Trading anxiety is emotional pressure around a trade that changes the decision process before the evidence changes. It is not simply feeling nervous, reducing risk, or avoiding a low-quality setup. The problem begins when pressure shortens review, changes execution, distorts risk behavior, or weakens post-trade evaluation.

- Trading anxiety becomes relevant when pressure changes the trading process, not merely when the trader feels uncomfortable.

- The clearest signs are process changes: hesitation, rushed exits, skipped review, forced confirmation seeking, or risk changes that were not part of the plan.

- A defensive decision is not automatically anxiety-driven if the evidence, risk condition, or invalidation point actually changed.

- The safer boundary is to compare the emotional pressure with the decision record before judging the action.

What Is Trading Anxiety?

Trading anxiety is a trading-psychology condition where uncertainty, loss memory, risk discomfort, or outcome pressure begins to affect how a trader reviews evidence, executes a plan, manages risk, or evaluates the result.

The boundary is process-based. A person can feel tension and still follow the plan. Risk can also be reduced for a valid reason if setup quality changed, volatility broke a predefined condition, or the original risk was too large. Anxiety becomes the stronger label when the decision changes before the trading evidence supports that change.

That makes trading anxiety different from ordinary nerves. Nerves describe the feeling. Trading anxiety describes the effect of that feeling on review, execution, risk behavior, or outcome evaluation.

What Trading Anxiety Is Not

| Mistaken label | Safer interpretation |

|---|---|

| Any nervous feeling before a trade | Nervousness alone is not enough. The question is whether the feeling changed evidence review, execution, risk behavior, or post-trade review. |

| Any decision to reduce exposure | Reducing risk can be valid if the plan, setup quality, or risk condition changed. It becomes anxiety-driven only when the change is not supported by the decision record. |

| Any skipped trade | A skipped trade may reflect discipline if the setup did not meet the plan. It may reflect anxiety if the setup met the plan but execution froze without new evidence. |

| Any losing trade | A loss does not prove anxiety. The process has to be checked separately from the outcome. |

| A need to become emotionless | The goal is not emotionless trading. The goal is to keep emotion from replacing review, evidence, and process discipline. |

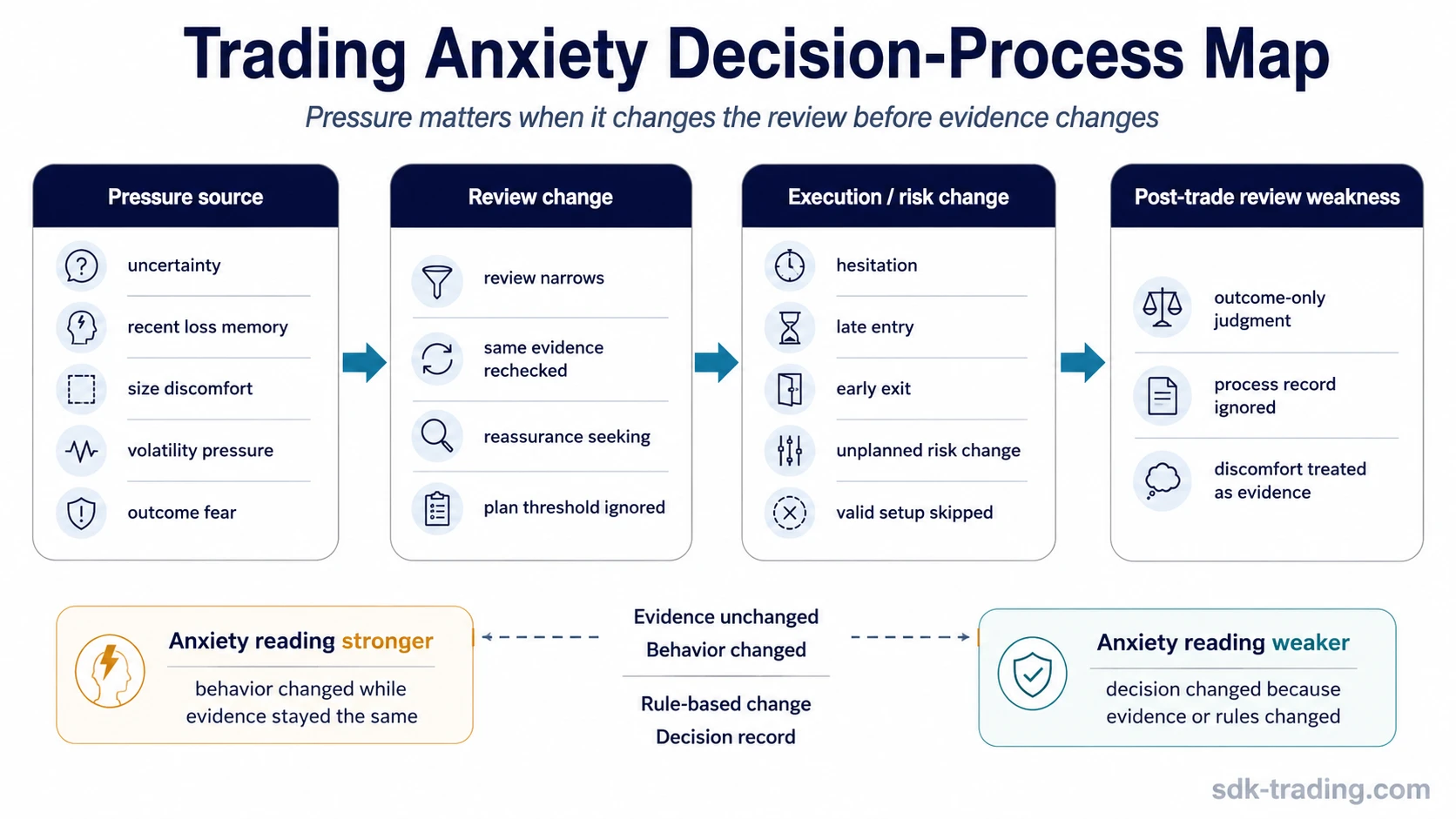

How Trading Anxiety Changes the Decision Process

Trading anxiety usually becomes visible through a sequence: pressure rises, review narrows, execution changes, and the trade is later judged through emotion or outcome instead of the original decision record.

- Pressure source: The trader feels uncertainty, loss memory, position-size discomfort, volatility pressure, or urgency to act.

- Review change: The trader checks less evidence, checks the same evidence repeatedly, or looks for reassurance instead of evaluating the plan.

- Execution change: The trader hesitates, enters late, exits early, cancels a valid setup, or changes risk without a rule-based reason.

- Review weakness: The trader judges the decision mainly by the result, not by whether the original process was followed.

The process change matters more than the emotion itself. A calm trader can still make a poor process decision, and an anxious trader can still follow a valid plan.

Common Triggers of Anxiety in Trading

Trading anxiety often starts when uncertainty feels exposed and the trader does not have enough process structure to separate valid caution from emotional pressure.

| Trigger | How it can affect the process | What to check before labeling it anxiety |

|---|---|---|

| Recent loss memory | The trader avoids a setup that still meets the plan because the previous loss feels too close. | Did the current setup actually weaken, or is the old outcome controlling the new decision? |

| Uncertainty before entry | The trader keeps searching for extra confirmation after the planned evidence is already present. | Is more information required by the plan, or is the review turning into reassurance seeking? |

| Position-size discomfort | The trader changes exposure mid-decision because the size feels uncomfortable. | Was the size outside the rule set, or did discomfort appear after the plan was already accepted? |

| Volatility | The trader exits before invalidation because the movement feels too fast. | Did volatility break a predefined condition, or did speed alone override the plan? |

| Outcome pressure | The trader focuses on being right instead of reviewing whether the evidence still supports the decision. | Is the trade being managed by evidence, or by fear of the next result? |

Observable Signs of Trading Anxiety

The strongest signs are not private feelings. They are visible changes in how the decision is made, managed, or reviewed.

- Execution hesitation: A planned trade is delayed even though the required conditions are still present.

- Premature exit: A position is closed before the evidence or invalidation condition changes.

- Skipped review: The trader acts quickly to reduce discomfort instead of checking the planned evidence.

- Forced confirmation seeking: The trader keeps looking for one more reason after the decision threshold has already been reached.

- Unplanned risk change: Exposure is reduced, increased, or moved for emotional relief rather than rule-based adjustment.

- Outcome-only review: The decision is judged mainly by profit or loss, not by whether the process was followed.

None of these signs proves anxiety by itself. The stronger test is whether behavior changed while the evidence stayed the same.

Diagnostic Boundary: What Confirms or Invalidates the Anxiety Reading

Pressure alone does not confirm trading anxiety. Trading anxiety is more likely when the evidence is unchanged but review, execution, risk behavior, or post-trade evaluation changes. The reading weakens when the decision change follows a predefined rule, a changed evidence state, or a corrected risk violation.

| Situation | Possible process distortion | Confirms anxiety reading | Invalidates anxiety reading |

|---|---|---|---|

| Loss memory | A valid setup is avoided because the previous loss feels too fresh. | The current evidence still meets the plan, but execution freezes. | The current setup quality actually weakened or no longer meets the plan. |

| Volatility pressure | The trader exits before the planned invalidation point. | The exit happens because the move feels uncomfortable, not because the evidence changed. | Volatility breaks a predefined condition that was part of the plan. |

| Position-size discomfort | Risk is changed after the trade is already underway. | The size change is made for emotional relief rather than a rule-based reason. | The original size violated the rule set and the correction restores the plan. |

| Uncertainty before entry | The trader keeps demanding extra confirmation. | The planned decision threshold was already reached, but the review keeps restarting. | The plan required more evidence and the extra review is part of the process. |

| Outcome pressure | The trader changes the decision to avoid being wrong. | The decision is managed by fear of outcome rather than evidence review. | The risk condition changed and the adjustment follows the original rules. |

Practical Scenario

A trader has a plan that requires a defined setup, a specific confirmation condition, and a predefined invalidation point. The setup appears and the evidence still matches the plan, but the trader remembers a recent loss and starts checking the same chart repeatedly. Nothing in the plan has changed, yet execution is delayed until the trade no longer matches the original condition.

The useful reading is not “the trader felt nervous.” The useful reading is that emotional pressure changed the review and execution sequence before the evidence changed. If the setup had actually weakened before entry, skipping it could have been a valid defensive decision instead.

How Trading Anxiety Differs From Nearby Trading Psychology Problems

Trading anxiety overlaps with other emotional trading problems, but the label should be chosen by the process that changed.

| Concept | Main process change | Boundary from trading anxiety |

|---|---|---|

| Trading anxiety | Pressure narrows review, delays execution, changes risk behavior, or weakens evaluation. | The core issue is uncertainty or discomfort changing the decision process before evidence changes. |

| Revenge trading | The trader tries to recover emotionally from a loss by forcing new action. | The core issue is retaliatory behavior after a loss, not hesitation or uncertainty before a decision. |

| FOMO trading | The trader chases a missed or fast-moving opportunity. | The core issue is urgency to participate, not discomfort with risk or uncertainty itself. |

| Panic selling | The trader exits quickly under fear or urgency. | The core issue is rapid liquidation behavior, not every anxious review or hesitant entry. |

| Fear and greed in trading | Emotional pressure swings between avoidance and over-pursuit. | The concept is broader; trading anxiety is one narrower way pressure can affect decisions. |

| Trading discipline | The trader’s consistency with rules, review, and execution is tested. | Discipline is the broader process standard; anxiety is one possible reason the process breaks. |

How to Deal With Trading Anxiety Without Turning It Into a Trading Signal

Trading anxiety should not be handled as a signal that a trade must be entered, avoided, reduced, or closed. The safer response is to separate the feeling from the evidence record.

- Name the pressure: Identify whether the pressure comes from uncertainty, loss memory, size discomfort, volatility, or outcome fear.

- Compare against the plan: Check whether the required evidence is still present, missing, or changed.

- Separate correction from avoidance: A rule-based reduction can be valid; an emotion-based change needs review.

- Protect invalidation discipline: Moving or ignoring invalidation because of discomfort weakens the decision record.

- Review process before result: A profitable outcome does not prove the process was sound, and a losing outcome does not prove anxiety caused the decision.

The purpose of this process is not to remove all emotion. The purpose is to keep emotion from replacing evidence, structure, and review discipline.

Common Mistakes When Identifying Trading Anxiety

| Mistake | Why it creates a weak reading | Better diagnostic question |

|---|---|---|

| Calling every nervous feeling trading anxiety | Feelings alone do not show whether the trading process changed. | Did the feeling alter review, execution, risk behavior, or evaluation? |

| Assuming anxiety always causes losses | Outcome and process are different. A poor process can still produce a favorable result. | Was the decision record followed, regardless of the outcome? |

| Treating risk reduction as proof of anxiety | Risk reduction may be valid if evidence or rule conditions changed. | Was the adjustment supported by the plan or made only to reduce discomfort? |

| Trying to become emotionless | Emotionless trading is not the practical standard. Process stability is the practical standard. | Can the trader feel pressure and still follow the review sequence? |

| Using a checklist as a guarantee | A checklist can improve review structure, but it does not guarantee better outcomes. | Does the checklist protect the process without pretending to control the result? |

When Anxiety Is Not the Right Explanation

Anxiety is not the strongest explanation when the decision changed because the market evidence changed, the plan was incomplete, the setup no longer met its conditions, or the original risk was not acceptable under the trader’s own rules.

A valid defensive adjustment is different from anxiety-driven distortion. If the decision can be traced to a predefined condition, a changed evidence state, or a corrected rule violation, the anxiety label becomes weaker.

The cleanest review question is: did the decision change because the evidence changed, or because emotional pressure made the same evidence feel harder to act on?

Trading Anxiety FAQ

Is trading anxiety the same as fear?

No. Fear is a broad emotional response. Trading anxiety is more specific: it describes pressure around a trade that changes review, execution, risk behavior, or post-trade evaluation before the evidence changes.

Is reducing risk always a sign of trading anxiety?

No. Reducing risk can be valid if the setup quality changed, the original size violated the plan, or a predefined risk condition was triggered. It becomes more likely to reflect anxiety when the reduction is made only to relieve discomfort while the evidence remains unchanged.

How do you know anxiety affected a trading decision?

The strongest sign is a process change without an evidence change. Examples include delayed execution, premature exit, repeated reassurance seeking, skipped review, or unplanned risk changes that were not supported by the original decision record.

Can trading anxiety happen before entering a trade?

Yes. It can appear before entry when the planned evidence is present but the trader freezes, keeps restarting the review, or avoids the setup because the risk feels uncomfortable rather than because the setup failed the plan.