Execution discipline in trading is the ability to follow, adjust, and review a defined trading decision process while pressure is present. The useful question is not whether a trade felt emotional or ended well. The useful question is which part of the process changed before the plan or evidence supported that change.

Core distinction: trading execution discipline is about process control during execution and review. It starts after a trading process exists. If the process itself is unclear, the problem may belong to plan design rather than execution discipline.

Key Points

- Execution discipline concerns how a trader follows, adjusts, and reviews a defined process under pressure.

- A strategy can be reasonable while execution still breaks through skipped checks, changed risk behavior, impulse action, or outcome-based review.

- The same symptom can point to different causes: fatigue, overtrading, weak plan design, inconsistent repetition, or broad behavioral discipline.

- The problem begins when pressure changes the review before the decision record supports that change.

What execution discipline means in trading

Execution discipline in trading means staying aligned with the defined decision process before, during, and after a trade decision. It includes checking whether the setup matched the plan, whether risk behavior stayed inside the intended rules, whether emotional pressure changed the review, and whether the post-trade assessment stayed based on process rather than outcome alone.

It is narrower than broad self-control. A trader may understand risk, know the setup criteria, and still change the action sequence when pressure rises. That is why execution discipline is best read through the affected process layer, not through a general judgment about discipline or personality.

Execution discipline vs strategy

A trading strategy defines what conditions matter. Execution discipline concerns whether those conditions are followed, adjusted, or reviewed consistently once pressure appears. A weak strategy can produce confusion even when the trader follows it. A clear strategy can still be executed poorly if urgency, fear, fatigue, or outcome bias changes the process.

Practical distinction: strategy failure asks whether the decision rules were useful enough. Execution-discipline failure asks whether the trader followed and reviewed the rules that were already defined.

| Question | Likely process reading |

|---|---|

| Were the rules unclear before the decision? | The issue may be plan design, not execution discipline. |

| Were the rules clear, but the action changed under pressure? | The issue may sit inside execution discipline. |

| Did the review change only after the outcome was known? | The issue may be post-trade review discipline. |

| Did repeated decisions reduce judgment quality? | The issue may be decision fatigue. |

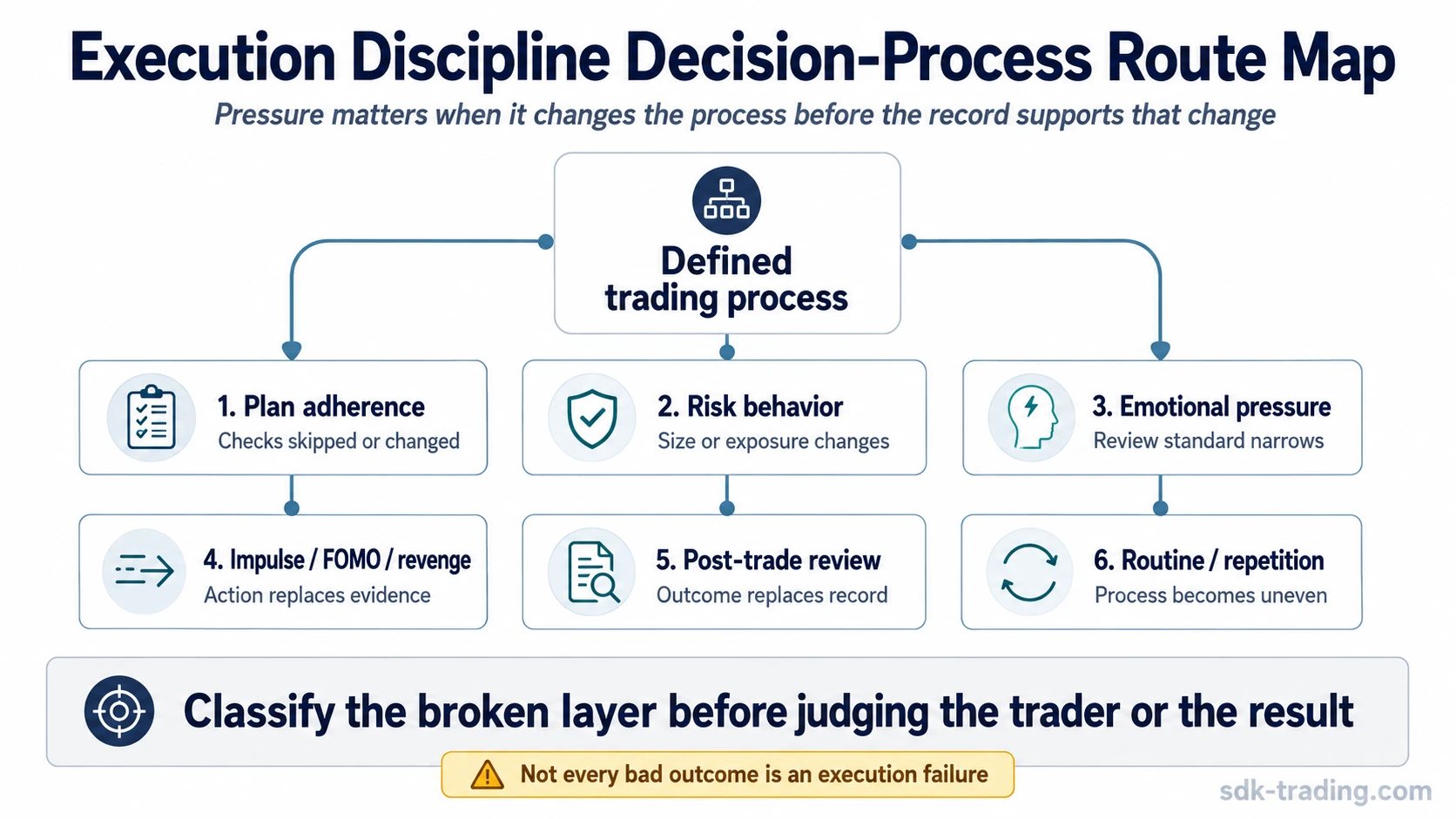

Where the decision process breaks

The broken layer matters because the same visible behavior can come from different causes. A skipped check, a changed risk response, a rushed action, or a distorted review should be read through the process layer that changed first.

| Process layer | What changes under pressure | Safer interpretation |

|---|---|---|

| Plan adherence | The trader skips the planned checks or adds new conditions after pressure rises. | Execution is suspect when the process was defined before pressure appeared. |

| Risk behavior | Size, exposure, or risk response changes before the evidence changes. | Risk reduction can be reasonable, but the decision record should explain why it changed. |

| Emotional pressure | Fear, urgency, frustration, or relief changes the review standard. | The emotion is not the issue by itself; the process change is the issue. |

| Impulse, revenge, or FOMO behavior | Action is added because pressure demands activity rather than because the plan has updated. | Forced activity often belongs closer to overtrading than to general discipline. |

| Post-trade review | The outcome replaces the original decision record as the main evidence. | A good outcome can still hide poor process, and a losing outcome can still come from valid execution. |

| Routine and repetition | The same process is applied unevenly across similar conditions. | Repeated rule-following over time may point toward consistency rather than a single execution break. |

Execution discipline vs nearby trading psychology concepts

Execution discipline overlaps with several trading psychology concepts, but each concept owns a different part of the problem. The safer classification comes from separating the broken execution layer from the broader behavior pattern around it.

| Concept | Main question | Boundary against execution discipline |

|---|---|---|

| Execution discipline | Did pressure change a defined decision process? | Focuses on process adherence, adjustment, and review under pressure. |

| Trading discipline | Is the broader rule-following and self-control structure stable? | Broader than execution; it includes general behavioral control, restraint, and rule respect. |

| Consistency in trading | Is the same process applied repeatedly across comparable situations? | More about repetition over time than one pressure-driven execution break. |

| Overtrading | Is the trader acting too often or forcing action outside the plan? | More about excessive activity, impulse, revenge, or FOMO behavior. |

| Decision fatigue | Has repeated decision load weakened review quality? | More about cognitive depletion than willingness to follow a rule. |

| Trading plan | Was the decision process clearly defined before execution? | If the plan was vague, the failure may be design clarity rather than execution discipline. |

Choose the right next concept

| If the issue is… | Read | Why that concept fits |

|---|---|---|

| Following the same rules across repeated situations | consistency in trading | The main issue is stable repetition, not only one pressure-driven decision. |

| Reduced clarity after too many decisions | decision fatigue | The main issue is depleted judgment and weaker review quality. |

| Taking too many trades, forcing action, or chasing movement | overtrading | The main issue is excessive or impulse-driven activity. |

| Broad rule adherence, restraint, and self-control | trading discipline | The main issue is wider behavioral discipline rather than a specific execution layer. |

| Unclear rules before the decision is made | trading plan | The main issue is whether the process was defined clearly enough before execution. |

Common misclassification

Not every skipped trade is poor discipline. Not every risk reduction is fear. Not every losing outcome is an execution failure. Not every fast action is overtrading. The stronger warning sign is a process change that appears before the plan, evidence, or review record supports that change.

A skipped trade may be reasonable if the setup no longer matches the plan. Risk reduction may be reasonable if the evidence changed. A losing trade may still be well executed if the decision record was followed. A fast action may be valid if it was already part of the process.

Practical routing scenario

A trader has a defined pre-trade checklist, but after several difficult decisions the trader starts skipping the review and acting from urgency. If the rules were clear and pressure changed the sequence, the problem may sit inside execution discipline. If the trader keeps adding trades to recover from frustration, the better match may be overtrading. If the trader cannot think clearly after repeated decisions, decision fatigue may explain the failure more accurately. If the checklist was vague from the beginning, the starting problem may be the trading plan.

FAQ

Is execution discipline the same as trading discipline?

No. Execution discipline is narrower. It concerns whether a defined decision process is followed, adjusted, and reviewed under pressure. Trading discipline is broader and includes general rule adherence, restraint, and behavioral control.

Is every losing trade an execution-discipline problem?

No. A losing trade can still come from valid execution if the plan was defined, the evidence was reviewed consistently, and the process was followed. The concern begins when the decision record changes only because the outcome is uncomfortable.