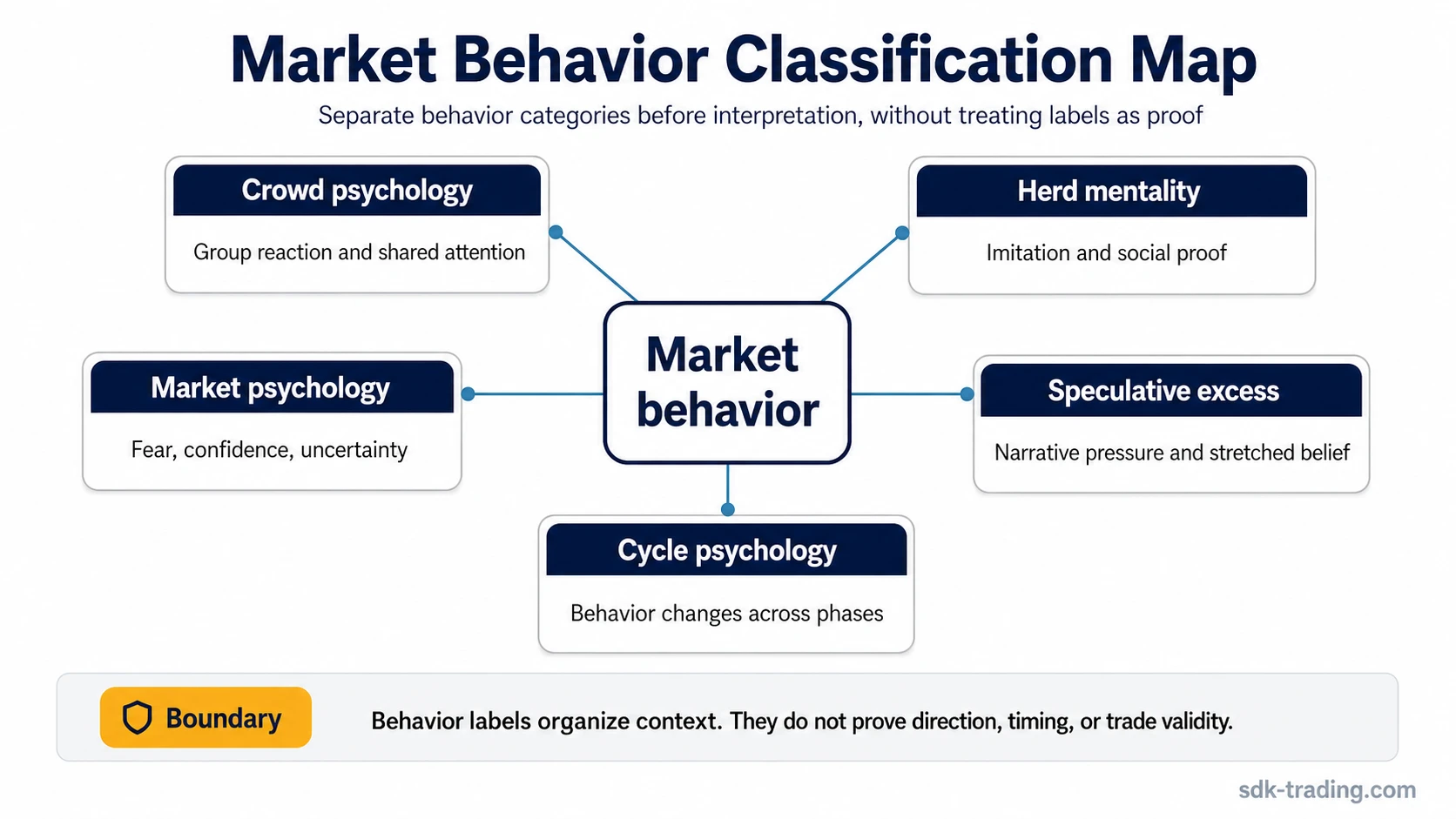

Market behavior in trading is a trading-psychology classification area. It separates crowd psychology, herd mentality, broader market psychology, speculative bubbles, sentiment extremes, and cycle psychology without treating any of them as a trade signal, forecast, setup, or replacement for a trading plan.

Definition: Market behavior describes how groups of market participants appear to respond to price movement, sentiment, perceived opportunity, fear, uncertainty, and narrative pressure. In trading psychology, the term organizes behavior-driven market conditions without proving that any trade is valid.

Key Points

- Market behavior is a classification layer inside trading psychology, not a standalone execution method.

- Crowd psychology, herd mentality, market psychology, bubbles, and cycle psychology describe related but different behavior patterns.

- Crowd participation does not automatically validate a trade, and contrarian behavior is not automatically smarter than following the crowd.

- Sentiment extremes, overbought or oversold labels, and accumulation or distribution language need context before they can be interpreted safely.

- The strongest use of market behavior is classification: identify the behavior category first, then study the specific behavior pattern in more detail.

What Market Behavior Means in Trading Psychology

Market behavior refers to the visible and interpreted actions of participants as prices move through uncertainty. It can include crowd agreement, emotional acceleration, narrative reinforcement, speculative excess, hesitation near extremes, or cycle-stage behavior. These are interpretation categories, not execution permissions.

In trading psychology, market behavior is useful because it narrows the question. Is the issue crowd pressure? Is it herd participation? Is it broader sentiment? Is it bubble-like excess? Is it cycle-phase behavior? Those questions should be separated before behavior is connected to planning, confirmation, or risk.

Classification filter: Market behavior helps identify what kind of participant behavior is being discussed. The label should not be used to decide whether price should rise, fall, reverse, continue, or justify a position.

Main Market Behavior Categories

The main concepts separate by the type of behavior question involved.

| Behavior category | Behavior question | Best next concept | Boundary |

|---|---|---|---|

| Crowd psychology | How group emotion, shared attention, and crowd reaction can influence interpretation. | Crowd psychology in trading | Crowd agreement does not prove that a trade is correct or that a move must continue. |

| Herd mentality | Why participants may follow others even when their own evidence is incomplete. | Herd mentality in investing | Following a crowd is not automatically wrong, but it becomes risky when evidence is replaced by imitation. |

| Market psychology | How fear, confidence, uncertainty, and expectation shape the background environment. | Market psychology | Market psychology is context, not a complete trading plan or forecast engine. |

| Speculative excess and bubbles | When participation, narrative, and price extension may become detached from sober evaluation. | Stock market bubble | Bubble language is often easier to apply after the fact and should not be used as a mechanical reversal call. |

| Cycle psychology | How behavior may change across expansion, enthusiasm, stress, exhaustion, and reset phases. | Market cycle psychology | Cycle labels can help organize context, but they do not prove timing or direction by themselves. |

Crowd Psychology vs Herd Mentality vs Market Psychology

These terms overlap, but they do not describe the same problem. Crowd psychology focuses on the behavior of groups under shared attention. Herd mentality focuses on imitation and social proof. Market psychology is broader: it includes fear, confidence, uncertainty, expectations, and the emotional background around price movement.

| Term | Primary focus | Useful interpretation | Common mistake |

|---|---|---|---|

| Crowd psychology | Group reaction | Shows how attention and emotion can cluster around a move or narrative. | Treating popular participation as confirmation that the move is safe. |

| Herd mentality | Imitation | Shows how participants may copy others instead of checking their own criteria. | Assuming the crowd is always wrong or always right. |

| Market psychology | Emotional environment | Shows how fear, confidence, expectation, and uncertainty shape interpretation. | Using broad mood language as if it were an execution rule. |

Each concept creates a different interpretation problem. Crowd psychology asks what the group is reacting to. Herd mentality asks whether participants are copying each other. Market psychology asks what emotional environment surrounds the decision process.

When Market Behavior Becomes Speculative Excess

Market behavior becomes more fragile when participation shifts from interpretation to assumption. A trader may see more attention, stronger narratives, faster price movement, or more confident commentary. None of those features proves that a market is in a bubble, but together they can raise the question of whether behavior has become less evidence-based.

Speculative excess often involves a stronger gap between what participants believe and what the available evidence can support. That gap can appear through narrative pressure, fear of missing out, late participation, or the belief that recent movement validates itself. The safer interpretation is conditional: behavior may be stretched, but stretched behavior is not a timing signal by itself.

Boundary: A market can stay extended longer than a behavioral label suggests. Bubble, euphoria, panic, overbought, oversold, accumulation, and distribution are classification terms. They need structure, evidence, and review before they can support any stronger conclusion.

What Market Behavior Does Not Prove

Market behavior can help organize interpretation, but it should not be treated as proof. It does not prove that a trade is valid, that a crowd is wrong, that a reversal is near, that a trend must continue, or that sentiment has reached a usable extreme.

| Misuse | Safer interpretation |

|---|---|

| Crowd participation proves the move is valid. | Crowd participation shows attention and agreement, but the decision still needs criteria, structure, and risk boundaries. |

| Contrarian behavior is automatically superior. | Going against the crowd is only meaningful when there is evidence that the crowd’s interpretation is weak or crowded in an unsafe way. |

| Sentiment extremes create automatic reversal signals. | Extremes are often easier to label after the fact and can persist while price continues moving. |

| Trend participation means the plan can be ignored. | A strong trend may increase attention, but it does not replace predefined criteria or review discipline. |

| Behavior labels replace a trading plan. | Behavior labels organize context. They do not define entries, exits, sizing, invalidation, or execution rules. |

A Short Classification Scenario

Example scenario: A market has been rising for several sessions, commentary becomes more confident, and more participants begin describing the move as obvious. The first question is not whether to follow or fade the move. The first question is classification: is this crowd psychology, herd mentality, broader market psychology, speculative excess, or a cycle-stage behavior pattern?

If participants are reacting together to the same narrative, the better concept is crowd psychology. If they are copying others without independent criteria, the better concept is herd mentality. If the issue is the broader emotional background, the better concept is market psychology. If the move is becoming narrative-led and detached from sober evaluation, the better concept may be speculative excess or bubble behavior.

This is a generic example, not a historical case or trade instruction. It shows why behavior labels need classification before they are used for interpretation.

Where to Go Next by Concept

Market behavior should organize related behavior concepts without replacing the detailed explanation of each one.

- Use crowd psychology when the main issue is group reaction, shared attention, emotional clustering, or crowd response to price movement.

- Use herd mentality when the main issue is imitation, social proof, or following others without enough independent criteria.

- Use market psychology when the main issue is the broader emotional environment around fear, confidence, uncertainty, or expectation.

- Use stock market bubble when the main issue is speculative excess, narrative pressure, and a possible gap between belief and evidence.

- Use market cycle psychology when the main issue is how behavior changes across different market-cycle phases.

Classification boundary: Market behavior organizes the behavior family. The detailed explanation should stay with the specific concept being studied.