Execution risk in trading is the risk that the actual execution of a trade differs from the intended execution. The difference can appear through the price received, fill quality, timing, liquidity availability, partial fills, order-type behavior, market impact, or account pressure.

Definition: Execution risk is the gap between intended trade execution and actual trade outcome. It does not describe whether a market idea is correct. It describes whether the trade could be carried out under the intended conditions.

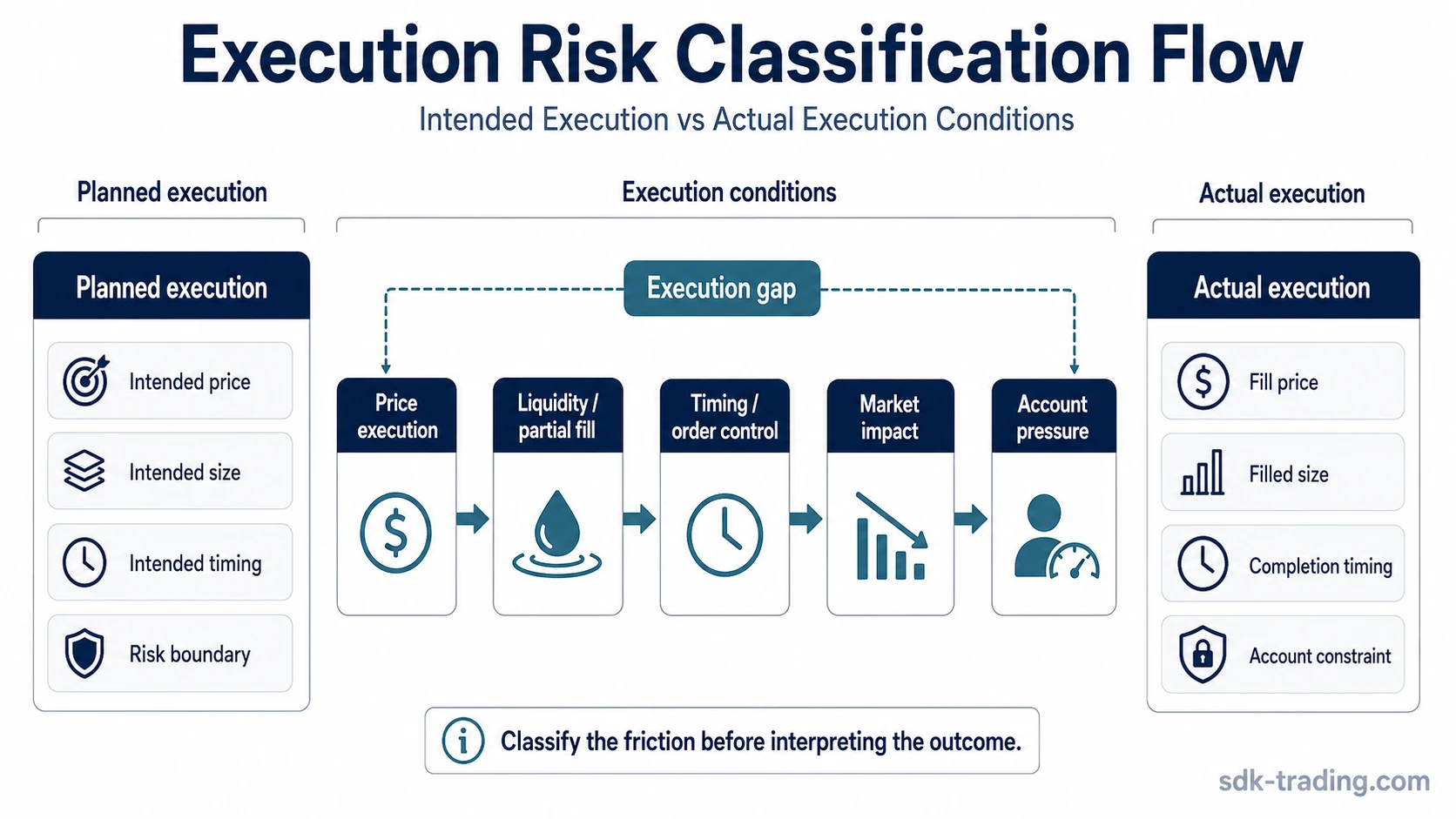

A trader may plan around a specific price, size, timing window, and risk boundary, but live market conditions can change the result before the order is fully processed. Thin liquidity, fast movement, delayed execution, limited depth, or forced account constraints can all make the final execution different from the original plan.

Key Points

- Execution risk concerns the difference between intended execution and actual execution.

- The main categories include price movement, liquidity, partial fills, timing friction, order-type behavior, market impact, and account-pressure constraints.

- Slippage is one execution-risk outcome, but execution risk is broader than price difference alone.

- A margin call belongs to the account-pressure side of execution risk, not to fill-price mechanics.

- The most useful first distinction is whether the problem came from price, liquidity, timing, order control, market impact, or account constraints.

What Execution Risk Means in Trading

Execution risk begins when the planned trade conditions and the actual market conditions do not match. The intended price may not be available, the available size may be smaller than expected, or the market may move before the order is completed.

The concept is especially important because execution quality can change the practical meaning of a trade idea. A setup may still look valid on a chart, but the actual fill can create a different risk profile if the price, size, timing, or available liquidity changes during execution.

Core distinction: Market analysis asks whether a trade idea makes sense. Execution risk asks whether that idea can be carried out near the intended conditions.

Why Intended and Actual Execution Can Differ

The intended execution is the trade condition a trader expects before interacting with the market. The actual execution is what happens after price, liquidity, timing, and order handling meet real market conditions.

Several frictions can create a gap between the two. Price can move while the order is being processed. Available liquidity can disappear or sit at a worse price. A large order can consume available depth. A price-control order can remain unfilled. A fast-execution order can fill away from the expected level.

| Execution factor | What can change | Why it matters |

|---|---|---|

| Expected price vs fill price | The final fill occurs away from the intended price. | The trade begins with a different risk and reward profile than planned. |

| Full fill vs partial fill | Only part of the intended size is executed. | The position may not match the planned exposure. |

| Speed vs price control | Fast execution may sacrifice price control, while strict price control may sacrifice completion. | The order type affects which execution risk is accepted. |

| Liquidity depth | Available size at the expected price is insufficient. | The trade may need to execute across multiple prices. |

| Delay or latency | The market changes between decision and execution. | The final execution may reflect a different market state. |

Main Execution Risk Areas

Execution risk is easier to classify when each friction is separated by the part of execution it affects. Some risks affect the price received. Others affect completion, size, timing, market impact, or account constraints.

| Execution-risk area | What can go wrong | Related execution concept |

|---|---|---|

| Price execution | The actual fill differs from the expected price. | slippage |

| Liquidity and partial fills | The market does not provide enough size at the intended price. | Liquidity depth, fill quality, and partial-fill behavior |

| Order-type behavior | The order prioritizes either speed or price control, but not both equally. | Order handling and price-control tradeoffs |

| Timing and processing friction | The market moves before execution is completed. | Latency, delay, platform, or processing conditions |

| Market impact | The order itself affects available liquidity or the next executable price. | Large-order execution and depth consumption |

| Account-pressure boundary | Account constraints force exposure changes under pressure. | margin call |

Execution Risk vs Slippage

Execution risk and slippage are related, but they are not identical. Slippage describes the price difference between the expected execution price and the actual fill price. Execution risk includes that price difference, but also includes other problems that can affect whether the trade is completed as intended.

A trade can have execution risk even when the final price difference is small. For example, an order may fill only partially, fill too late for the intended condition, or require a different size because market depth changed. Those are execution problems even if the price gap is not the main issue.

Boundary: Treating execution risk as only slippage makes the concept too narrow. Slippage is the price-result category. Execution risk also includes liquidity, fill completion, order behavior, timing friction, market impact, and account-pressure effects.

Execution Risk vs Margin Call

A margin call is not the same thing as a poor fill. It belongs to the account-pressure side of execution risk because it can force exposure changes when account equity, margin requirements, or leverage conditions no longer support the existing position.

The distinction matters because slippage is usually about execution price, while margin pressure is about whether the account can maintain exposure. Both can affect the final trade outcome, but they come from different mechanisms.

Boundary: Margin pressure should not be explained as a fill-quality problem. It is an account constraint that can change what a trader is able to hold or reduce under pressure.

Practical Execution Risk Scenario

Example: A trader plans around a price level where enough liquidity appears to be available. When the order reaches the market, the visible liquidity is smaller than expected, the price moves, and only part of the intended size is filled near the planned level. The execution problem is not one single issue. It combines price difference, liquidity depth, partial fill behavior, and timing friction.

The focus stays on execution conditions rather than prediction. The main question is not whether the market idea was right. The question is whether the trade could be executed with the intended price, size, timing, and account constraints still intact.

How to Classify an Execution Risk Problem

The first step is to identify which part of the execution changed. A price problem, a liquidity problem, a timing problem, and an account-pressure problem should not be treated as the same issue.

| Question | Likely risk area |

|---|---|

| Did the actual fill differ from the expected price? | Price execution |

| Was only part of the intended size completed? | Liquidity or partial-fill friction |

| Did the order complete after the relevant condition changed? | Timing or processing friction |

| Did the order type prioritize speed over price control, or price control over completion? | Order-type behavior |

| Did the order consume available depth and affect the next executable price? | Market impact |

| Did account constraints force exposure reduction? | Account-pressure boundary |

Separating these categories prevents one execution problem from being misread as another. A fill-price issue, a partial-fill issue, and an account-pressure issue can all affect the final outcome, but each requires a different interpretation.