Herd mentality in investing is the tendency for investors to copy or align with visible crowd behavior instead of maintaining independent analysis, defined criteria, and risk boundaries. Not every group move is herd mentality: many investors can react similarly to the same public information without copying one another. A herding reading becomes stronger when crowd visibility, social proof, or fear of missing out weakens the decision process that would normally check evidence, risk, and alternatives.

Definition: Herd mentality in investing means investor behavior shifts from independent judgment toward imitation of a visible group, popular trend, or perceived informed crowd. The key issue is not that many people act in the same direction; it is that the crowd begins to replace the investor’s own criteria.

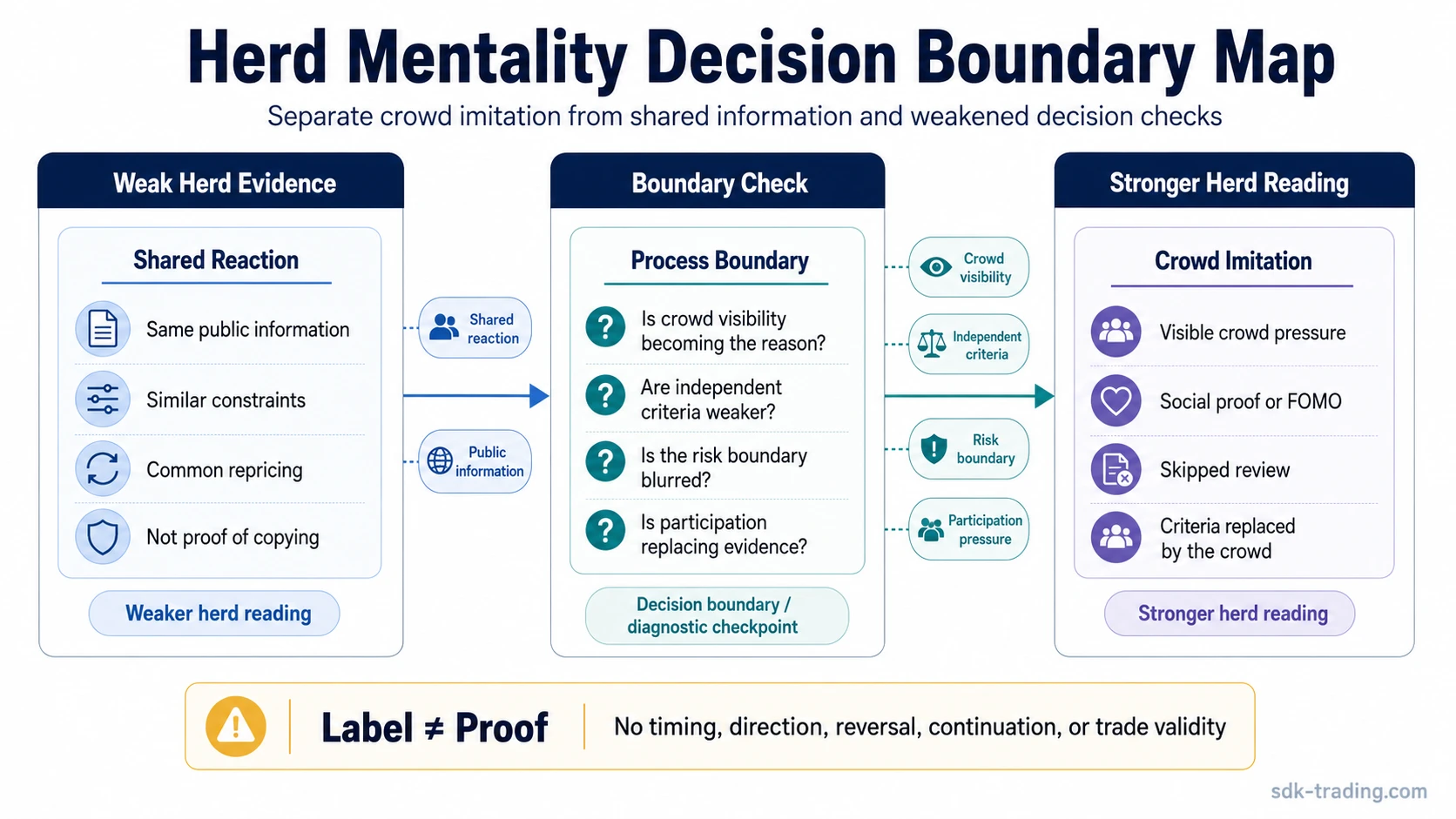

In market behavior, herd mentality can appear during crowded buying, panic selling, speculative attention cycles, and popular narratives. The label is most useful when it identifies a decision-process problem: the investor follows participation pressure before the evidence, risk boundary, or original thesis supports that action.

Key Points

- Herd mentality in investing is about imitation and weakened independent judgment, not simply a large number of investors moving in the same direction.

- A similar market reaction can come from shared public information, fundamentals, constraints, or liquidity conditions without proving true herding.

- FOMO, social proof, visible trend participation, and the belief that “others know something” can all strengthen herd behavior.

- The main risk is not only price movement; it is the loss of criteria, risk discipline, and evidence checks during crowd-driven participation.

- A crowd label does not validate a trade, prove continuation, prove reversal, or make contrarian action automatically better.

What Is Herd Mentality in Investing?

Herd mentality in investing describes a shift from independent evaluation toward crowd imitation. An investor may buy because a stock, sector, theme, or market is attracting visible attention, or sell because a wave of fear makes holding feel socially or emotionally harder.

The concept overlaps with behavioral finance because the investor is not only responding to price. The decision is influenced by the behavior of other participants: what they appear to be buying, selling, praising, abandoning, or treating as obvious.

The strongest sign is a weakening of the normal decision filter. Independent analysis becomes secondary. Risk boundaries become flexible. Evidence that would normally slow the decision is ignored because the crowd seems to be moving first.

Important distinction: Herd mentality is a narrower behavior than broad crowd psychology in trading. Crowd psychology can describe many group emotions and feedback loops. Herd mentality specifically focuses on copying or aligning with the crowd because the crowd itself becomes persuasive.

What Herd Mentality Is Not

A herd label is easy to overuse. Similar decisions across many investors do not automatically prove imitation. A market can move in one direction because participants are reacting to the same information, facing the same constraints, or repricing the same risk.

| Misread | Safer interpretation |

|---|---|

| Any popular trade is herd mentality | A popular trade may still be supported by independent evidence, valuation logic, technical structure, or a clear risk plan. |

| Any large group move proves copying | Many participants can respond to the same public information without relying on imitation. |

| A market bubble is the same thing as herding | A stock market bubble can include herd behavior, but speculative excess, valuation detachment, and feedback loops are broader conditions. |

| Contrarian action is automatically smarter | Acting against the crowd without evidence can be another emotional reaction, not a better decision process. |

| A crowd label confirms a setup | Herd behavior may describe participation pressure, but it does not prove timing, direction, continuation, reversal, or trade validity. |

Boundary: Herd mentality becomes a useful diagnosis only when the crowd appears to replace independent criteria. Without that process change, the same market move may be a shared reaction rather than true herding.

Why Investors Follow the Herd

Herding often begins because the crowd feels like information. If many participants appear to be buying, the move can look safer, smarter, or more urgent than it really is. The investor may treat participation itself as confirmation.

- FOMO: A rising price or popular theme can create pressure to act before the move is “missed.”

- Social proof: Visible participation can make an idea feel more credible even before the investor has checked the evidence.

- Safety in numbers: Being wrong with a crowd can feel emotionally easier than being wrong alone.

- Perceived informed action: Investors may assume others know something, even when the visible crowd is reacting to the same incomplete information.

- Narrative compression: A complex market situation can get reduced to a simple crowd story that spreads faster than the underlying analysis.

- Skipped review: Criteria, invalidation, sizing, and downside scenarios may receive less attention once the crowd move feels urgent.

The problem is not that investors notice other participants. Market awareness is normal. The problem begins when crowd behavior becomes the reason for action before the investor has tested whether the decision still fits the evidence and the risk boundary.

How Herd Mentality Can Affect Market Behavior

Herd mentality can amplify market moves because participation itself can attract more participation. Rising prices can draw in buyers who fear missing the move. Falling prices can push investors to sell because others appear to be exiting. In both cases, the crowd can create pressure that moves faster than careful evaluation.

Possible effects include trend chasing, volatility amplification, buying after a move has already become crowded, panic selling during stress, and speculative excess during strong narratives. These are possible effects, not automatic outcomes.

A herd reading also does not mean the market must reverse. Crowded behavior can continue longer than expected, weaken suddenly, or become mixed with valid information. The useful question is not “Is the crowd wrong?” but “Has crowd pressure weakened the decision process?”

Limitation: Herd mentality can help explain participation behavior, but it cannot by itself determine direction, timing, continuation, reversal, or whether a position is justified.

When Herd Mentality Becomes a Stronger or Weaker Reading

A stronger herding reading requires more than a popular move. It requires signs that investors are copying visible behavior or allowing crowd pressure to override independent review.

| Boundary check | What it suggests | Why it matters | Stronger or weaker herd reading |

|---|---|---|---|

| Similar market move | Many participants are acting in the same direction. | Alignment begins the question, but it does not prove imitation. | Weak by itself |

| Visible crowd pressure | The trade, asset, sector, or narrative is attracting attention and participation. | Visibility can make the crowd feel like confirmation. | Stronger if visibility becomes the reason for action |

| Independent criteria weakened | The decision relies less on analysis, structure, valuation, or predefined conditions. | Herding is most useful as a process diagnosis when criteria are displaced. | Stronger |

| Risk boundary ignored or blurred | Sizing, invalidation, downside, or exit logic becomes flexible because participation feels urgent. | Crowd pressure is more dangerous when risk control weakens. | Stronger |

| Public information explains the move | Participants may be reacting similarly to the same news, data, earnings, policy, or fundamentals. | Shared reaction can look like herding even when imitation is not the main driver. | Weaker |

| Dominant actor or opaque mechanics explain the move | Flows, liquidity, positioning, or a concentrated participant may explain behavior better than crowd copying. | Not every broad move is a psychology-driven herd event. | Weaker or uncertain |

Practical Scenario

Example: A stock begins rising quickly and becomes widely discussed. More investors enter because the move is visible, not because their original criteria have changed. Some stop checking whether the risk is still defined, whether the valuation or structure still supports the idea, or whether the move is already crowded. That creates a stronger herd mentality reading.

The reading weakens if the same move is mainly explained by new public evidence that participants are independently incorporating, such as a material business update, a broad sector repricing, or a clear change in available information.

The same price movement can have different meanings. Crowd pressure may be present, but the interpretation depends on whether investors are copying visible behavior or independently responding to evidence.

Decision-Process Checks Around Herd Behavior

Herd mentality is most useful when it forces a process check. The issue is not whether the crowd exists. The issue is whether the crowd has changed the standard that would normally govern the decision.

- Criteria check: Is the decision still supported by the original evidence, or mainly by the fact that many others are acting?

- Risk check: Is the downside, sizing, or invalidation still defined, or has urgency blurred the boundary?

- Information check: Is the crowd reacting to new public evidence, or is participation itself becoming the evidence?

- Alternative check: Has the opposite view been considered, or has the dominant narrative made alternatives feel irrelevant?

- Timing check: Is the decision being made because conditions changed, or because the crowd moved first?

Process note: A crowd-driven environment does not automatically require following, fading, or avoiding the move. It requires separating participation pressure from evidence quality.

Common Mistakes When Reading Herd Mentality

| Mistake | Why it is risky | Cleaner reading |

|---|---|---|

| Calling every crowded move irrational | A popular move can still have evidence behind it. | Check whether participation is replacing analysis or only occurring alongside analysis. |

| Treating herding as a reversal signal | Crowded behavior can persist, pause, or fail without a clean timing signal. | Use herding as a behavior label, not as a timing tool. |

| Assuming the crowd is always wrong | Contrarian reactions can become emotional too. | Evaluate evidence quality instead of automatically opposing consensus. |

| Ignoring shared information | Markets can move together because participants receive the same facts. | Separate common reaction from imitation before applying a herd label. |

| Using the label to justify a weak plan | A psychology label does not define risk or validate execution. | Keep the decision tied to criteria, evidence, and risk boundaries. |

FAQ

Is herd mentality the same as crowd psychology?

No. Crowd psychology is broader and can include many types of group emotion, attention, and feedback. Herd mentality is narrower: it focuses on copying or aligning with the crowd because the crowd itself becomes persuasive.

Does a market bubble always mean herd mentality?

No. A bubble can include herd behavior, but it can also involve valuation detachment, speculative narratives, liquidity conditions, leverage, and feedback loops. Herd mentality is one possible ingredient, not the full definition.

Is every popular trade herd behavior?

No. A popular trade may still be supported by independent evidence. A stronger herd reading appears when popularity replaces the investor’s own criteria, risk boundary, or evidence checks.

Can herd mentality predict a market reversal?

No. Herd mentality can describe crowd participation pressure, but it does not predict timing, continuation, or reversal on its own.