Panic selling in trading is not simply selling quickly during a decline. It is a stress-driven decision break where urgency changes evidence review, risk behavior, or invalidation discipline before the trading record supports that change.

The key diagnostic is the decision process. A fast exit can be rational when price action, risk limits, invalidation, or exposure rules already support it. Panic selling begins when the need for relief shortens the review and turns discomfort into the reason for action.

Definition: Panic selling is an urgency-driven exit or exposure reduction in which fear narrows the trader’s review before the evidence, risk plan, or invalidation condition justifies the change.

Key Points

- Panic selling is identified by process distortion, not by whether the market later rebounds or continues lower.

- A structured exit can happen quickly when pre-defined evidence or risk rules support the action.

- The common break is evidence narrowing: the trader stops reviewing context and starts acting to reduce emotional pressure.

- Market-wide selling pressure can amplify urgency, but the individual trading question remains whether the decision record changed.

What Panic Selling Means in Trading

In trading, panic selling describes a breakdown in exit discipline under stress. The trader may reduce exposure, close a position, or abandon a planned review because the immediate feeling of danger becomes stronger than the evidence being reviewed.

That does not make every defensive action a panic response. A position can be closed quickly when the market reaches a defined invalidation point, when risk limits are exceeded, or when new evidence changes the original decision. The difference is whether the action follows the decision record or replaces it.

Panic selling can also describe broader market behavior, where falling prices create fear, fear creates more selling, and that selling can deepen the decline. For an individual trader, the useful question is narrower: did crowd pressure or market stress change the review before the evidence changed?

How Panic Selling Changes the Decision Process

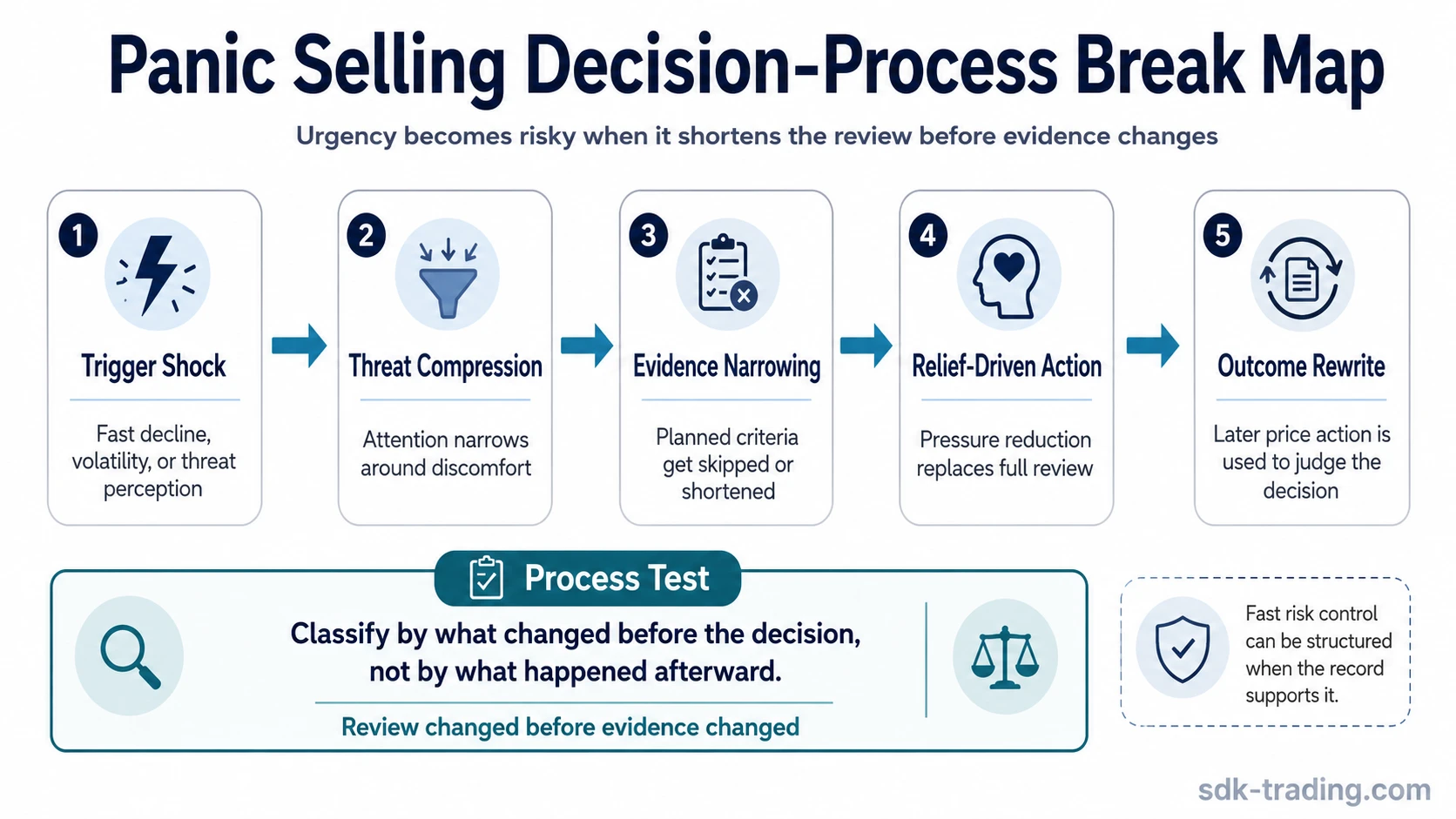

Panic selling usually develops through a compressed sequence. The market move may be fast, but the real damage happens when the review becomes shorter, narrower, and more relief-driven.

- Trigger shock: A fast decline, volatility spike, news reaction, or sharp unrealized loss creates immediate threat perception.

- Threat compression: Attention narrows around the discomfort of the position instead of the full trading context.

- Evidence narrowing: The trader stops checking the planned criteria and focuses only on the information that confirms danger.

- Relief-driven exit: The exit becomes a way to end emotional pressure rather than a decision supported by the full record.

- Post-outcome rationalization: The trader later judges the decision mainly by what happened afterward, instead of reviewing whether the process was followed.

Process note: Panic selling collapses the separation between market fear and trade expression. A bearish view, a risk-reduction decision, and an actual exit are separate decisions until the record supports connecting them.

Panic Selling vs a Structured Risk Exit

The same external action can have different meanings. Two traders may both exit during volatility, but one may be following a defined risk rule while the other is reacting to pressure before the review is complete.

| Decision area | Panic selling | Structured risk exit |

|---|---|---|

| Evidence review | Review is shortened by urgency or fear. | Review follows the planned evidence, context, and invalidation criteria. |

| Reason for action | The main driver is relief from pressure. | The main driver is a defined risk, evidence, or exposure rule. |

| Speed of decision | Speed replaces the process. | Speed can be acceptable because the process was defined before stress increased. |

| Role of outcome | Later price action is used to justify or condemn the decision. | Later review asks whether the decision followed the record, regardless of outcome. |

| Discipline test | Urgency changed behavior before evidence changed. | Behavior changed because evidence, invalidation, or risk limits changed. |

Boundary: A fast liquidation is not automatically panic selling. It becomes panic selling when urgency overrides the review that was supposed to decide whether the trade was still valid.

What Can Trigger Panic Selling

Panic selling can start when a trader interprets market pressure as an immediate threat and stops separating discomfort from evidence. The trigger may be external, but the classification depends on what happens inside the decision process.

| Trigger | How it can distort the decision | Safer interpretation |

|---|---|---|

| Sudden volatility | The move feels dangerous before the planned criteria are reviewed. | Volatility raises the need for review; it does not automatically decide the trade. |

| Large decline | Loss size becomes the only evidence considered. | The decline matters most when it changes structure, invalidation, or risk limits. |

| Perceived threat | The trader reacts to what could happen next instead of what is confirmed. | Scenario risk should be separated from confirmed evidence. |

| Crowd behavior | Visible selling pressure makes urgency feel like confirmation. | Crowd pressure can matter, but it still needs context and acceptance behavior. |

| Margin pressure | Forced exposure reduction can remove time for normal review. | Forced selling is a risk-control issue, not proof that every exit was discretionary panic. |

| Stop-loss cascades | Automatic orders can accelerate the move and intensify fear. | Cascades can increase pressure, but they do not replace the trader’s own decision record. |

| Algorithmic or automatic selling | Market-wide acceleration can make the decline feel self-confirming. | Market mechanics can amplify urgency without proving that a discretionary exit was correct or incorrect. |

The Panic Selling Feedback Loop

Panic selling can feed on itself when a decline creates fear, fear creates more selling, and additional selling pushes price lower. That loop can happen across a market, inside a group of leveraged participants, or inside one trader’s decision process.

At the market level, the loop may involve crowd behavior, forced liquidation, stop-loss cascades, and automatic selling. At the trader level, the loop is more personal: the price decline creates urgency, urgency narrows the review, and the narrowed review makes the exit feel necessary before the full record is checked.

Illustrative scenario: A trader sees a fast decline and skips the planned review of structure, invalidation, and position risk. The position is closed mainly to remove pressure. If price later rebounds, the trader calls the exit panic; if price keeps falling, the trader calls it discipline. Both reviews are incomplete because the real question is whether the decision process was followed at the time.

Diagnostic Checklist

A useful review does not start with “was the exit right?” It starts with what changed before the exit happened.

- Evidence change: Did the evidence change, or did only the urgency change?

- Review length: Was the planned review shortened or skipped?

- Risk behavior: Did position behavior change before invalidation, exposure limits, or evidence supported that change?

- Relief driver: Was the decision made mainly to reduce emotional pressure?

- Outcome rewrite: Is later price action being used to rewrite the quality of the decision?

Review principle: Classify by the process, not the outcome. A poor outcome after a structured exit does not automatically prove panic, and a favorable outcome after a rushed exit does not automatically prove discipline.

Common Misread: Judging Panic Selling by Outcome

The most common mistake is using the later chart to decide whether the trader panicked. A rebound after the exit can make the decision feel emotional, but it does not prove the process was broken. A continued decline can make the exit look correct, but it does not prove the process was disciplined.

Outcome review matters, but it should not replace process review. The cleaner question is whether the trader had a defined basis for changing exposure before stress increased. If the answer is yes, the exit may have been structured risk control. If the answer is no, the exit may have been driven by urgency even if the later price action made it look reasonable.

Limitation: Panic selling is not a moral label and not a forecast label. It does not say what price should do next. It describes a decision-process break where fear changes the review before the decision record supports that change.

Related Trading Psychology Concepts

Panic selling belongs to a wider group of emotional-pressure distortions, but it has a specific direction. It pushes the trader toward exiting or reducing exposure under stress.

FOMO trading is different because urgency pulls the trader toward chasing opportunity, usually through entry pressure rather than exit pressure. Revenge trading is different because frustration after a loss or missed move pushes the trader toward reactive re-engagement.

The shared issue is not emotion by itself. Fear, urgency, frustration, and excitement become trading problems when they change evidence review, risk behavior, invalidation discipline, or post-outcome review before the record supports that change.

FAQ

Is every fast exit panic selling?

No. A fast exit can be structured when it follows pre-defined evidence, invalidation, exposure, or risk rules. It becomes panic selling when urgency replaces the review.

Can panic selling ever reduce risk?

It can reduce exposure, but that does not automatically make the decision disciplined. The review should ask whether the risk reduction was supported by the trading record or driven mainly by relief.

How is panic selling different from FOMO trading?

Panic selling pushes a trader toward exiting under threat pressure. FOMO trading pushes a trader toward entering or chasing because opportunity feels urgent.

How is panic selling different from revenge trading?

Panic selling is usually an exit-pressure response to perceived danger. Revenge trading is reactive re-engagement after frustration, loss, or the desire to recover control.