A stock market bubble is a stock-market condition where prices rise far beyond underlying value because belief, speculation, and continued participation reinforce each other. A bubble is not the same as a strong rally, a high valuation, or a market correction, although those conditions can overlap with parts of a bubble classification.

Definition: A stock market bubble forms when price expansion becomes increasingly detached from underlying value and depends more on the expectation that future buyers will accept still higher prices.

The label describes a risk condition; it does not identify when a reversal, correction, or crash will begin.

The most important distinction is the source of the move. A durable rally can reflect better earnings, stronger cash flows, lower discount rates, or improved risk appetite. A bubble classification becomes more plausible when the price advance depends less on improving fundamentals and more on speculative continuation, crowd participation, and a self-reinforcing narrative.

Key Points

- A stock market bubble depends on price and value separating while speculative participation keeps reinforcing the move.

- A strong rally or stretched valuation does not automatically prove a bubble.

- Bubble signs can appear before a major reversal, but they do not provide precise timing.

- The label becomes more useful when valuation, sentiment, participation, and feedback-loop evidence align.

What Is a Stock Market Bubble?

A stock market bubble is a broad speculative expansion in equity prices where market value rises faster than the evidence supporting that value. The condition usually involves a growing gap between price behavior and underlying fundamentals, combined with belief that the advance can continue because participation keeps expanding.

Not every expensive market is a bubble. A market can trade at high valuation multiples because earnings growth is strong, interest rates are low, or investors are willing to pay more for durable cash flows. Bubble risk increases when the explanation shifts from value support toward narrative momentum, emotional participation, and dependence on later buyers.

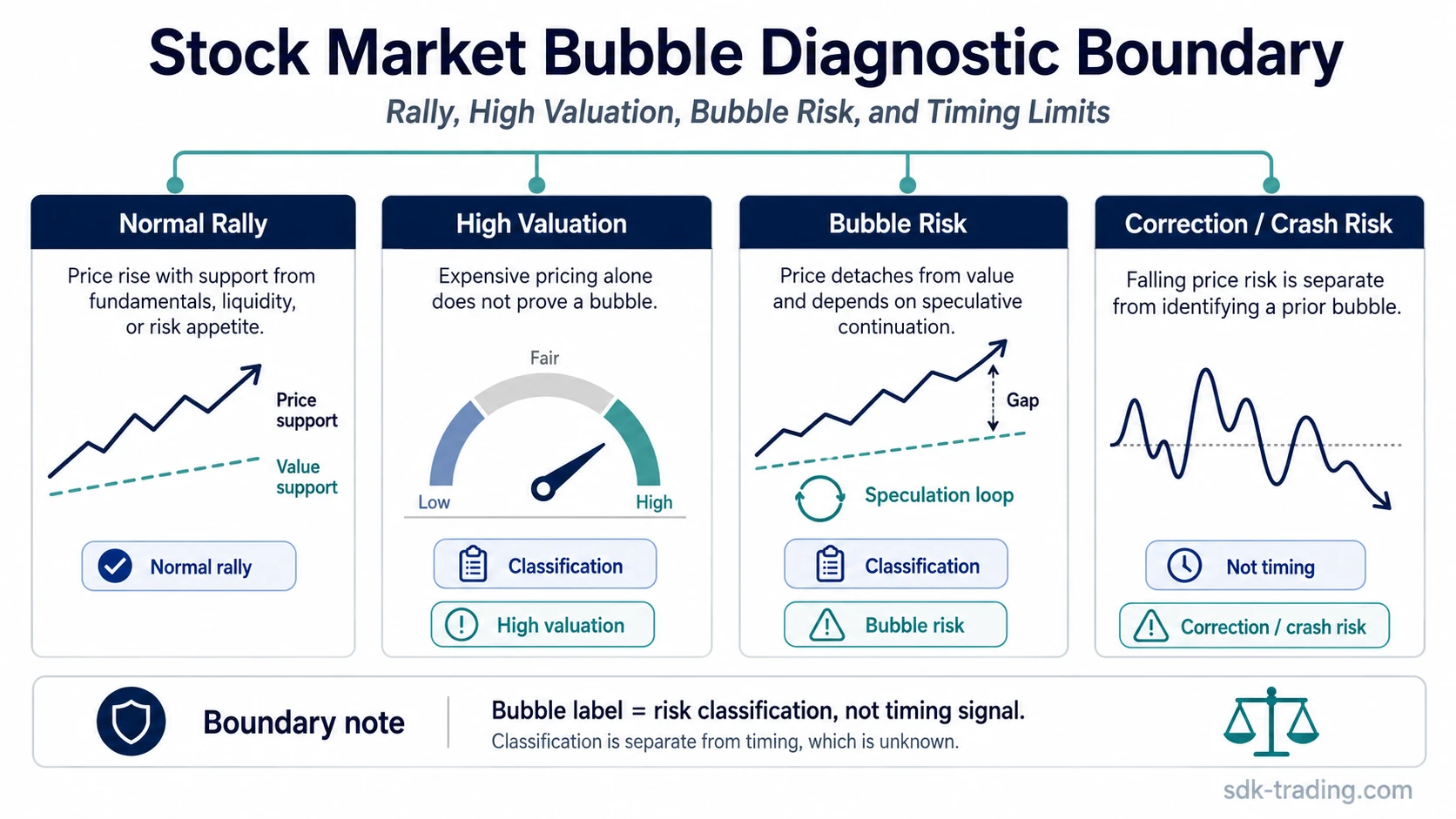

What Separates a Bubble From a Normal Rally?

The boundary is diagnostic, not mechanical. A bubble classification needs more than price strength. It depends on the relationship between price, value, participation, and the reason buyers keep accepting higher levels.

| Condition | What it means | What changes the bubble classification |

|---|---|---|

| Normal rally | Prices rise while the move remains connected to improving fundamentals, liquidity, or risk appetite. | That interpretation becomes less convincing as a bubble if earnings, cash flows, and valuation support improve alongside price. |

| High valuation | Stocks trade at elevated multiples, but high valuation alone does not prove speculative excess. | This points more strongly toward bubble risk when valuation stretches while justification becomes increasingly narrative-driven. |

| Stock market bubble | Price expansion becomes detached from underlying value and depends on continued speculative participation. | The classification becomes more defensible when sentiment, valuation, participation, and feedback-loop behavior align. |

| Correction or crash risk | Price begins to fall or volatility rises, but a decline is not the same thing as identifying a prior bubble. | The prior bubble classification becomes clearer only when the advance was already detached from value before the break. |

How Stock Market Bubbles Form

Stock market bubbles usually develop through a feedback loop. Prices rise, the advance attracts attention, more participants enter, and the rising price itself becomes part of the justification. As the loop matures, valuation discipline can weaken because recent price action appears to confirm the story.

Behavior matters, but it is not the whole concept. herd mentality in investing can amplify participation when investors treat the crowd as evidence. In a stock market bubble, that behavior matters because it can help detach price from underlying value rather than simply explain enthusiasm.

Mechanism note: A bubble does not require every participant to be irrational. It can also grow when rational participants believe they can exit before the feedback loop breaks, even while recognizing that prices are difficult to justify on fundamentals.

Common Signs of a Stock Market Bubble

Bubble signs are best treated as evidence categories rather than a checklist that gives a final answer. The more categories align, the more defensible the bubble classification becomes.

| Observable | Bubble-related interpretation | Limitation |

|---|---|---|

| Rapid price appreciation | Prices rise faster than the underlying value case appears to improve. | Fast gains can also occur during legitimate repricing. |

| Stretched valuation measures | Multiples or broad valuation gauges move well above normal context. | Valuation can stay elevated for long periods and does not time a reversal. |

| Euphoria or FOMO | Participation becomes driven by fear of missing further gains rather than disciplined valuation. | Strong sentiment alone does not prove detachment from value. |

| Greater-fool logic | Buyers depend on later buyers accepting even higher prices. | The logic must be separated from ordinary momentum and liquidity-driven repricing. |

| Concentration or narrow leadership | A small group of stocks carries a large share of index enthusiasm. | Concentration can also reflect genuine earnings leadership. |

Stock Market Bubble Stages

Bubble stages are descriptive labels, not a required sequence. Markets can skip, blur, or repeat parts of the lifecycle, so the structure is more useful for interpretation than for timing.

- Displacement: A new theme, policy shift, innovation, liquidity change, or growth story creates a reason for repricing.

- Boom: Price gains attract broader attention, and participation expands beyond early buyers.

- Euphoria: Confidence becomes self-reinforcing, valuation discipline weakens, and the story starts to justify almost any price.

- Profit-taking: Some participants reduce exposure, volatility may increase, and leadership can narrow.

- Panic or unwind: The feedback loop breaks if buyers no longer accept the prior narrative or higher prices.

Limitation: Stage labels are easier to apply after the fact. During the move, the same evidence can resemble a strong rally, late-cycle speculation, or early bubble behavior depending on valuation, participation, and market breadth.

Why Bubble Timing Is Difficult

A bubble label is a classification risk, not a timing signal. The label can describe an unstable condition without identifying when price will stop rising, when liquidity will change, or when confidence will break.

This matters because overvaluation can persist, speculative enthusiasm can intensify, and strong narratives can survive several failed warnings. The more useful question is not whether the bubble label sounds persuasive, but whether the evidence still supports price expansion without relying mainly on belief continuation.

Common mistake: Treating high valuation as automatic proof of a bubble creates false positives. Treating the bubble label as a crash forecast creates a different error because classification and timing are separate problems.

A Practical Stock Market Bubble Scenario

A broad index keeps advancing while valuation measures stretch and new participation concentrates around the belief that the advance itself validates the story. The bubble classification becomes more defensible when the move relies less on earnings or cash-flow support and more on the assumption that later buyers will keep accepting higher prices.

The same scenario remains unresolved if fundamentals improve fast enough to support the higher prices, participation broadens for durable reasons, or valuation evidence becomes less stretched. In that case, the move may still be risky, but the bubble classification becomes less defensible.

What Weakens a Bubble Reading?

A bubble classification weakens when the evidence no longer depends mainly on speculative continuation. The label becomes less convincing if earnings, cash flows, productivity, balance-sheet quality, or other value supports catch up with price.

- Fundamentals catch up: Higher prices become easier to justify because value support improves.

- Participation becomes durable: Buyers are not only chasing recent price action, but responding to stronger underlying evidence.

- Valuation pressure eases: Multiples normalize through earnings growth, price consolidation, or broader evidence improvement.

- The feedback loop fades without a disorderly break: The market stops depending on constant new enthusiasm to support the prior move.

Related Market Psychology Concepts

A stock market bubble includes psychological forces, but it is not only a psychology concept. The classification depends on price-value detachment, speculative participation, and the persistence of the feedback loop.

Broader market psychology helps explain why narratives spread, why confidence can become extreme, and why investors may discount contrary evidence during a speculative expansion.

FAQ

Why is a stock market bubble hard to identify before it bursts?

A bubble is hard to identify in real time because strong rallies, high valuations, and speculative excess can look similar until later evidence shows whether price was supported by value or mostly by belief continuation.

Is a strong stock market rally always a bubble?

No. A strong rally can be supported by improving earnings, liquidity, or risk appetite. A bubble reading needs evidence that price is becoming detached from underlying value.

Can bubble signs predict when a crash will happen?

No. Bubble signs can describe risk conditions, but they do not provide precise timing for a reversal, correction, or crash.

What weakens a stock market bubble reading?

The reading weakens when fundamentals catch up, valuation pressure eases, participation becomes more durable, or the move no longer depends mainly on speculative continuation.