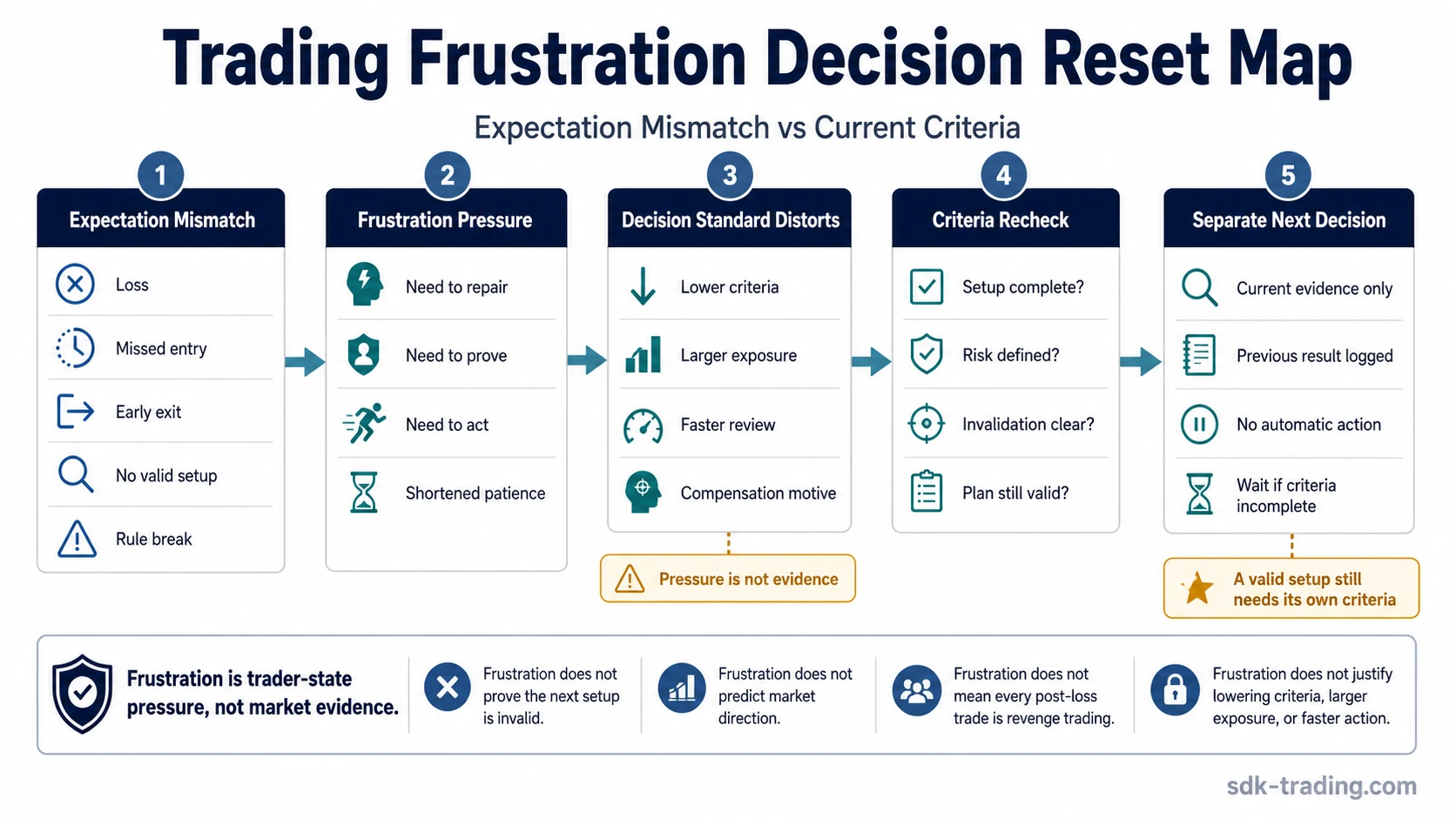

Trading frustration appears when expectation, execution, or market response diverges from what the trader expected and that mismatch begins to pressure the next decision. The frustration itself is not market evidence. The risk is that the trader starts treating a blocked expectation as a reason to force action, lower standards, increase exposure, or shorten review.

Frustration in trading can follow a loss, a missed entry, an early exit, a stop-out before the expected move, or a period where the market gives no clean setup. The pressure usually comes from the gap between what the trader wanted to happen and what actually happened. That gap can be useful only if it is labeled correctly: a trader-state signal, not a signal from price.

Trading frustration is a pressure state that can appear after expectation mismatch. It does not prove that the next setup is good or bad. It only shows that the trader may be carrying unresolved pressure into the next decision.

The Common Mistake: Treating Frustration as Evidence

The main mistake is using frustration to justify a different decision standard. A trader may feel that the next trade needs to recover a loss, prove the original idea was right, or compensate for a missed move. Once that happens, the next decision is no longer being judged only by the plan, setup, risk, and criteria.

The correction is not to suppress the emotion or pretend it is irrelevant. The correction is to classify it accurately. Frustration can be noted as trader-state pressure, then separated from current market evidence before any new decision is evaluated.

| Frustrated interpretation | Process correction |

|---|---|

| The last trade failed, so the next one must make it back. | The next decision needs its own criteria, risk definition, and evidence. |

| The missed move proves the trader must act faster. | Missed-move pressure belongs closer to FOMO trading when urgency starts replacing setup quality. |

| The market is unclear, so the rules should be loosened. | Unclear conditions are a reason to recheck criteria, not to lower them. |

| The trader was right but the timing was unlucky. | Separate idea quality, execution quality, and outcome quality before changing behavior. |

Common Trading Frustration Triggers

Trading frustration usually starts with blocked progress. The trader expected clarity, movement, validation, or recovery, but the market produced delay, rejection, loss, or ambiguity instead.

| Trigger | Common misread | Decision risk | Safer process interpretation |

|---|---|---|---|

| Losing streak | The next trade needs to recover the damage. | Increasing size or taking weaker setups. | The streak is reviewed separately from the next setup. |

| Missed entry | The trader must chase before the move is gone. | Entering without planned criteria. | The missed trade is logged as a missed decision, not converted into urgency. |

| Stopped out before expected move | The original idea was right, so re-entry is automatically justified. | Re-entering from irritation rather than fresh evidence. | The new decision needs to be checked against the planned criteria before it is treated as separate from the prior frustration. |

| Rule break or outcome that feels unfair | The market or the trader needs to be corrected immediately. | Changing rules after the result or forcing a compensating decision. | The rule break and the outcome are reviewed separately before the next setup is judged. |

| Exiting early before continuation | The trader must make up for leaving too soon. | Overcorrecting on the next trade. | The exit is reviewed as execution behavior before new exposure is considered. |

| No valid setup | The market is wasting time. | Forcing trades in unclear conditions. | No setup is a condition to observe, not a defect that must be solved by action. |

| Repeated break-even or near-miss outcomes | The trader is close and should push harder. | Moving rules, timing, or exposure to force a result. | Near misses require review, not compensation. |

How Frustration Distorts the Next Decision

Frustration becomes a decision problem when it changes the process before the trader notices the change. The setup may look similar on the surface, but the standard used to judge it becomes weaker, faster, or more personal.

- Impulse entries: The trader acts because waiting feels intolerable, not because planned conditions are complete.

- Overtrading pressure: Multiple weak attempts replace one defined decision.

- Revenge trading pressure: The next trade begins to carry the job of repairing the previous outcome.

- Changing criteria: The trader accepts evidence that would normally be considered incomplete.

- Increasing size: Exposure becomes a compensation tool instead of a risk decision.

- Shortened review: The trader skips the pause that normally separates idea, setup, risk, and execution.

Frustration is not proof that the next setup is invalid. A valid setup can appear after a frustrating outcome. The problem is not the sequence of events. The problem is whether frustration is now deciding the standard of evidence.

Expectation Mismatch and Perfectionism

Frustration often grows when the trader needs the market to provide progress, clarity, validation, or immediate recovery. The stronger that need becomes, the harder it is to accept ordinary market ambiguity.

Perfectionism can add pressure because every missed entry, early exit, or stop-out feels like a personal failure rather than a decision sample. That can blur the difference between a poor process, a normal losing outcome, and a reasonable decision that simply did not work.

A cleaner review separates three questions: Was the plan clear? Was the execution aligned with the plan? Was the outcome simply unfavorable despite acceptable process? Mixing those questions turns every frustrating result into a reason to change behavior.

A Short Example of Frustration in Trading

A trader waits for a planned setup, exits early after a small reaction, and then watches the market continue without them. The frustration is not market evidence. It is a pressure signal created by the mismatch between the expected participation and the actual result. If the trader immediately enters a weaker setup to repair the feeling of being left behind, the new decision is being shaped by frustration rather than by the original criteria.

The narrower interpretation is: the early exit deserves review, but it does not automatically justify a new position. The next setup still needs to be evaluated on its own structure, timing, risk, and invalidation.

Observable Signs of Frustration Pressure

The clearest signs are usually visible in behavior, not in the market. Price does not reveal whether a trader is frustrated. The trader’s changes in process often do.

- Urgency to recover immediately after a loss or missed move.

- Review becomes shorter than normal.

- Criteria change after the outcome instead of before the trade.

- Position size increases to compensate for a prior result.

- The trader cannot wait for the planned setup.

- The last outcome is replayed repeatedly while the current setup receives less attention.

- The next trade is framed as compensation rather than a separate decision.

If the pressure is mostly fear about what could happen before the trade is even taken, the issue is closer to trading anxiety. Frustration is more often tied to blocked expectation, blocked progress, or perceived execution failure.

Frustration, Anger, Regret, and Exit Pressure

Frustration can sit close to anger and regret, but the states are not identical. Anger often adds blame: the market, the broker, the news, the system, or the trader’s own mistake becomes the target. Regret focuses on the decision that was not taken, the exit that happened too early, or the entry that was missed.

Both states can distort the next decision if they demand immediate repair. The trader may start looking for a trade that relieves the feeling rather than a setup that meets the plan.

Fear-side pressure is different. If the emotional reaction mainly pushes the trader to exit quickly, abandon exposure, or escape discomfort during a decline, the behavior may be closer to panic selling. Frustration can contribute to exit pressure, but it is not always an exit behavior.

How to Reset After Trading Frustration

A reset is useful only if it returns the decision to planned criteria. It should not become a motivational routine or a way to force confidence. The purpose is to separate the last mismatch from the next decision.

- Pause and label the trigger: Identify whether the pressure came from a loss, missed entry, early exit, unclear market, or rule break.

- Separate outcome quality from execution quality: A losing outcome is not automatically poor execution, and a profitable outcome is not automatically good execution.

- Journal the mismatch: Write what was expected, what happened, and which part created pressure.

- Recheck predefined criteria: Confirm whether the next idea meets the planned setup, timing, risk, and invalidation requirements.

- Return to the plan: If criteria are incomplete, the reset is to wait or review. If criteria are complete, the trade still stands or fails on the plan, not on the frustration.

A trade after a loss is not automatically revenge trading. The distinction is whether the new decision is based on current criteria or on the need to repair the previous outcome.

What Trading Frustration Does Not Mean

Trading frustration is a decision-process warning, not a market forecast. It does not mean the trader is wrong about direction, and it does not mean the next setup must fail. It only means the decision process needs enough separation from the previous mismatch.

- It is not proof that the current market is unfair or abnormal.

- It is not proof that the next trade is invalid.

- It is not always visible as overtrading.

- It is not the same as anxiety, which is more tied to anticipated uncertainty.

- It is not the same as FOMO, which is more tied to missed opportunity and urgency.

- It is not a trading signal, entry condition, exit condition, or sizing reason.

If the emotional reaction becomes severe, persistent, or affects behavior outside trading, a trading journal or reset routine may not be enough. In that case, support from a qualified professional can be more appropriate than another trading-process adjustment.

FAQ

Is every frustrated trade revenge trading?

No. A trade after frustration becomes revenge trading only when the main purpose shifts toward recovering, proving, or compensating for the previous result. A new trade can still be valid if it meets the planned criteria independently.

Is trading frustration always caused by losing money?

No. Frustration can appear after a missed entry, early exit, unclear market, break-even result, or failure to follow the plan. The common source is expectation mismatch, not only loss.

Can frustration appear after a winning trade?

Yes. A trader may feel frustrated after winning if the trade was exited too early, sized too small, or handled outside the plan. The result may be positive while the process still feels unresolved.

What is the difference between frustration and anxiety in trading?

Frustration usually follows blocked expectation or perceived execution failure. Anxiety is more often anticipatory and appears before or during uncertainty about what may happen next.