Slippage is the difference between the price a trader expects, requests, or sees quoted and the actual price where an order is filled. In trading, that gap belongs to execution risk because market conditions can change between the decision to trade and the completed fill.

Slippage means expected price versus actual fill price. If the expected price is 100.00 and the order fills at 100.08, the 0.08 difference is slippage. The same idea applies in the opposite direction when the final fill is better than the expected price.

Slippage is not the same as a broker fee, commission, or normal spread. It is the execution gap created when available liquidity, order type, market speed, or price movement changes the fill before the order is completed.

What Is Slippage in Trading?

In trading, slippage occurs when the final execution price differs from the price the trader expected at the moment the order was sent. The expected price can be a quoted price on the screen, a requested order price, or the price used in a risk calculation before execution.

The boundary is the completed fill. A price can appear available before the order reaches the market, but the actual fill depends on the liquidity available at execution time. When the fill happens at a different price, the difference becomes slippage.

Execution boundary: slippage begins only when there is a completed fill at a different price. If the order is rejected or never fills, the issue is not slippage. It is a no-fill or rejected-order condition.

How Slippage Happens

Slippage usually appears when the market cannot fill the full order at the expected price. That can happen because the price moves quickly, available depth is thin, the order is large relative to nearby liquidity, or the order reaches the market after conditions have changed.

A market order is most exposed to this problem because it prioritizes getting filled over controlling the exact fill price. If there is not enough available liquidity at the best visible price, the remaining quantity can fill at the next available prices.

| Cause | How it can create slippage |

|---|---|

| Fast price movement | The quoted price changes before the order is fully executed. |

| Low liquidity | There may not be enough available size at the expected price. |

| Shallow market depth | The order can move through several price levels before completion. |

| Spread widening | The executable price can move farther from the visible reference price. |

| Execution delay | Market conditions can change between order submission and completed execution. |

| Order size | A larger order may consume available liquidity at more than one price. |

| Market gaps | The next available price can be materially different from the last visible price. |

| Off-hours or weekend movement | When trading resumes, the first executable price may differ from the prior reference price. |

Positive vs Negative Slippage

Slippage can be negative or positive. Negative slippage means the fill is worse than expected. Positive slippage means the fill is better than expected. The direction depends on whether the final execution price improves or worsens relative to the trader’s expected price.

| Type | Meaning | Simple example |

|---|---|---|

| Negative slippage | The order fills at a worse price than expected. | A buy order expected near 100.00 fills at 100.08. |

| Positive slippage | The order fills at a better price than expected. | A buy order expected near 100.00 fills at 99.96. |

| No slippage | The order fills at the expected price. | A quoted 100.00 price fills at 100.00. |

Positive slippage does not make execution risk disappear. It only means that one fill improved relative to the expected price. The same execution process can still produce worse fills under different liquidity or volatility conditions.

Slippage vs Spread, Fees, and Rejected Orders

Slippage is often confused with other trading costs or execution outcomes. The clean distinction is that slippage compares the expected price with the actual fill price. Other costs or failures have different mechanics.

| Concept | What it measures | How it differs from slippage |

|---|---|---|

| Slippage | The gap between expected price and actual fill price. | It appears only after an order fills at a different price. |

| Spread | The difference between bid and ask prices. | Spread exists before execution; slippage is measured against the final fill. |

| Commission or fee | A direct charge for trading or platform use. | A fee is charged separately; slippage is embedded in the execution price. |

| Rejected order | An order that is not accepted or not executed. | No fill means no fill-price gap to measure as slippage. |

| Technical outage | A platform or connectivity failure. | An outage may affect execution, but it is not itself the fill-price difference. |

| Margin call | An account-pressure event caused by insufficient margin. | It concerns account requirements, while slippage concerns execution price versus expected price. |

Why Slippage Matters for Execution Risk

Slippage matters because planned risk can differ from realized execution. A trader may calculate risk using one expected price, but the actual fill can change the position’s entry price, cost basis, or realized exit condition.

This is especially important when the market is moving quickly or available liquidity is thin. The trade idea may be unchanged, but the execution conditions can alter the final price enough to change the practical risk boundary.

Execution tradeoff: slippage can sometimes be reduced or bounded, but it cannot be eliminated in every market condition without accepting another tradeoff. More price control can mean a higher chance of no fill, while more fill certainty can mean less price control.

Order Types and Slippage

Order type affects how much price control the trader requests and how much fill certainty the order seeks. That does not make one order type universally better. It only changes the execution tradeoff.

| Order context | Slippage relationship | Main limitation |

|---|---|---|

| Market order | Prioritizes execution, so the fill can move through available liquidity. | Higher fill certainty can come with less price control. |

| Limit order | Sets a price boundary for the fill. | The order may not fill if the market does not trade at the limit price. |

| Stop-loss order | Can trigger during fast movement and then execute at the next available price, depending on order design and venue rules. | The stop level is not always the final execution price. |

| Stop-limit order | Adds a limit boundary after the stop condition is triggered. | The limit can prevent a worse fill, but it can also leave the order unfilled. |

The key distinction is price certainty versus fill certainty. Slippage is the visible result when the final fill differs from the expected execution price.

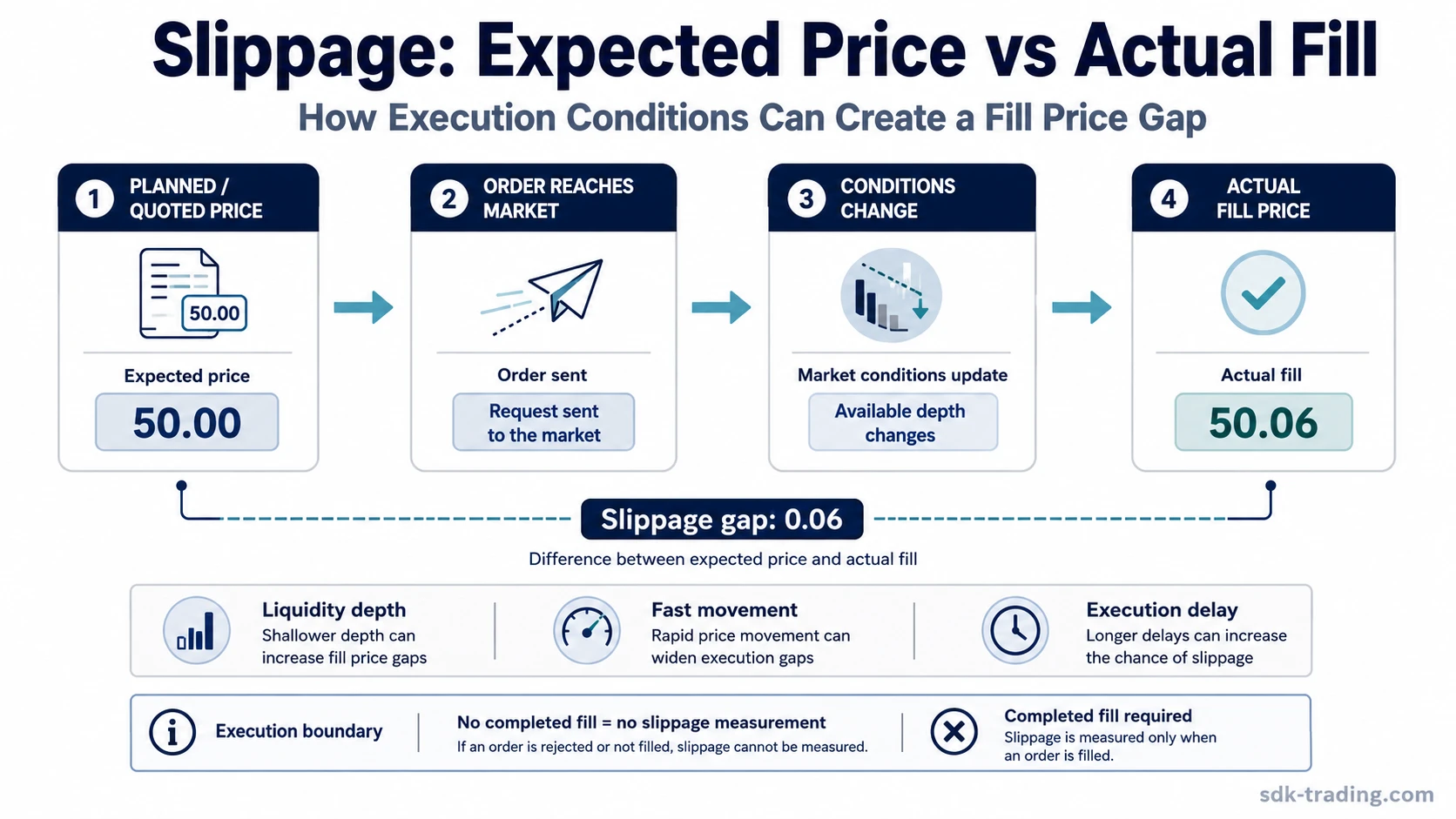

Practical Slippage Example

A trader sees a quoted price of 50.00 and sends an order. Only part of the available liquidity remains at 50.00 by the time the order reaches the market, so the final average fill is 50.06. The 0.06 difference between the expected price and the actual fill is slippage.

The same scenario can become larger in a fast market. If price moves quickly or depth disappears near the quoted price, the actual fill can move farther from the expected level before execution completes.

| Input | Value |

|---|---|

| Expected price | 50.00 |

| Actual fill price | 50.06 |

| Slippage amount | 0.06 |

Real execution can also involve partial fills, changing spreads, venue rules, or average prices across several fills.

Slippage in Crypto Markets

Slippage in crypto follows the same core logic: expected execution price versus actual fill price. The difference is that crypto markets can vary widely by venue, liquidity depth, trading pair, order routing, and market speed.

Some crypto interfaces also show slippage tolerance settings. That setting is not slippage itself. It is a boundary for how much execution price difference the user is willing to allow before the transaction or order fails under that venue’s rules.

Crypto context: slippage can be more visible in thin trading pairs, fast market moves, or fragmented liquidity conditions. The core measurement remains the gap between expected price and actual fill price.

Common Slippage Mistakes

Slippage is easiest to misunderstand when it is treated as a single fixed cost. In reality, it is a variable execution outcome that depends on the order, market, venue, and available liquidity at the time of execution.

| Mistake | Cleaner interpretation |

|---|---|

| Assuming the quoted price is guaranteed | A quote is a reference point. The final fill still depends on executable liquidity. |

| Treating slippage as a broker fee | Fees are charged separately. Slippage is reflected in the execution price. |

| Ignoring order size | A larger order can consume more than one price level. |

| Assuming limit orders always solve slippage | A limit can control price, but it may also leave the order unfilled. |

| Measuring slippage without a completed fill | Without a fill, there is no actual fill price to compare against the expected price. |

FAQ

What is slippage in trading?

Slippage in trading is the difference between the expected price of an order and the actual price where the order is filled.

Is slippage always bad?

No. Slippage can be negative when the fill is worse than expected, or positive when the fill is better than expected.

Is slippage the same as spread?

No. Spread is the difference between bid and ask prices, while slippage is the gap between the expected execution price and the final fill price.

Is slippage a trading fee?

No. A trading fee is a separate charge, while slippage is the difference between the expected price and the actual fill price after execution.

Can slippage be avoided completely?

Not in every market condition. Some order settings can add price boundaries, but stronger price control can also increase the chance that the order does not fill.

How does slippage affect stop-loss orders?

A stop-loss order can trigger at a selected level, but the final fill may occur at a different price when the market moves quickly or available liquidity changes.

What is slippage in crypto?

In crypto, slippage is still the gap between expected and actual execution price. It can be affected by liquidity depth, venue conditions, network timing, and slippage tolerance settings.