Risk per trade is the predefined amount or percentage of account equity a trader is willing to lose on one trade if the trade reaches its invalidation boundary. It is not the same as the full position value. A position can use more capital than the amount actually accepted as loss if the boundary is reached.

Core idea: risk per trade defines the loss boundary for one decision. Position size, price distance, volatility, instrument behavior, and execution uncertainty determine how that boundary is translated into actual exposure.

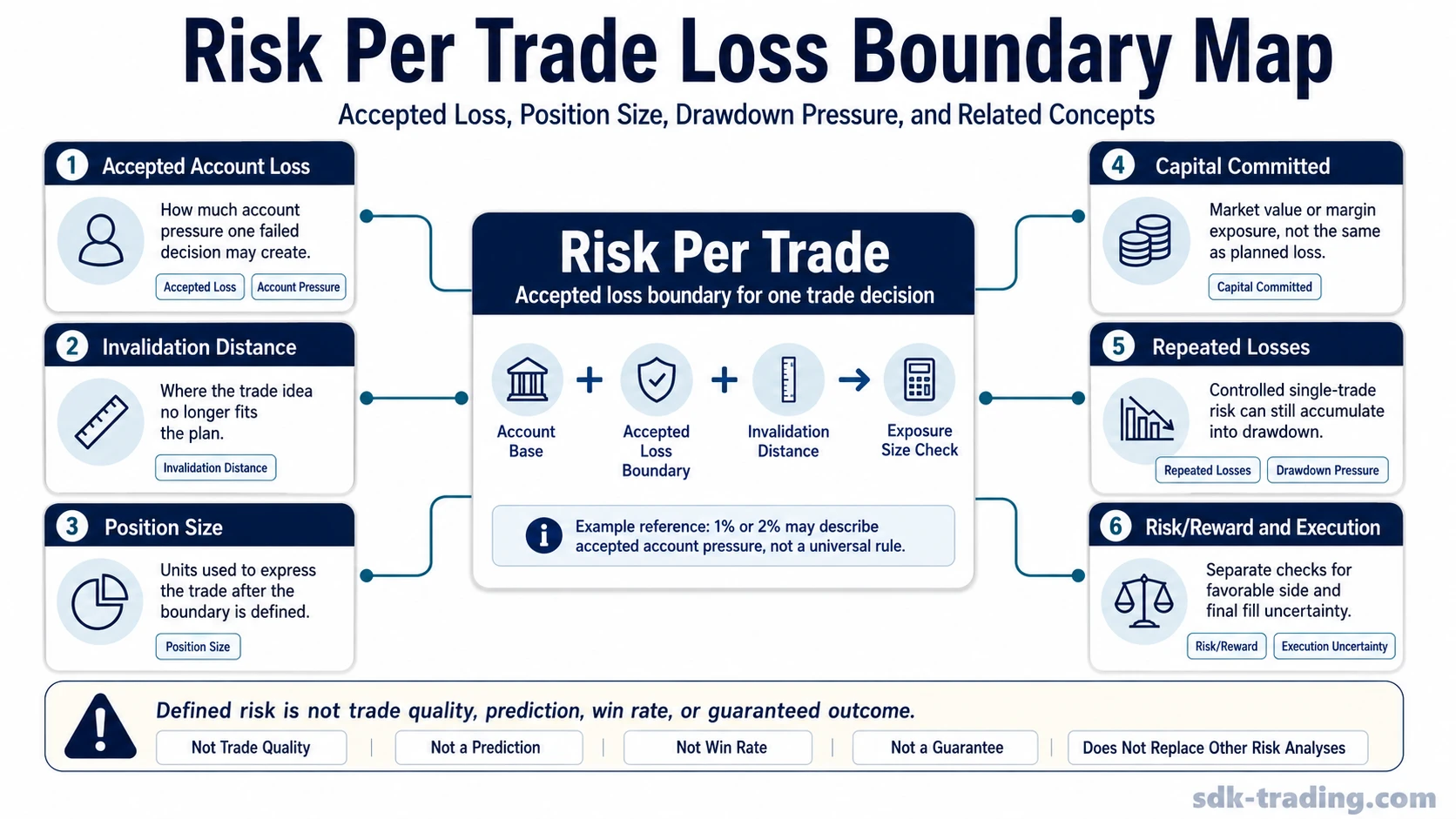

The common mistake is starting with a percentage before defining what the percentage controls. A 1% or 2% figure can describe the accepted account loss, but it does not explain whether the position is too large, whether the invalidation boundary is logical, whether repeated losses are survivable, or whether the trade has a favorable structure.

What Risk Per Trade Means

Risk per trade measures the planned account loss for a single trade idea. If an account is $10,000 and the accepted loss boundary is 1%, the planned account risk is $100. That $100 is the risk amount, not necessarily the amount invested or the market value of the position.

The boundary usually connects four inputs: account base, accepted loss, trade-level invalidation, and the exposure needed to express the idea. The account base sets the reference amount. The accepted loss defines how much account pressure one failed decision may create. The invalidation boundary marks where the idea no longer fits the trader’s plan. Position size converts those inputs into shares, contracts, lots, or units.

Useful distinction: risk per trade answers “how much account loss is accepted if this trade fails?” It does not answer “how much capital is used?” or “is this a good trade?”

Risk Per Trade vs Position Size

Risk per trade and position size are connected, but they are not interchangeable. Risk per trade is the allowed-loss decision. Position size is the exposure amount that results after the trader considers the distance between entry and invalidation, the instrument’s unit value, and the amount of account loss being accepted.

Two trades can use the same position value and still carry different risk per trade. If one trade has a narrow invalidation distance and another has a wider invalidation distance, the same capital commitment can produce different planned loss boundaries. The reverse can also happen: two trades can share the same risk per trade while requiring different position sizes.

| Concept | What it controls | Common confusion |

|---|---|---|

| Risk per trade | The accepted loss on one trade if the invalidation boundary is reached. | Confusing the loss boundary with the full amount invested. |

| Position size | The number of shares, contracts, lots, or units used to express the trade. | Assuming a larger position always means larger account risk. |

| Capital committed | The market value or margin exposure tied to the position. | Treating total exposure as the same thing as planned loss. |

| Invalidation distance | The gap between the trade expression and the level where the idea no longer fits the plan. | Choosing size before knowing what boundary is being accepted. |

For a fuller exposure-size process, position sizing explains how the accepted loss boundary becomes actual market exposure.

Why the 1% or 2% Rule Is Only a Reference Point

The 1% risk rule and 2% risk rule are common examples because they express risk as a simple account percentage. They are easier to compare than raw currency amounts. A $100 planned loss can mean something very different on a $5,000 account than on a $100,000 account, while a percentage keeps the account-pressure reference visible.

That does not make any fixed percentage universally correct. The better test is whether the accepted loss fits the account, the trader’s process, the instrument’s behavior, the expected variation in outcomes, and the number of similar decisions likely to occur. A fixed percentage can still create pressure if several trades fail in sequence or if open exposure becomes too concentrated.

Boundary limitation: a percentage rule controls planned account pressure per trade. It does not validate the trade idea, improve win rate, remove execution uncertainty, or prove that the position size is appropriate for the surrounding market conditions.

Simple Risk Per Trade Example

Consider an account where the trader accepts a $100 loss on one trade. If the trade idea fails at a boundary that is $2 away from the planned entry area, the exposure calculation would be different from a trade where the failure boundary is $5 away. The accepted loss can be the same, but the position size needed to stay inside that boundary changes.

Illustrative scenario: a trader accepts $100 of risk on one trade. A tighter invalidation distance allows more units before the $100 boundary is reached. A wider invalidation distance allows fewer units before the same $100 boundary is reached. The risk per trade stays constant, while the position size changes.

| Input | Scenario A | Scenario B | What changes |

|---|---|---|---|

| Accepted account loss | $100 | $100 | The planned risk per trade is the same. |

| Distance to invalidation | $2 per unit | $5 per unit | The wider boundary requires fewer units. |

| Illustrative unit count before the boundary | 50 units | 20 units | Position size changes to keep the same loss boundary. |

| Main distinction | The loss boundary and the exposure amount are connected, but they are not the same decision. | ||

This example is conceptual. Actual results can differ from the illustration because fills, gaps, liquidity, order type, fees, leverage, and instrument rules may change the final loss.

How Risk Per Trade Connects to Drawdown

Risk per trade affects drawdown because repeated losses accumulate. A small accepted loss on one trade can become meaningful account pressure when several decisions fail close together. The percentage does not need to be large for repeated exposure to matter.

This is where trade-level risk and account-level decline must stay separate. Risk per trade defines one loss boundary. Maximum drawdown describes the account decline from a prior peak to a later trough. A trader can keep each trade small and still experience drawdown if the sequence of outcomes is unfavorable.

Risk per trade also differs from risk of ruin, which deals with repeated-exposure survival rather than one trade’s planned loss boundary. A single-trade boundary helps control account pressure, but it does not replace broader survival analysis.

Risk Per Trade, Risk/Reward, and Expectancy

Risk per trade defines the downside boundary for one decision. Risk/reward compares that downside boundary with the potential favorable movement being considered. A trade can have a small planned loss and still be unattractive if the favorable side is too limited, unclear, or dependent on unrealistic movement.

The risk/reward ratio is therefore a separate concept. It does not replace risk per trade, and risk per trade does not replace it. One controls accepted loss. The other compares accepted loss with potential favorable movement.

Expectancy adds another layer. It depends on the distribution of wins and losses across many decisions, not only on the risk amount chosen for one trade. A clean risk boundary can make losses more defined, but it cannot make an unprofitable process profitable by itself.

Common Mistakes When Setting Risk Per Trade

| Mistake | Why it creates risk | Cleaner distinction |

|---|---|---|

| Choosing a percentage first | The percentage may look controlled while the invalidation boundary remains unclear. | Define what trade failure means before converting that boundary into size. |

| Confusing position value with capital at risk | A large position may have a smaller planned loss, while a smaller position may still carry too much risk if the boundary is wide. | Separate market exposure from the loss accepted if the trade fails. |

| Treating 1% or 2% as universal | A benchmark percentage ignores account tolerance, strategy behavior, volatility, and repeated exposure. | Use percentages as reference points, not automatic rules. |

| Ignoring drawdown sequence | Several controlled losses can still create meaningful account decline. | Evaluate the pressure of repeated losses, not only one isolated trade. |

| Assuming defined risk proves trade quality | A controlled loss boundary says nothing by itself about favorable movement, edge, or execution quality. | Risk control can define the downside, but it does not prove that the idea has favorable structure. |

When Risk Per Trade Is Not Enough

Risk per trade is incomplete when it is used alone. A trader can define the loss on one trade but still ignore concentration, correlated positions, open exposure, slippage, gap risk, changing volatility, or a string of losses. The boundary controls one decision, not the whole account environment.

It is also incomplete when the boundary is chosen only to fit the desired position size. If the invalidation distance is moved simply to allow more units, the calculation may look controlled while the trading premise becomes weaker.

Final boundary check: risk per trade is a risk-control input, not a trade-quality test. It should be read alongside position sizing, drawdown tolerance, risk/reward, expectancy, and execution uncertainty before the account-level impact is understood.

FAQ

Is risk per trade the same as position size?

No. Risk per trade is the accepted loss boundary for one trade. Position size is the number of shares, contracts, lots, or units used to express that trade. Position size is partly derived from the accepted loss boundary, but the two concepts are not identical.

Is the 1% risk rule always correct?

No. A 1% rule is a common reference point, not a universal answer. The appropriate risk boundary depends on account size, strategy behavior, volatility, drawdown tolerance, repeated exposure, and execution uncertainty.

Can risk per trade prevent drawdown?

No. Risk per trade can limit the planned loss on one trade, but repeated losses can still create drawdown. Drawdown depends on the sequence and size of account declines, not only one trade’s accepted loss.

How does risk per trade relate to risk/reward?

Risk per trade defines the downside boundary. Risk/reward compares that downside boundary with potential favorable movement. A defined loss boundary does not automatically make the favorable side attractive.