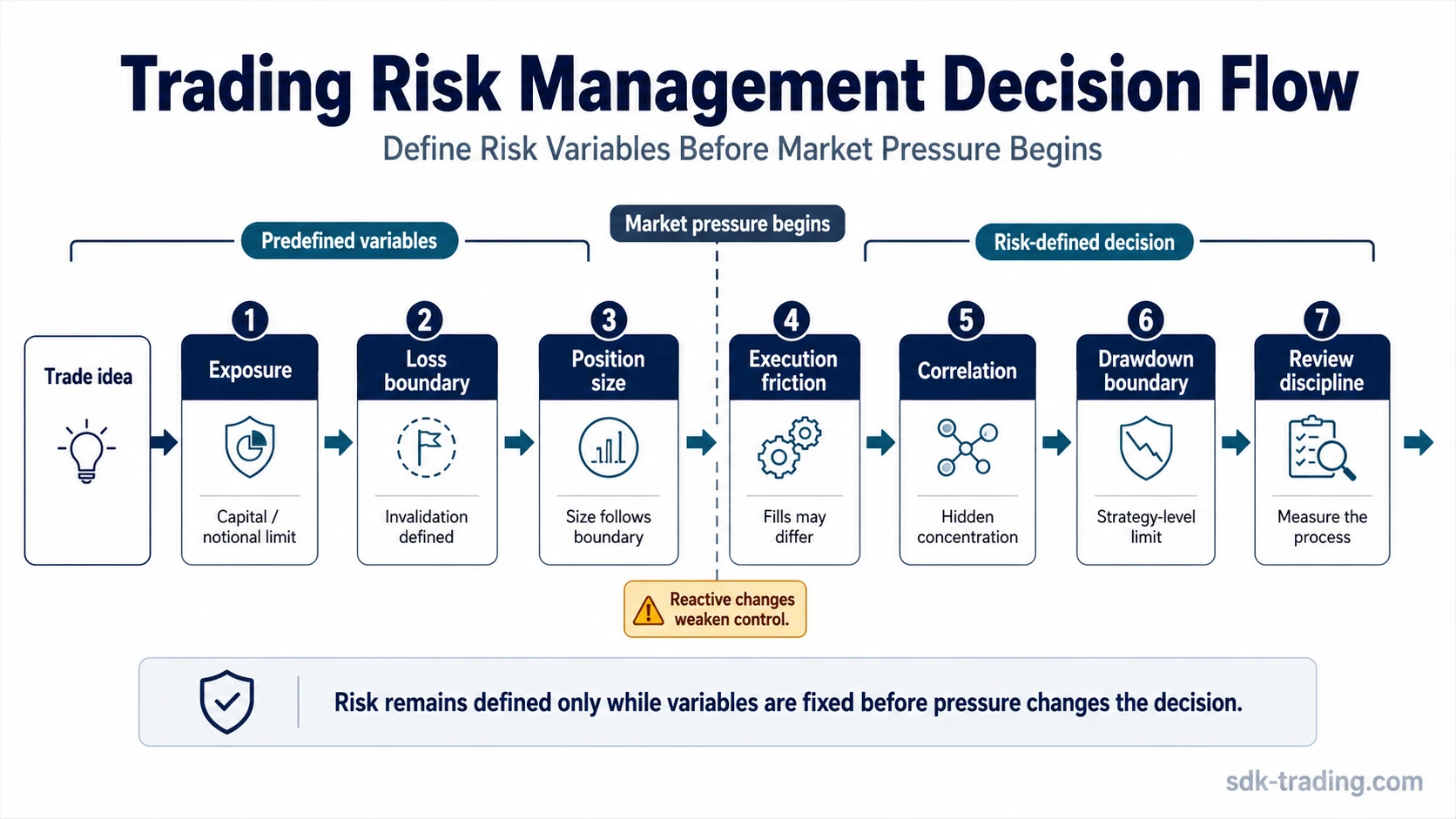

A trading risk management strategy is a framework for deciding exposure, loss boundaries, position size, execution risk, and review rules before market pressure begins.

The framework separates a trade idea from a risk-defined decision by checking exposure first, then loss boundary, position size, execution friction, correlation or leverage, drawdown limits, and review discipline.

Definition: A trading risk management strategy organizes the risk variables that must be fixed before execution: exposure, loss boundary, position size, execution friction, correlation, leverage, drawdown tolerance, and review discipline.

Broader risk management in trading explains the full concept of controlling financial exposure. A strategy turns that concept into a repeatable decision process so risk is not improvised after a position becomes emotionally difficult.

Key Points

- A trading risk management strategy defines risk variables before execution, not after pressure starts.

- Position size depends on the loss boundary, not only on account size or confidence.

- A stop-loss and take-profit can support the framework, but they do not replace the whole process.

- Slippage, leverage, and correlated exposure can make planned risk different from expected risk.

- Review discipline matters because risk control weakens when review becomes justification instead of measurement.

What a Trading Risk Management Strategy Controls

The strategy controls the decision points that can change risk before, during, and after execution. The main issue is not whether a trade idea is interesting. The issue is whether the idea can be expressed with defined exposure, a defined loss boundary, a defined position size, and a defined review process.

A clean framework treats risk as a permission condition. If the loss boundary cannot be defined, position size cannot be calculated responsibly. If execution friction can materially change the expected loss, the planned risk is incomplete. If correlation or leverage creates hidden exposure, the single-position view may underestimate total risk.

Framework note: The strategy does not predict whether a trade will work. It defines the conditions under which the idea remains risk-defined.

The Core Risk Variables

Each risk variable answers a different decision question. Treating one variable as the whole strategy creates blind spots. A stop can define a loss boundary, but position size, execution friction, and total exposure still decide whether that boundary is usable.

| Risk variable | Decision question | Failure mode | Framework role |

|---|---|---|---|

| Exposure | How much capital or notional value is at risk? | The trade looks small but creates excessive total exposure. | Sets the outer boundary before deeper sizing decisions. |

| Loss boundary | Where is the idea no longer valid? | The trader changes the boundary after pressure starts. | Defines the point where the risk premise has failed. |

| Position sizing in trading | How large can the position be relative to the loss boundary? | Size is chosen before invalidation is clear. | Connects account risk, stop distance, and drawdown tolerance. |

| Stop-loss | How can a predefined loss boundary be expressed? | The stop becomes an emotional reference instead of a risk-control tool. | Supports the loss boundary without replacing the full strategy. |

| Take-profit | How will favorable movement be evaluated before the trade begins? | The trader treats a planned exit level as a prediction instead of a planning boundary. | Connects favorable-outcome planning with risk acceptance without guaranteeing that price will reach the level. |

| Execution friction | Can fills differ from the planned price? | The planned loss assumes execution conditions that do not hold. | Adjusts expected risk for real execution conditions. |

| Correlation and leverage | Does the position duplicate existing risk? | Separate trades behave like one larger exposure. | Prevents hidden concentration across related positions. |

| Drawdown boundary | When does the strategy reduce or pause risk? | Losses are treated as isolated events instead of process feedback. | Controls strategy-level risk, not only single-trade risk. |

| Review discipline | What will be measured after the outcome? | Review becomes a story that defends the decision. | Separates process quality from outcome bias. |

A Scenario Tree for Risk Decisions Under Pressure

The scenario tree begins before execution. Its purpose is to keep each risk variable fixed enough to evaluate the trade idea without letting stress change the rules midstream.

- Trade idea: The market presents a potential setup, but the idea is only an observation until risk can be defined.

- Exposure cap: The trader checks whether the position would add acceptable total exposure or duplicate existing correlated risk.

- Loss boundary: The idea needs a clear invalidation area before size can be chosen.

- Size calculation: Position size is adjusted to the distance between the intended execution area and the loss boundary.

- Execution risk: The trader checks whether spreads, gaps, liquidity, or fast movement could change the planned loss.

- Correlation check: The position is compared with other open or planned positions that may respond to the same market driver.

- Drawdown limit: The trade is checked against strategy-level risk limits, not only the single-position loss.

- Review rule: The trader defines what will be reviewed later: boundary quality, sizing discipline, execution quality, and adherence to process.

- Failure condition: If any risk variable must be changed after pressure begins, the strategy has moved from controlled to reactive.

Boundary: A scenario tree is not a trade signal. It is a control process for deciding whether the risk variables are defined enough to make the idea process-valid.

How Position Size, Stop-Loss, Take-Profit, and Risk/Reward Interact

Position size should follow the loss boundary. If the distance to invalidation is wider, the same position size creates a larger potential loss. If the distance is narrower, the position may appear easier to control, but only if the boundary is meaningful rather than arbitrary.

A take-profit can help define how favorable movement will be evaluated, but it should not be treated as a promise that the market will reach a planned level. It is part of the planning structure, not evidence that the trade is favorable by itself.

The risk-reward ratio connects planned loss to planned reward, but the ratio is incomplete unless the setup has a definable invalidation point, realistic execution assumptions, and a review rule for whether the process was followed.

Practical distinction: Risk/reward describes planned asymmetry. Risk management strategy decides whether that asymmetry is usable after size, execution friction, correlation, and drawdown are considered.

Execution Risk and Slippage

Execution risk matters because planned risk is based on assumed prices, but real fills can differ. Slippage is one of the clearest examples: a trader may define a loss boundary correctly, yet still face a larger realized loss if the market moves through the expected execution area.

The same friction can affect entry assumptions, stop execution, and exit planning, so it should be considered before size and risk/reward are treated as stable.

This is especially important when spreads widen, liquidity thins, price gaps, or volatility accelerates. The strategy should account for the possibility that the planned execution price and the realized execution price are not identical.

Execution boundary: A strategy that ignores execution friction may look controlled on paper while leaving real risk undefined in fast or thin conditions.

When a Risk Management Strategy Breaks Down

A risk management strategy breaks down when predefined variables become flexible after market pressure begins. The failure is usually not one isolated mistake. It is the moment when size, loss boundary, exposure, or review criteria begin changing to defend the trader’s opinion instead of controlling risk.

| Breakdown pattern | What changes under pressure | Why it weakens the strategy |

|---|---|---|

| Loss boundary moves | The invalidation area is adjusted after price moves unfavorably. | The original risk premise is no longer being measured. |

| Size no longer matches risk | The position remains large even though the loss boundary has widened. | The planned risk and actual exposure separate. |

| Correlation is ignored | Several positions depend on the same market driver. | Total exposure becomes larger than it appears from each trade alone. |

| Leverage expands the error | A small adverse move has an outsized effect on account risk. | The strategy becomes sensitive to normal market noise. |

| Review becomes justification | The trader explains the outcome instead of measuring the decision process. | The same risk error can repeat because it is not identified clearly. |

- Define invalidation before size: Size has no stable meaning until the loss boundary is known.

- Separate planned risk from execution risk: Fast markets, wide spreads, and thin liquidity can change the effective loss.

- Review decisions, not stories: The review should measure whether the framework was followed.

Trading Risk Management Strategy Example in Context

Price advances into a prior resistance area and briefly trades above it, but the move does not yet prove that the setup is usable. Before execution, the trader defines the loss boundary, checks whether the required position size fits that boundary, and considers whether the same market driver already appears in other positions.

If the loss boundary is clear, size can be reduced or adjusted so the planned loss remains inside the allowed risk limit. If the boundary is unclear, the idea remains only an observation. If spreads are wide or price is moving quickly, execution friction may change the expected loss enough to make the idea structurally weak.

The useful distinction is not the touch of resistance itself. The idea becomes risk-defined only if the boundary, size, execution assumptions, and review rule are fixed before pressure begins. If those variables have to be widened or reinterpreted after price moves, the decision process has already become reactive.

Common Risk Management Strategy Mistakes

Most risk management mistakes come from treating one control as if it solves every risk variable. A stop, ratio, or percentage limit can help, but the strategy still needs a full process for exposure, execution, correlation, drawdown, and review.

| Mistake | Safer interpretation |

|---|---|

| Treating a stop-loss as the whole strategy | A stop can define a boundary, but size, execution risk, and total exposure still determine the real risk. |

| Using a fixed percentage without context | A percentage limit needs a meaningful loss boundary and drawdown rule to be useful. |

| Ignoring slippage and market conditions | Execution friction can change planned risk even when the written plan looks precise. |

| Sizing before invalidation is defined | Position size should be calculated after the loss boundary is known. |

| Reviewing only the outcome | Process review should check whether risk variables were defined and followed, not only whether the trade won or lost. |

FAQ

What should a trading risk management strategy include?

It should include exposure limits, a loss boundary, position size logic, execution-risk assumptions, correlation checks, drawdown limits, and a review process.

Is a stop-loss enough for risk management?

No. A stop-loss can support the loss boundary, but position size, slippage, correlation, leverage, drawdown, and review discipline still affect total risk.

How does position size fit into a risk management strategy?

Position size translates the loss boundary into account-level risk. It should be calculated after the invalidation area is defined, not before.

When does a risk management strategy become reactive?

It becomes reactive when the trader changes size, loss boundary, exposure, or review criteria after market pressure begins instead of following predefined conditions.

How can slippage change planned trading risk?

Slippage can make the realized execution price worse than the planned price, which can increase the loss beyond the original framework.