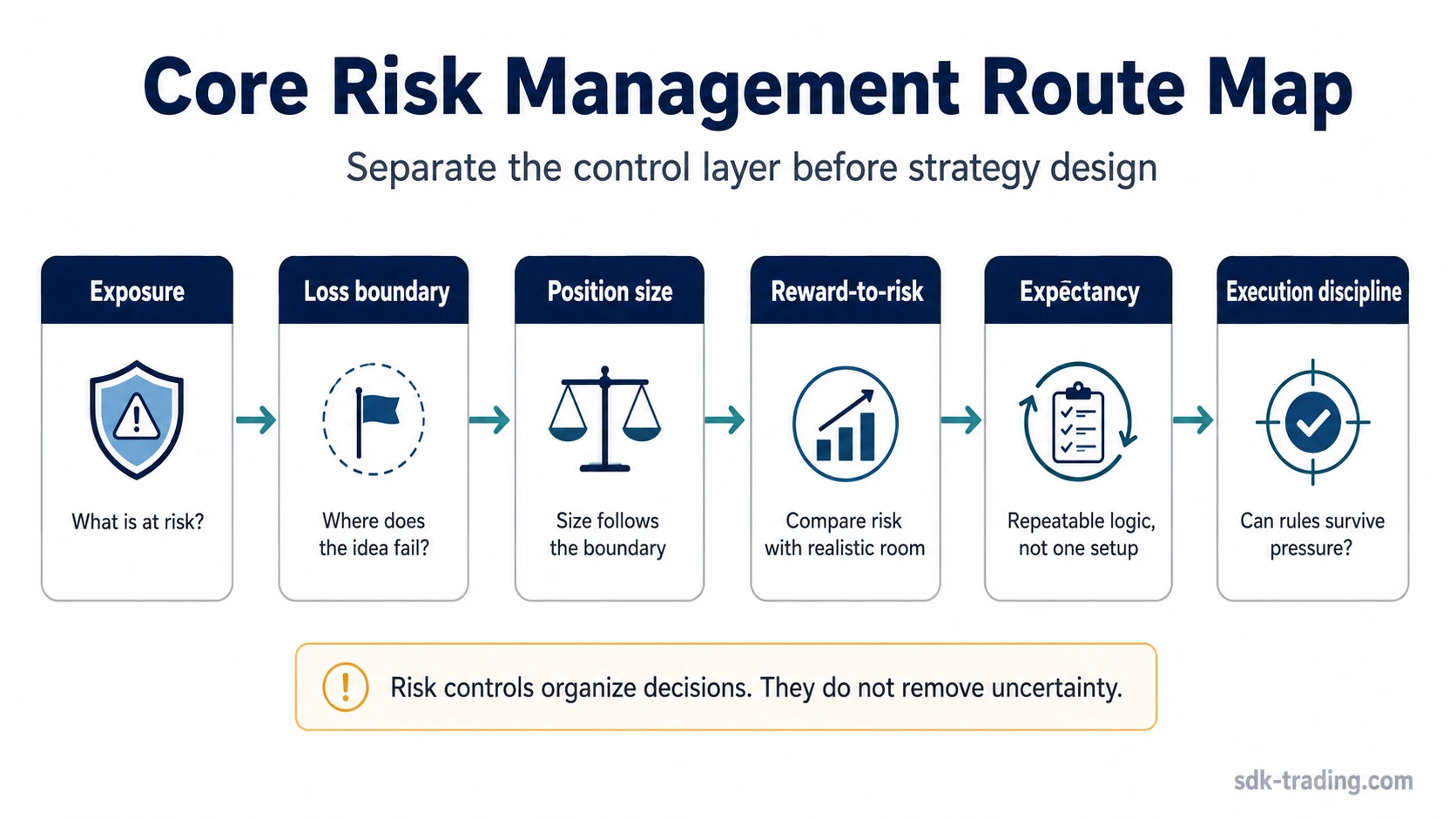

Core risk management for trading is the starting filter that separates exposure, defined loss, position size, reward-to-risk, expectancy, and execution discipline before a trader evaluates any strategy.

Definition: Core risk management is the basic risk-control layer that helps a trader identify what is at risk, where the idea becomes invalid, how size connects to that boundary, and whether the planned risk is supported by expectancy and execution discipline.

Key Points

- Core risk management starts with exposure before strategy selection.

- Position size only has meaning after the loss boundary is defined.

- Reward-to-risk is weak if expectancy and execution discipline are missing.

- A trading idea is not strategy-ready until risk, invalidation, and review logic are clear.

What Core Risk Management Means in Trading

In trading, core risk management is not a prediction tool. It is a control sequence that keeps a market idea separate from the amount of capital exposed, the point where the idea no longer holds, and the conditions required before that idea can be evaluated as part of a strategy.

The sequence is simple: define exposure, define the loss boundary, connect position size to that boundary, compare risk with realistic reward potential, check expectancy, then review whether the rules can be followed during execution.

Classification: Core risk management comes before detailed strategy design. It separates the main trading risk controls first so exposure, loss boundary, sizing, reward-to-risk, expectancy, and execution discipline are not mixed together too early.

- Position exposure: What capital or account risk is actually exposed?

- Defined loss boundary: Where does the idea stop making sense?

- Position sizing: Is size connected to the loss boundary rather than chosen emotionally?

- Reward-to-risk: Is the potential reward large enough to justify the defined risk?

- Expectancy: Does the method have a repeatable logic beyond one attractive setup?

- Execution discipline: Can the rules survive pressure, speed, and uncertainty?

The Core Risk Controls to Separate First

The controls below should be separated before a trader combines them into a broader process. When they are mixed together too early, a setup can look organized while the actual risk remains unclear.

| Risk control | Question it answers | Best next focus |

|---|---|---|

| Position exposure | How much market risk is open before the idea is judged right or wrong? | Start with the broad risk-management foundation. |

| Defined loss boundary | What condition would show that the idea is no longer valid? | Clarify invalidation before thinking about strategy structure. |

| Risk per trade and position sizing | Does the position size match the defined loss boundary? | Separate sizing logic from confidence in the setup. |

| Reward-to-risk relationship | Is the possible reward reasonable compared with the planned risk? | Check whether the setup offers enough room before execution pressure begins. |

| Expectancy filter | Does the method make sense across repeated decisions, not only one example? | Move from single-setup thinking toward repeatable process quality. |

| Execution discipline | Can the trader follow the rule when the market moves quickly or emotionally? | Review the behavioral mistakes that break otherwise clear plans. |

Example: A trader may have a valid market idea, but if exposure is undefined, the loss boundary is unclear, and position size is not connected to that boundary, the idea is not ready for strategy evaluation.

Which Risk Management Topic Should You Read Next?

Different risk questions need different levels of detail. The broad foundation, intraday constraints, mistake patterns, and strategy framework should stay separate so one risk-control problem does not blur into another.

| If your question is about… | Read this next | Why it fits |

|---|---|---|

| The full foundation of trader risk control | risk management in trading | Use this when you need the main concept before separating narrower risk topics. |

| Fast decisions, session pressure, and intraday constraint | risk management in day trading | Use this when time compression and execution speed change the risk-control problem. |

| Why risk rules fail in real decisions | common risk management mistakes | Use this when the issue is not the concept, but the behavior or process error that breaks it. |

| Combining risk controls into a repeatable framework | trading risk management strategy | Use this after exposure, loss boundary, sizing, reward-to-risk, and expectancy are separated. |

Boundary: The broad concept, day-trading constraints, mistake prevention, and strategy framework are related, but they should not be collapsed into one explanation. Each answers a different risk-management problem.

Where Core Risk Management Breaks Down

Core risk management usually breaks down when the trader treats risk as a general intention instead of a defined control system. The issue is rarely one missing rule; it is more often a gap between exposure, invalidation, sizing, expectancy, and execution behavior.

Limitation: Risk rules do not remove loss or uncertainty. They make the loss boundary, decision size, and review process explicit enough to evaluate whether a trading idea is controlled or still incomplete.

| Breakdown | What becomes unclear | Safer risk-control reading |

|---|---|---|

| Undefined exposure | The trader does not know how much account risk is actually open. | Exposure should be clear before the idea is judged as usable. |

| Missing invalidation | The idea has no clear point where it stops making sense. | The loss boundary should exist before position size is chosen. |

| Inconsistent position sizing | Size changes with emotion, confidence, or urgency. | Size should connect to the defined loss boundary, not to excitement about the setup. |

| Distorted reward-to-risk | The possible reward is imagined without checking whether the risk is reasonable. | Reward-to-risk should be evaluated with realistic structure and expectancy. |

| Strategy before expectancy | A single attractive idea is treated as a repeatable method. | Expectancy should be considered before a strategy is treated as repeatable. |

| Rules abandoned during execution | The trader has rules, but pressure changes the decision. | Execution discipline should be reviewed as part of the risk process, not after the fact. |

How Core Risk Management Connects to Strategy

Core risk management gives strategy design its first boundary. Exposure shows what is open, the loss boundary shows where the idea fails, position sizing translates that boundary into account impact, reward-to-risk tests whether the setup is worth considering, and expectancy checks whether the logic can survive repeated use.

Only after those pieces are clear does a broader trading risk-management strategy have enough structure to evaluate entries, filters, review habits, and rule consistency without turning the process into prediction.

Strategy boundary: Core risk management can prepare a trader for strategy design, but it does not provide entry instructions, trade signals, performance promises, or certainty about market direction.

FAQ

Is core risk management the same as risk management in trading?

No. Core risk management is the starting control layer: exposure, defined loss, sizing, reward-to-risk, expectancy, and discipline. Risk management in trading is the broader explanation of how those controls fit the full trading process.

Which risk-management topic should I start with?

Start with the broader trading risk-management foundation if the concept is new. Move to day-trading risk when intraday pressure is the issue, risk-management mistakes when rules break down, and strategy structure when the controls need to become a repeatable framework.

What comes before a trading risk management strategy?

Exposure, loss boundary, position sizing, reward-to-risk, expectancy, and execution discipline should be separated first. Without those controls, a strategy can look organized while the real risk remains undefined.