Trading psychology is the way emotions, cognitive biases, pressure, and expectation shape trading decisions and execution behavior.

The label is useful only when it connects to observable plan deviation or process behavior. Fear, greed, regret, FOMO, or overconfidence may be present, but the practical question is whether that pressure changed the plan, distorted sizing, delayed action, triggered revenge trading, or weakened the decision record.

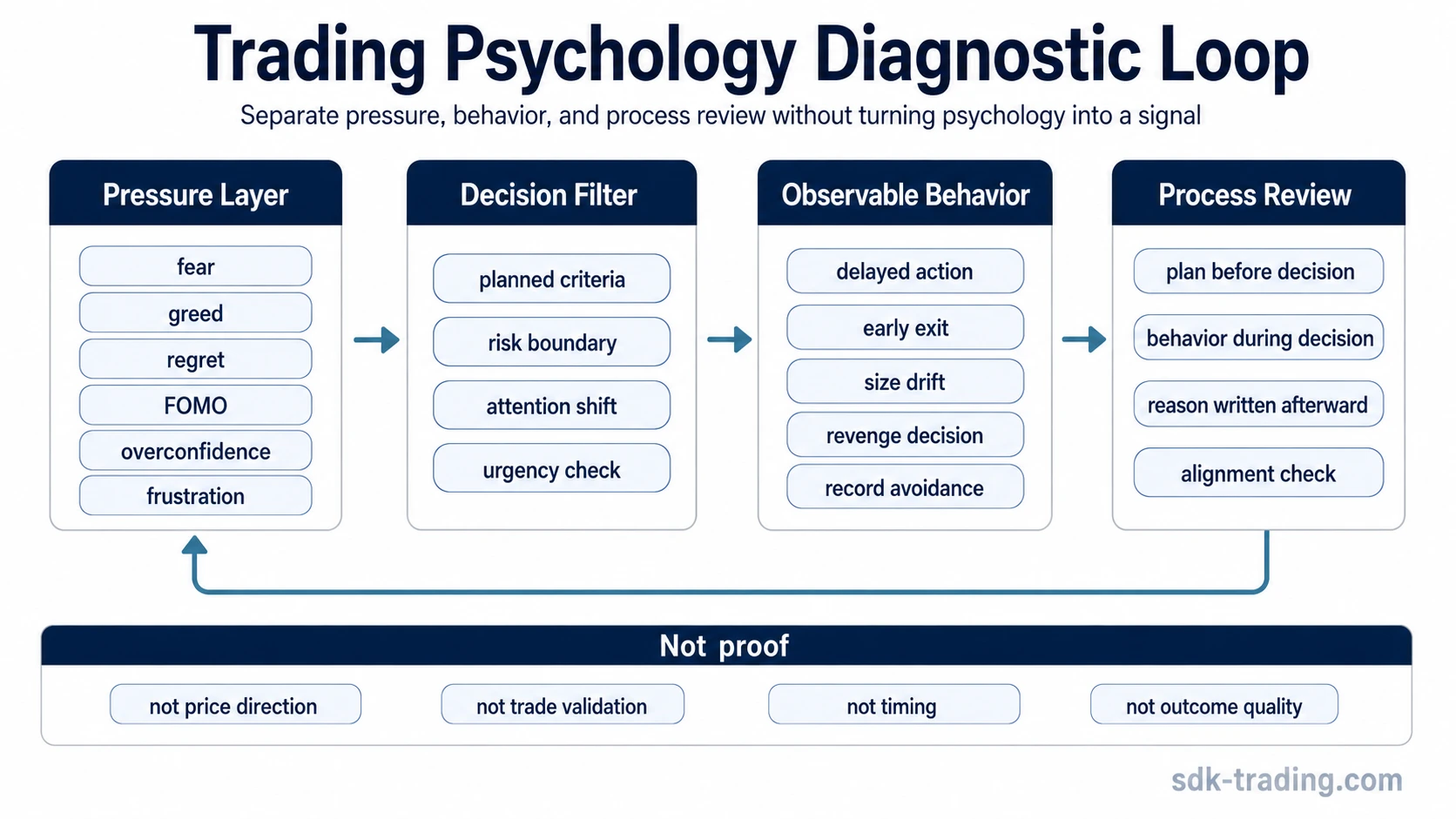

Definition: Trading psychology is a trader decision-process concept. It describes how emotional and cognitive pressure can influence interpretation, patience, execution, risk boundaries, and post-trade review. It is not a price signal, a trade validator, or proof that a market should move in any direction.

Key Points

- Trading psychology describes the pressure layer behind trading decisions, not a forecast of price movement.

- The strongest use is behavioral: compare what was planned with what was actually done.

- Emotion alone is not a process failure; behavior change is the evidence that matters.

- A losing outcome does not automatically prove poor psychology if the decision followed a defined process.

Trading Psychology Definition

Trading psychology belongs to the trader decision process. It includes emotional reactions such as fear, greed, frustration, regret, and urgency, as well as cognitive biases such as loss aversion, confirmation bias, recency bias, and overconfidence.

The same market information can lead to different decisions when risk, recent outcomes, or missed opportunities change the trader’s attention. A setup may look clear before a position is opened, then feel different after money is at risk, after a recent loss, or after several missed opportunities.

A useful process check does not judge the trade outcome first. It compares the decision with the planned criteria, checks whether risk boundaries were respected, and identifies whether pressure changed behavior before the decision was made.

Why Trading Psychology Changes Trading Decisions

Emotional pressure changes decisions by shifting attention. Fear can narrow attention toward loss avoidance. Greed can make risk boundaries feel less important. Regret can pull attention back to a missed move. FOMO can make incomplete evidence feel urgent. Overconfidence can make normal uncertainty look smaller than it is.

These reactions are not automatically mistakes. Pressure becomes more important when it changes execution behavior, such as chasing a move after the original plan was missed, increasing size after a loss, exiting before the planned condition appears, or avoiding the decision record because the outcome was uncomfortable.

Trading frustration is one common pressure point because blocked expectations can make a trader want immediate repair. That response can blur the difference between a valid new decision and an emotional attempt to erase discomfort.

The Diagnostic Boundary: Emotion, Behavior, and Process

Trading psychology becomes useful when it separates emotional narrative from observable process behavior. A trader may feel fear and still follow the plan. Another trader may feel confident and still break risk rules. The emotion is the clue, but behavior is the evidence.

Boundary: A psychology label cannot prove price direction, confirm a setup, validate a trade, or explain every loss. It only helps evaluate whether emotional or cognitive pressure changed the decision process.

The cleanest comparison uses three records: the plan before the decision, the behavior during the decision, and the reason written afterward. If those records disagree, psychology may belong in the process check. If they remain aligned, an unfavorable outcome should not be converted into a psychological failure.

Emotion, Behavior, Risk, and Process Response

The same emotion can lead to different behavior. A structured record keeps the focus on what changed in execution, not on whether the emotion felt pleasant or uncomfortable.

| Pressure | Observable behavior | Risk created | Safer process response |

|---|---|---|---|

| Fear after a loss | Skipping valid criteria or exiting before the planned condition appears | The trader may confuse discomfort with new evidence | Compare the decision with the original plan before judging the outcome |

| Greed after a favorable move | Adding exposure without the same criteria used for the original decision | Risk can expand after confidence rises | Require the same decision standard before increasing commitment |

| FOMO after a missed move | Entering late because waiting feels worse than uncertainty | The decision may be based on urgency rather than structure | Separate missed opportunity from current eligibility |

| Frustration after repeated invalidation | Taking a new decision mainly to recover control | The decision record becomes reactive instead of evidence-based | Pause and identify whether the new decision has independent criteria |

| Overconfidence after several good outcomes | Reducing preparation or ignoring contrary evidence | Recent outcomes may be mistaken for process quality | Check whether the same standard would have been followed without the streak |

Clean, Weak, and Invalid Psychology Readings

A useful psychology check needs a boundary between clear evidence, weak evidence, and misleading blame. Without that boundary, every uncomfortable trade can be turned into a psychology story.

| Reading type | What it means | Review standard |

|---|---|---|

| Clean psychology reading | Emotion or bias is connected to a specific observable behavior that changed the plan. | The record identifies the trigger, the behavior change, and the process rule that was bypassed. |

| Weak psychology reading | The trader felt emotion, but the decision stayed consistent with the predefined process. | The emotion can be recorded, but it should not be treated as proof of poor execution. |

| Invalid psychology reading | The outcome was bad, but the decision followed the plan. | Calling the result a psychology failure would distort the record and punish process consistency. |

Common misunderstanding: The purpose of trading psychology is not to remove emotion. The stronger task is to notice when emotion changes behavior before, during, or after the decision.

Common Trading Psychology Mistakes

Most trading psychology mistakes are not visible as emotions alone. They show up when pressure changes the decision standard.

| Mistake | Behavioral clue | Safer interpretation |

|---|---|---|

| Revenge trading | A new decision appears mainly after a loss or frustrating sequence | The trade idea needs independent criteria, not emotional repair logic |

| Overtrading | Activity increases even when eligible conditions have not improved | The issue may be urgency, boredom, or pressure to act |

| Holding losers from loss aversion | The trader avoids accepting a defined invalidation condition | The record should separate plan-based patience from refusal to recognize loss |

| Exiting early from fear | The position is closed before the planned review condition appears | The decision may reflect discomfort rather than new market information |

| Plan drift after frustration | Rules become flexible only after several adverse outcomes | The process needs review before the next decision is treated as normal |

Trading Psychology and Cognitive Biases

Cognitive biases are one part of trading psychology. They describe recurring mental shortcuts that may influence how a trader interprets evidence, remembers outcomes, and reacts to risk.

Loss aversion is especially relevant because a trader may treat realized loss as more painful than the risk originally allowed. Confirmation bias may make supportive evidence feel heavier than conflicting evidence. Recency bias may make the latest outcome feel more predictive than it is. Overconfidence may reduce preparation after a favorable run.

Bias language should stay specific. Calling every mistake a bias can weaken the decision record because it hides the actual behavior that changed. A stronger process names the bias only after the behavior is visible.

How to Review Trading Psychology Without Turning It Into a Signal

Psychology review should evaluate decision quality, not forecast the next market move. The most useful record is often simple: what the plan required, what happened, what the trader did, and whether the action matched the original criteria.

Trading discipline covers the consistency side of that process. Psychology review explains the pressure that can interfere with consistency; discipline describes whether the rules were followed when the pressure appeared.

Patience in trading belongs in the same process check because waiting is often where pressure becomes visible. A trader may know the criteria but still act early because uncertainty feels harder than action.

Example of a Basic Trading Psychology Reading: A trader has a written condition for taking a setup. After a prior loss, the next occurrence meets the written condition, but the trader hesitates and leaves the decision unexecuted. The psychology reading is stronger if the record shows that fear from the previous loss changed the planned behavior. The reading is weaker if the setup only looked similar but did not meet the original criteria. The skipped trade’s later outcome does not decide the review; the comparison between the written condition and the actual action does.

Trading Psychology vs Related Concepts

Trading psychology is the broad decision-pressure layer. Related concepts are narrower and should not be collapsed into the same label.

| Concept | Primary role | Boundary |

|---|---|---|

| Trading psychology | Explains how emotional and cognitive pressure can affect decisions | Does not predict price or validate a trade |

| Trading discipline | Focuses on process adherence and consistency | Does not explain every emotional trigger behind rule-breaking |

| Patience in trading | Focuses on waiting behavior and timing restraint | Does not cover the full range of emotional and cognitive bias |

| Trading frustration | Focuses on emotional reaction under blocked or adverse conditions | Does not include every psychological pressure state |

| Loss aversion | Focuses on a specific bias around avoiding realized losses | Does not explain every form of poor execution |

| Psychological mistakes | Groups recurring behavior errors | Does not replace the core definition of the pressure layer |

FAQ

What is trading psychology?

Trading psychology is the way emotions, biases, pressure, and expectations influence trading decisions and execution behavior. It helps review decision quality, not predict price direction.

Why does trading psychology matter?

Trading psychology matters because pressure can change how a trader follows a plan, handles risk, waits for criteria, and reviews outcomes. The useful evidence is observable behavior, not emotion by itself.

Is emotion always a trading mistake?

No. Emotion becomes important when it changes behavior. A trader can feel fear or greed and still follow a defined process. The review should focus on whether the decision standard changed.

Can trading psychology confirm a trade?

No. Trading psychology cannot confirm a setup, validate a trade, or prove price direction. It can only help evaluate whether the decision process stayed consistent under pressure.