Position sizing and drawdown work as a risk-management filter that separates position size, loss depth, recovery burden, and account exposure.

Position size, drawdown tolerance, risk per trade, risk/reward, and risk of ruin are connected, but they do not answer the same question. Position size controls exposure. Drawdown measures account pressure. Risk per trade defines the amount at risk if a trade fails. Risk/reward compares potential reward with defined risk. Risk of ruin looks at repeated exposure and the chance that losses compound beyond a survivable level.

The useful starting point is not a formula. It is identifying which risk question is actually being asked before moving into detailed sizing methods, drawdown analysis, reward/risk structure, or survival math.

Key Points

- Position sizing controls how much exposure a trader takes before the result is known.

- Drawdown describes account decline from a prior high and the recovery burden created by that decline.

- Risk per trade depends on both position size and stop distance dependency, not size alone.

- Risk/reward and risk of ruin belong to different decisions: trade structure versus repeated exposure survival.

How Position Sizing and Drawdown Connect

Position sizing sets the amount of market exposure attached to a trade idea. Drawdown shows how account value changes after losses accumulate. A position can look small in share count or contract count, but still create large position risk if the stop distance is wide, volatility is high, or the same risk budget is repeated too often.

Drawdown is also affected by thesis duration and entry patience. A longer thesis may tolerate more normal account volatility than a short tactical setup, but that does not make unlimited exposure acceptable. Trend persistence, stop distance dependency, and the trader’s risk budget all shape whether the position size fits the drawdown tolerance.

Core idea: position sizing is an exposure decision, while drawdown is the account-level pressure created when losses reduce equity from a previous peak.

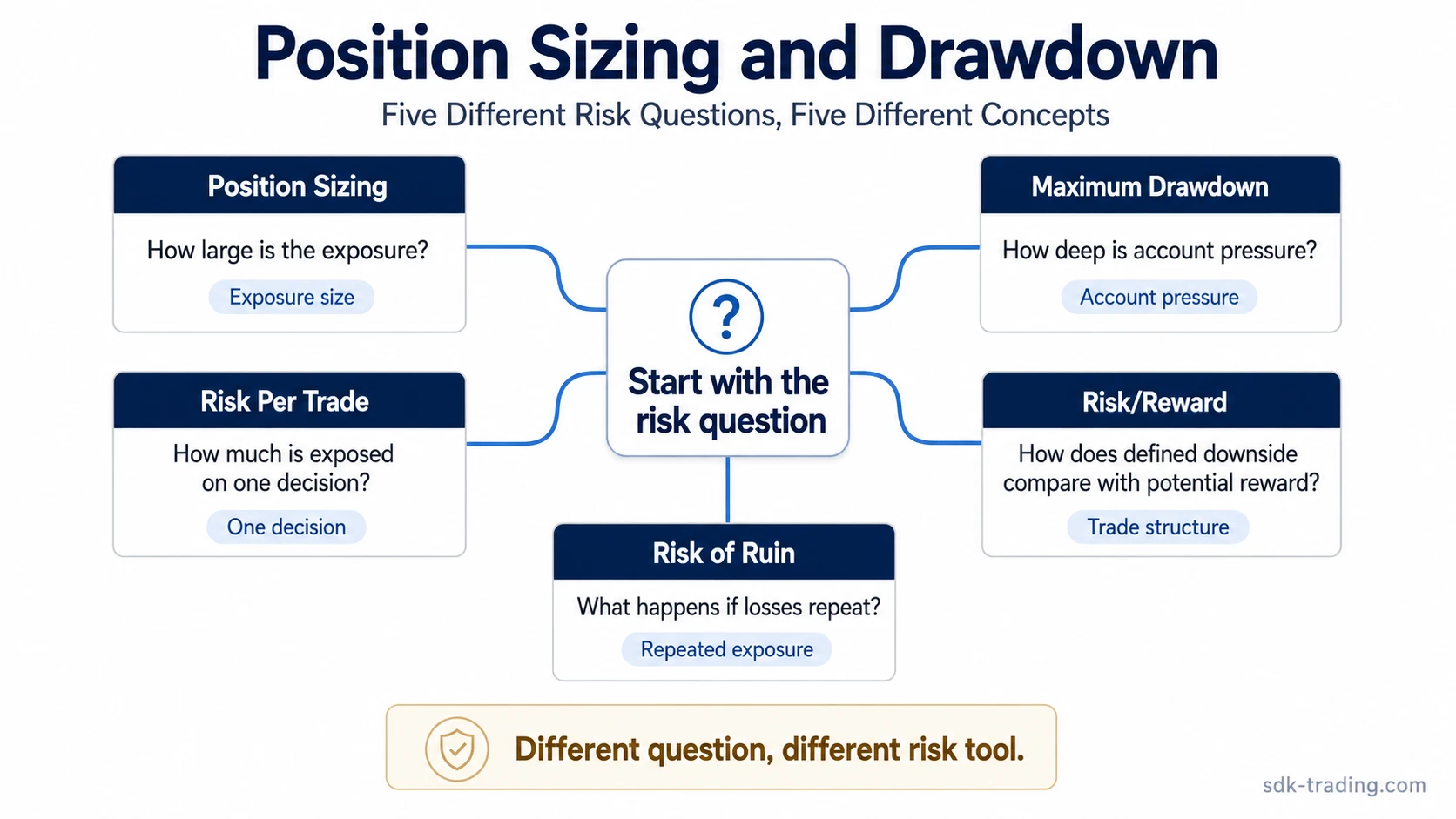

Which Risk Question Are You Trying to Solve?

The same trading plan can raise several different risk-management questions. Treating all of them as “position sizing” creates confusion because each concept has a different job.

| Risk question | Concept | What it separates |

|---|---|---|

| How large should the exposure be? | Position sizing | Account size, volatility, stop distance, and planned risk budget. |

| How much can the account decline before recovery becomes difficult? | Maximum drawdown | Peak-to-trough decline, recovery burden, and account volatility. |

| How much is lost if one trade reaches its predefined risk boundary? | Risk per trade | Position size, stop distance dependency, and the amount exposed on one decision. |

| Is the potential reward large enough relative to defined risk? | Risk/reward ratio | Trade structure, potential reward, and defined downside. |

| What happens if repeated losses compound? | Risk of ruin | Risk compounding, repeated exposure, and survival risk. |

Position Size Is Not the Same as Risk Per Trade

Position size describes the amount of exposure. Risk per trade describes the amount that can be lost if the trade reaches its planned risk boundary. Those two values can diverge because stop distance, volatility, and instrument behavior change how much risk is attached to the same nominal size.

A larger position with a narrow stop can expose the account differently from a smaller position with a wide stop. The better comparison is not size alone, but size relative to the risk boundary and account risk budget.

Practical distinction: position size answers “how much exposure is open?” while risk per trade answers “how much account equity is at risk if this specific trade fails?”

Drawdown Is Not Just a Single Losing Trade

Drawdown is broader than one loss. It measures decline from a prior account high to a later low. That makes it an account-level concept rather than a single-trade concept.

The recovery burden rises as drawdown deepens because a larger percentage gain is needed to return to the prior equity high. This is why drawdown tolerance must be considered before increasing position risk. A trade can have a defined risk boundary and still be too large if repeated losses would create account volatility that the plan cannot absorb.

Risk/Reward and Risk of Ruin Belong to Different Decisions

Risk/reward ratio evaluates the structure of one trade idea. It compares defined downside with potential upside. That does not automatically answer whether the account can survive a sequence of losses.

Risk of ruin belongs to repeated exposure. It looks at how risk compounds across many decisions. A trade can appear attractive on a reward/risk basis while still being unsuitable if the same position risk is repeated too aggressively during a losing period.

Boundary: reward/risk can describe one setup, but it does not replace position sizing, drawdown tolerance, or survival analysis across repeated trades.

Common Misreads

Risk-management mistakes often come from using one concept to answer a different concept’s question.

| Misread | Safer interpretation |

|---|---|

| Treating a larger account as automatic permission for larger risk. | Account size matters, but position risk still has to fit stop distance, volatility, and drawdown tolerance. |

| Using the same fixed size across different market conditions. | The same size can create different account volatility when price range, liquidity, or stop distance changes. |

| Reading reward/risk as survival math. | Reward/risk describes one trade structure. Survival depends on repeated exposure, loss sequences, and risk compounding. |

| Treating drawdown tolerance as emotional comfort only. | Drawdown tolerance also reflects recovery burden, account volatility, thesis duration, and the plan’s ability to continue after losses. |

Where to Go Next

The next concept depends on the exact risk question. A sizing problem, a drawdown problem, a reward/risk problem, and a survival-risk problem each need a different explanation.

| If the question is… | Use this concept | Best next explanation |

|---|---|---|

| How much exposure should a trade carry? | Position sizing | position sizing in trading |

| How deep can account decline become before recovery becomes difficult? | Maximum drawdown | maximum drawdown |

| How much is exposed on one trade decision? | Risk per trade | risk per trade |

| How does defined downside compare with potential reward? | Risk/reward | risk/reward ratio |

| What happens when losses repeat and compound? | Risk of ruin | risk of ruin |

FAQ

Is position sizing the same as drawdown control?

No. Position sizing controls exposure before and during a trade. Drawdown control looks at the account-level pressure created when losses reduce equity from a prior high.

Can a small position still create large risk?

Yes. A small nominal position can still create meaningful account risk if the stop distance is wide, volatility is high, or repeated losses compound against the same risk budget.

Does a strong risk/reward ratio prevent drawdown?

No. Risk/reward describes the structure of one trade idea. Drawdown depends on realized losses, position risk, repeated exposure, and account recovery burden.