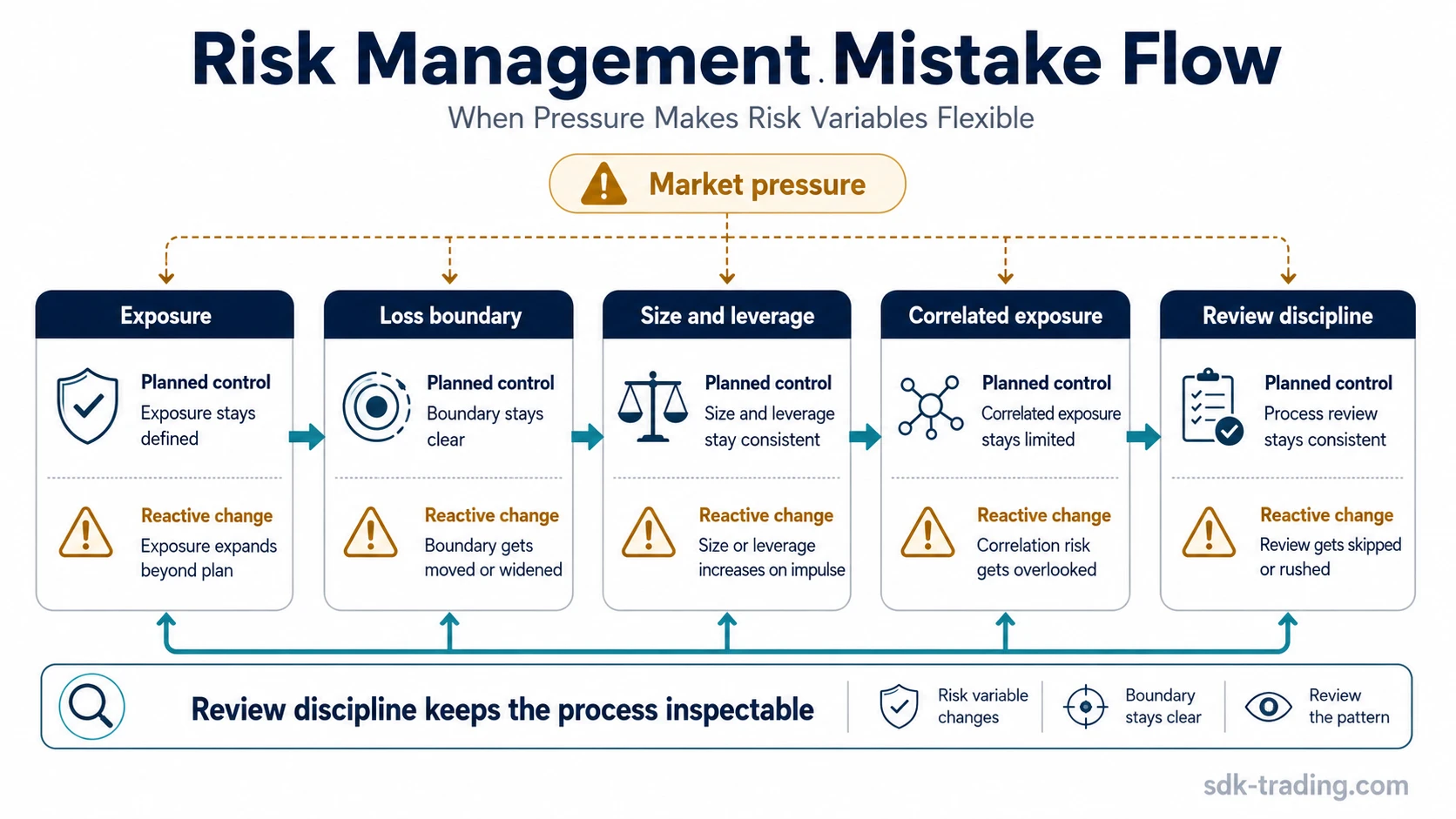

Common risk management mistakes in trading happen when a trader changes exposure, sizing, leverage, loss boundaries, or review rules after pressure starts.

Not every trading mistake is a risk-management mistake. A late entry, a weak read, or a missed move becomes risk-management specific only when it changes capital at risk, loss containment, account exposure, or review discipline.

Boundary condition: A trading mistake becomes a risk-management mistake when the risk decision changes after the trade idea is already under pressure.

The diagnostic value comes from separating risk-control errors from trade-selection errors. The distinction should not be used to predict the next move, choose entries, place targets, or turn a mistake list into a trading signal.

Key Points

- Risk-management mistakes change exposure, sizing, leverage, loss containment, or review discipline.

- Overtrading, oversizing, and stacked exposure can compound risk even when each single decision looks small.

- Loss boundaries are process controls, not prediction tools.

- Pressure often turns predefined rules into flexible reactions unless the review process is clear before the decision starts.

When a trading mistake becomes a risk management mistake

A trading mistake can stay local if it only affects the interpretation of one idea. It becomes a risk-management mistake when the response to that idea changes the amount at risk, the loss boundary, the use of leverage, the number of related positions, or the discipline used to review repeated rule breaks.

A weak entry is not automatically a risk-management failure. The risk problem begins when the trader reacts to discomfort by increasing size, widening the boundary, adding correlated exposure, or treating the next decision as a way to repair the previous one.

Process note: The mistake is usually not being wrong about direction. The mistake is allowing risk variables to become adjustable after the market has already created pressure.

The main risk variables these mistakes distort

Risk-management mistakes are easier to review when they are tied to the specific variable they distort. A vague label such as “bad discipline” is less useful than identifying whether the issue came from exposure, sizing, leverage, loss containment, correlation, cost, volatility, or review behavior.

| Risk variable | What changes under pressure | Why it matters |

|---|---|---|

| Exposure | The trader adds more positions or keeps too much capital tied to one idea. | Account risk can rise even if each decision appears manageable on its own. |

| Position size | The trade becomes larger than the original plan allowed. | The same market movement can create a larger loss than the plan was designed to absorb. |

| Leverage | Borrowed exposure increases the impact of normal price movement. | Small adverse moves can create account-level stress when leverage is too flexible. |

| Loss boundary | The original invalidation point becomes negotiable after discomfort appears. | The decision shifts from controlled risk to delayed acceptance of the failed idea. |

| Correlation | Several positions depend on the same market driver without being treated as connected. | Risk may be concentrated even when the positions look different on the surface. |

| Review discipline | Rule breaks are explained away instead of recorded and reviewed. | The same behavior can repeat because the process never identifies the pattern. |

Common risk management mistakes in trading

A risk-management mistake list is clearest when it separates the surface behavior from the risk variable that changed under pressure.

| Mistake | How it appears | Risk variable distorted | Safer control principle |

|---|---|---|---|

| Oversizing | The position is larger than the plan can tolerate because the idea feels clear or urgent. | Position size | Size should be defined before pressure appears, not adjusted because conviction feels stronger. |

| Overleveraging | Leverage is used to make a normal idea feel more meaningful. | Leverage and account exposure | Leverage should be treated as risk amplification, not as a way to compensate for uncertainty. |

| Moving or ignoring the loss boundary | The original boundary is shifted after price starts moving against the idea. | Loss containment | A boundary should mark where the scenario weakens, not where discomfort becomes harder to accept. |

| Overtrading | Several decisions are taken in quick succession because the trader wants to stay active. | Repeated exposure | Frequency should be reviewed as a risk variable when repeated decisions depend on similar conditions. |

| Chasing after a missed move | The trader increases urgency after the original planned area has already passed. | Entry quality and loss boundary clarity | A missed move should not justify accepting a less defined risk boundary. |

| Revenge trading | The next decision is made to recover emotionally from the previous one. | Discipline and exposure | A new decision should stand on its own structure, not on the desire to repair a prior loss. |

| Ignoring correlation or stacked exposure | Several trades look separate but depend on the same market theme, sector, instrument type, or volatility condition. | Correlated exposure | Related positions should be reviewed as one combined risk footprint when their drivers overlap. |

| Not reviewing repeated rule breaks | The same behavior appears again, but each case is treated as a unique exception. | Review discipline | Repeated exceptions should be logged as process data, not dismissed as isolated moments. |

Why risk rules often fail under pressure

Risk rules often fail because the rule is written before pressure appears, while the violation happens when fear, frustration, overconfidence, or urgency changes the trader’s tolerance for risk. A rule that looked clear before the decision can become negotiable when the trader wants the market to give the idea more time.

Recent wins can create false confidence. Recent losses can create urgency. Missed moves can create chasing behavior. In each case, the risk problem is not the emotion by itself. The problem is allowing the emotion to change exposure, size, leverage, loss boundaries, or review behavior.

Limitation: Rules, journals, and review routines can improve process discipline, but they do not remove uncertainty or guarantee better outcomes. They only make the risk decision easier to inspect.

A simple failure-mode scenario

Illustrative scenario: A trader begins with a defined loss boundary and a position size that fits the original plan. Price moves against the idea, but instead of accepting that the scenario has weakened, the trader adds size and shifts the boundary farther away. The risk-management mistake is not the initial read being wrong. The mistake is allowing exposure and loss containment to change after pressure has already started.

The same situation can remain unresolved rather than clearly wrong if the trader does not add risk but also does not review the boundary. A cleaner process separates three questions: what was the original risk decision, what changed after pressure appeared, and whether the later change was planned or reactive.

How to review the mistake without turning it into a signal

A risk-management review should separate process inspection from trade prediction. The question is whether the prior decision kept its risk variables stable after pressure appeared, not whether the next decision should be larger, smaller, long, short, or avoided.

| Review question | What it checks | Unsafe interpretation to avoid |

|---|---|---|

| Was the loss boundary defined before the decision? | Whether invalidation was known before discomfort appeared. | Treating the boundary as a prediction of where price must reverse. |

| Did position size change after pressure started? | Whether sizing followed the plan or emotional adjustment. | Assuming larger size is justified by stronger conviction. |

| Did related positions increase the same exposure? | Whether correlation made the risk footprint larger than expected. | Counting similar risks as separate simply because instruments differ. |

| Was the rule break recorded? | Whether repeated behavior can be reviewed later. | Explaining each exception away as a special case. |

Review discipline turns a vague mistake into a visible process pattern. The useful question is whether the same risk variable keeps moving after pressure begins.

Where the boundary connects to broader risk management

Risk management in trading defines how risk is planned, contained, reviewed, and kept consistent across decisions. Common mistakes show where that process tends to break under pressure.

Leverage and exposure deserve separate attention because they can turn a normal mistake into account-level stress. A margin call is one possible forced-risk event when leveraged exposure moves beyond the account’s ability to maintain required collateral.

Boundary summary: The narrow issue is not whether a trader can avoid every loss. The issue is whether exposure, size, leverage, loss boundaries, and review rules remain controlled when the market creates pressure.

FAQ

What are common risk management mistakes in trading?

Common risk management mistakes in trading include oversizing, overleveraging, moving loss boundaries, overtrading, revenge trading, chasing missed moves, ignoring correlated exposure, and failing to review repeated rule breaks.

When does a trading mistake become a risk-management mistake?

A trading mistake becomes a risk-management mistake when it changes capital at risk, loss containment, leverage, exposure, or review discipline after pressure has already started.

Is poor entry timing the same as poor risk management?

Poor entry timing is not automatically poor risk management. It becomes a risk-management issue when the trader responds by increasing size, shifting the boundary, adding correlated exposure, or ignoring the original plan.

Why can overtrading increase risk even when each trade looks small?

Overtrading can increase risk because repeated decisions may stack exposure, costs, volatility sensitivity, or emotional pressure. The combined footprint can be larger than each individual trade suggests.