weaker, and the acceptable loss changed after emotion had already entered. At that point, the trade no longer has defined risk in any practical sense.

A cleaner interpretation separates the market outcome from the decision process. Price can move against a valid idea. Risk becomes undefined only when the trader changes the limit, size, or participation rule because the loss is emotionally difficult to accept.

When Risk Management Fails

Risk management fails when the visible plan and the actual behavior separate. A trader may write down a loss limit, but the limit has little value if it is widened under stress, ignored after a losing streak, or replaced by a recovery trade.

| Failure pattern | Why it breaks risk control | Cleaner interpretation |

|---|---|---|

| Moving the loss boundary | The planned maximum loss is replaced by a new decision made under pressure. | The limit must be defined before the trade has emotional weight. |

| Increasing size after losses | The account becomes more exposed exactly when decision quality may be weaker. | Bigger size requires better evidence and controlled risk, not stronger emotion. |

| Ignoring repeated-loss damage | Each loss may look acceptable alone while the sequence damages the account. | Repeated losses must be measured against account survival, not only trade-by-trade logic. |

| Using reward to excuse risk | A large upside scenario can hide the fact that the downside is not controlled. | Potential reward matters only after the loss limit is believable. |

The account-level version of this problem is risk of ruin: the possibility that repeated losses, excessive size, or uncontrolled exposure make recovery structurally difficult even if some future trades work.

Related Risk Management Concepts

Risk management sets the control layer. Position sizing, risk/reward, drawdown, and risk of ruin explain the separate parts of that control layer.

| Concept | How it connects to risk management |

|---|---|

| Position sizing | Translates the acceptable loss limit into the amount of exposure allowed. |

| Risk per trade | Defines the trade-level loss unit, but it still needs account and sequence context. |

| Risk/reward ratio | Compares possible loss with possible reward before the trade becomes emotional. |

| Maximum drawdown | Measures account damage across a sequence, not only one trade. |

| Common risk management mistakes | Common mistakes usually begin when the trader changes size, limits, or participation rules after stress appears. |

FAQ

What is risk management in trading?

Risk management in trading is the process of defining exposure, acceptable loss, position size, and decision boundaries before a trade or sequence of trades can damage the account.

Is a stop-loss the same as risk management?

No. A stop-loss can be one part of risk management, but the full process also includes position size, account vulnerability, repeated-loss limits, and rules that prevent emotional boundary changes.

How is trading risk calculated?

Trading risk is usually calculated by connecting the distance to the loss boundary with the position size. The practical question is how much capital would be lost if the predefined invalidation or stop condition occurs.

Does risk management guarantee safety?

No. Risk management cannot guarantee safety, profit, or accuracy. It limits exposure and defines what should happen when a trade idea is wrong or when losses begin to cluster.

When does risk management stop being real?

Risk management stops being real when the trader changes size, loss limits, or participation rules because of stress, hope, urgency, or the desire to recover a prior loss.