Position sizing in trading is the process of deciding how large a trade or exposure should be relative to account size, accepted account pressure, and trade-level risk. It controls exposure size; it does not decide whether the trade idea is valid, whether price will move as expected, or whether the outcome will be profitable.

Core definition: Position sizing converts a risk boundary into an exposure amount. The decision connects capital base, accepted account pressure, trade-level risk, volatility or distance, and existing open exposure before the final size is set.

Key Points

- Position sizing controls exposure size, not trade validity.

- Account size, accepted account pressure, and trade-level risk shape the final size.

- Volatility, distance, concentration, and open exposure can change the size even when the market idea stays the same.

- Calculators can help implement sizing inputs, but they do not replace the concept.

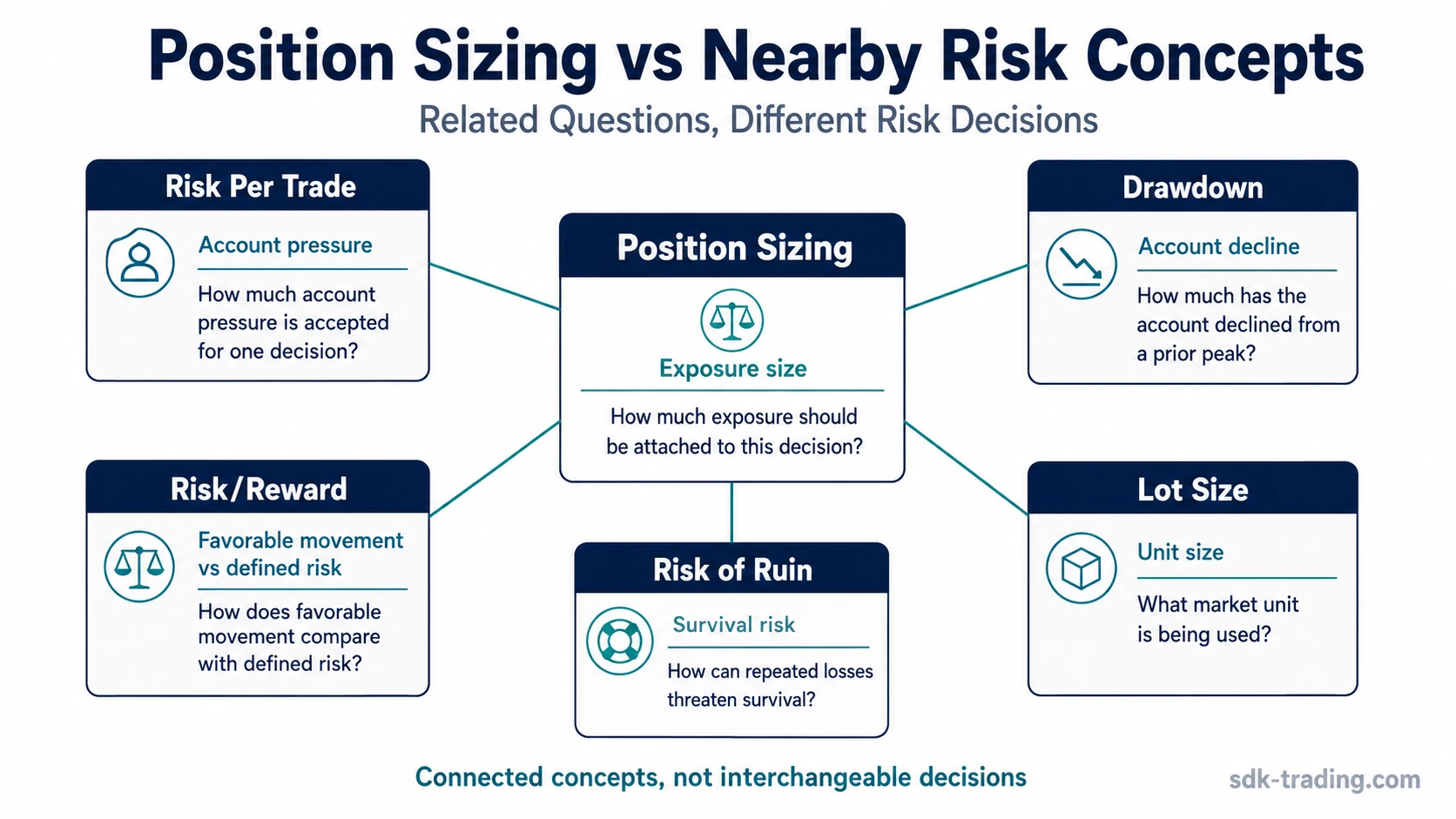

- Position sizing is different from risk/reward, drawdown, stop placement, risk of ruin, and lot size.

What Position Sizing in Trading Means

Position sizing links the size of a position to the amount of account pressure a trader is willing to accept if the idea fails. A trade can look similar on a chart while requiring different exposure because the account, instrument, volatility, distance to invalidation, or open portfolio exposure is different.

The basic logic is not “how many shares, contracts, or lots feel right.” The logic is whether the exposure fits the risk boundary of the account and the structure of the trade. That makes position sizing a risk-control layer rather than a prediction layer.

Useful boundary: A larger position does not make a setup better. A smaller position does not make a weak setup stronger. Size only changes how much account exposure is attached to the decision.

What Position Sizing Does Not Decide

Position sizing does not confirm a trade, improve the quality of a signal, or prove that the market should move in one direction. A position can be sized carefully and still lose. A trade can also be poorly sized even when the original market idea is reasonable.

Many sizing mistakes begin when conviction, frustration, or recent outcome replaces a defined risk boundary. A trader may increase size because the setup feels strong, reduce size because the last trade lost, or hold the same size across very different volatility conditions. Those decisions are not controlled position sizing unless they still reference account exposure and trade-level risk.

Failure condition: If size is changed without reference to account exposure, risk per unit, volatility or distance, open exposure, or drawdown tolerance, the decision is not truly controlled position sizing.

How Account Risk and Trade Risk Shape Position Size

Position size usually comes from two different risk questions. The first is account-level pressure: how much stress the account can absorb from one decision or a group of open positions. The second is trade-level risk: how much exposure each unit of the position carries if the idea is invalidated.

Account risk describes the account-level side of that decision. Trade-level risk describes the exposure attached to each share, contract, option premium, lot, or other position unit. Position sizing connects those two ideas so the final exposure is not chosen in isolation.

| Input | Question it answers | How it affects size |

|---|---|---|

| Capital base | What account or portfolio amount is being exposed? | Defines the base from which account pressure is judged. |

| Accepted account pressure | How much account stress is acceptable if the decision fails? | Limits how much total exposure can be attached to the trade. |

| Trade-level risk | How much risk exists per unit of exposure? | Determines how many units can fit inside the accepted pressure. |

| Volatility or distance | How much room does the instrument need before the idea is invalidated? | Wider movement or larger distance usually reduces allowable size. |

| Open exposure | How much related risk is already active? | Can reduce size when exposure is concentrated or correlated. |

The Position Sizing Mechanism

A controlled sizing decision follows a sequence. It starts with capital base, then defines acceptable account pressure, then identifies the trade-level exposure unit, then converts that information into position size, and finally checks the account or portfolio consequence.

- Capital base: define the account, portfolio sleeve, or risk budget being considered.

- Accepted pressure: define how much account stress the decision can create.

- Exposure unit: identify the risk attached to one share, contract, lot, option structure, or other unit.

- Position size: translate the accepted pressure into a number of units.

- Consequence check: compare the resulting exposure with open positions, concentration, volatility, and drawdown tolerance.

This sequence keeps the sizing decision tied to risk rather than emotion. The same setup can produce a smaller or larger position depending on the account, instrument, volatility, and existing exposure.

Position Sizing vs Risk Per Trade, Drawdown, and Risk/Reward

Position sizing is often confused with related risk terms. The terms interact, but they do not answer the same question.

| Concept | Question answered | What it does not answer |

|---|---|---|

| Position sizing | How much exposure should be attached to this decision? | Whether the trade idea is valid or likely to work. |

| Risk per trade | How much account pressure is accepted for one decision? | Whether the position fits wider portfolio concentration. |

| Risk/reward ratio | How potential favorable movement compares with defined risk. | How large the position should be. |

| Drawdown | How much the account has declined from a prior peak. | Whether one specific position is sized correctly. |

| Risk of ruin | How repeated losses could threaten account survival. | The exact exposure for one individual trade. |

| Stop-loss placement | Where a trade idea is no longer accepted or where risk is controlled. | The account-level amount that should be exposed. |

| Lot size | What unit size is used in the market or instrument. | Whether that unit size is appropriate for the account. |

A Simple Position Sizing Scenario

A trader reviews the same market idea in two different conditions. In the first condition, volatility is low, open exposure is limited, and the trade-level risk per unit is small relative to the account boundary. In the second condition, volatility is wider, several related positions are already open, and each unit carries more account pressure. The market idea has not changed, but the acceptable size may change because the account consequence is different.

The scenario does not require a forecast, target, or exact percentage rule. The important point is that position size comes from exposure control, not from confidence alone.

Common Position Sizing Mistakes

Most sizing errors come from disconnecting exposure from risk. The mistake may look technical, emotional, or procedural, but the common pattern is the same: size is chosen before the real account consequence is understood.

| Mistake | Why it creates risk | Safer interpretation |

|---|---|---|

| Using the same share size every time | Different instruments and volatility conditions can create different account pressure. | Size should respond to the exposure created by the specific instrument and setup structure. |

| Scaling because of emotion | Frustration, excitement, or recent results can replace the original risk boundary. | Size changes need a risk reason, not only a feeling of confidence or urgency. |

| Ignoring volatility | A wider-moving instrument can make the same unit count much more aggressive. | Volatility and distance should be considered before exposure is finalized. |

| Calculator-only thinking | A calculator can process inputs without judging whether the inputs are complete. | The logic behind the inputs matters more than the tool output alone. |

| Ignoring concentration | Several positions may behave similarly even if each one looks acceptable alone. | Open exposure should be checked before adding another related risk. |

| Treating size as trade quality | A carefully sized trade can still be a weak idea, and a strong idea can still be oversized. | Sizing controls account impact; it does not validate the market thesis. |

Where Calculators Fit

A position size calculator can be useful when the required inputs are already clear. It may help convert account size, accepted pressure, and unit risk into a position amount. It cannot decide whether the trade idea is valid, whether volatility has been understood, or whether existing exposure makes the final size too concentrated.

Calculator boundary: A calculator implements a sizing rule. It does not replace the judgment needed to define the account boundary, trade-level risk, volatility context, and open exposure.

Method families such as fixed fractional sizing, volatility-adjusted sizing, risk parity, or Kelly-style sizing can describe different approaches to exposure control. They should not be treated as automatic rules, rankings, or promises of better results. The useful question remains whether the method keeps exposure aligned with the account and the risk being taken.

Position Sizing in Stocks, Options, Forex, and Other Markets

The principle is the same across markets, but the exposure unit changes. A stock position may be counted in shares. A forex position may use lots. An options position may involve premium, Greeks, expiration, assignment risk, or spread structure. Futures and leveraged instruments may include contract multipliers and margin effects.

Because the exposure unit changes, the same surface size can represent very different account pressure. The correct comparison is not the visible number of units alone, but the risk those units create relative to the account and the rest of the portfolio.

Instrument boundary: More complex instruments usually make exposure checks more important. Premium, leverage, margin, volatility, contract structure, and liquidity can change the real pressure behind a position.

When Position Sizing Is Being Controlled

A sizing decision is more controlled when the trader can identify the account boundary, the trade-level exposure unit, the reason for the size, and the consequence of being wrong. A sizing decision is weaker when the answer depends mainly on confidence, recent results, desired profit, or a tool output with incomplete inputs.

| Check | Controlled sizing signal | Weak sizing signal |

|---|---|---|

| Account boundary | The account pressure is defined before size is chosen. | The size is chosen first and the account impact is checked later. |

| Unit risk | The exposure carried by each unit is understood. | Only the number of units is considered. |

| Volatility and distance | The size reflects how much movement the idea requires before invalidation. | The same size is used across different volatility environments. |

| Open exposure | Related positions and concentration are reviewed. | Each trade is sized as if it existed alone. |

| Decision reason | The size can be explained through risk logic. | The size comes mainly from confidence, fear, or a desire to recover losses. |

Position Sizing in Trading FAQ

What is position sizing in trading?

Position sizing in trading is the process of deciding how large a position should be relative to account size, accepted account pressure, and trade-level risk. It controls exposure size, not trade validity or outcome.

Is position sizing the same as risk per trade?

No. Risk per trade describes the accepted account pressure for one decision. Position sizing converts that risk boundary and the trade-level exposure unit into the actual size of the position.

Is a position size calculator enough?

A calculator can help process inputs, but it is not enough by itself. The inputs still need to reflect account size, accepted pressure, unit risk, volatility, distance, and open exposure.

Does position sizing improve trade quality?

No. Position sizing controls how much exposure is attached to a decision. It does not make a weak setup strong, confirm direction, create edge, or guarantee a better outcome.

How is position sizing related to drawdown?

Position sizing can affect how much account pressure a losing sequence creates, while drawdown measures decline from a prior account peak. They are related risk concepts, but they are not the same decision.