Market psychology in trading is the collective emotional and cognitive pressure that shapes how market participants interpret risk, opportunity, uncertainty, and price movement.

It helps organize behavior behind participation, sentiment, narratives, volatility, and price response. Price structure and participation still need confirmation before the interpretation can carry weight.

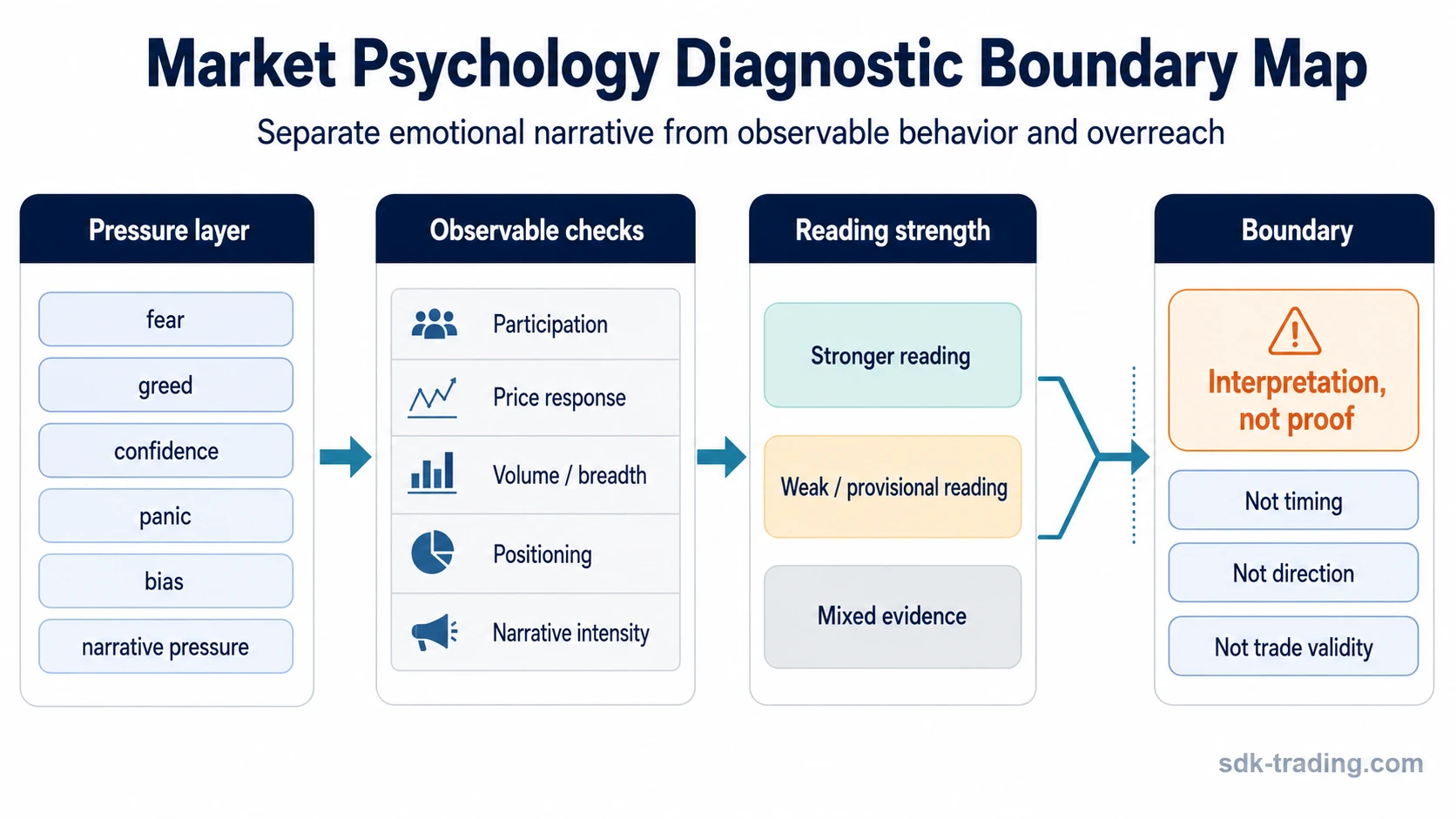

Definition: Market psychology is the shared emotional and cognitive backdrop behind market behavior. It includes fear, greed, confidence, panic, euphoria, doubt, bias, and narrative pressure as they appear through prices, volume, breadth, positioning, and sentiment gauges.

Key Points

- Market psychology describes collective pressure in financial markets, not the private emotions of one trader.

- Emotion and bias can affect participation, price response, volatility, volume, breadth, and sentiment indicators.

- Market sentiment is narrower than market psychology because it usually describes current attitude or a measurable gauge.

- A stronger reading needs observable behavior, not only a story about fear or greed.

- The label organizes interpretation, but it does not validate a trade or predict what price must do next.

What Market Psychology Means in Trading

Market psychology connects behavioral finance with chart behavior. Participants do not process information in a perfectly neutral way. They respond to gains, losses, recent price action, news, uncertainty, peer behavior, and narratives that may amplify confidence or caution.

In trading, the concept matters because price movement is not only a mechanical response to fundamentals. A move can also reflect changing risk appetite, defensive positioning, crowded expectations, or emotional exhaustion after an extended advance or decline.

Boundary: A market psychology reading is an interpretation layer. It can help explain why participation looks urgent, hesitant, crowded, or defensive, but it does not replace price structure, risk definition, confirmation, invalidation, or a separate trading plan.

How Market Psychology Shows Up in Price Behavior

Market psychology becomes more visible when emotion and participation appear together. A fast move, a volatility expansion, a volume surge, or a sentiment extreme may matter more when it also changes how price behaves around known areas of supply, demand, support, resistance, or prior acceptance.

Observable pressure can appear through several layers at once:

- Participation: more traders or investors reacting to the same narrative, risk event, or price level.

- Price response: strong acceptance, failed acceptance, sharp rejection, stalled recovery, or repeated inability to hold a tested area.

- Volume and breadth: expanding activity, narrowing participation, or broad confirmation across many instruments.

- Positioning: crowded exposure, defensive hedging, leveraged participation, or forced adjustment.

- Narrative intensity: repeated explanations that make one interpretation feel obvious before price behavior has confirmed it.

Emotions and Biases Behind Market Psychology

Market psychology often reflects a combination of emotion and cognitive bias. Fear may increase defensive behavior. Greed may support aggressive participation. Euphoria can reduce caution after an extended move. Panic can compress decision-making when price moves quickly against crowded expectations.

Biases can make those emotions more persistent. Confirmation bias can cause participants to seek only evidence that supports an existing view. Anchoring can keep attention fixed on a prior level or narrative. Recency bias can make the latest move feel more reliable than it is. Loss aversion can make participants react more strongly to downside pressure than to comparable upside movement.

| Emotion or bias | How it can appear in market behavior | Interpretation limit |

|---|---|---|

| Fear | Defensive positioning, faster selling, wider volatility, reduced willingness to hold risk. | Fear alone does not prove that price must keep falling. |

| Greed | Aggressive participation, late chasing, tolerance for weaker evidence, or acceptance of thinner risk boundaries. | Strong demand can still fail if acceptance and follow-through do not appear. |

| Euphoria | One-sided confidence after an extended advance, crowded optimism, or repeated dismissal of failed follow-through. | An overheated mood is not automatic reversal evidence. |

| Panic | Urgent liquidation, disorderly movement, rapid repricing, or failed recovery attempts. | A panic label needs observable stress, not only a large candle or headline reaction. |

| Confirmation bias | Selective attention to evidence that supports the dominant narrative. | A popular explanation can be incomplete if price behavior contradicts it. |

| Recency bias | Assuming the latest move or latest regime will continue because it is most visible. | Recent movement needs context from structure, participation, and alternative explanations. |

Market Psychology vs Market Sentiment, Trading Psychology, and Crowd Psychology

Several nearby concepts overlap, but they do not describe the same thing. Market psychology is the broader collective backdrop. Sentiment is usually the current attitude or gauge. Trading psychology is the individual decision process. Crowd behavior and imitation describe narrower forms of collective pressure.

| Concept | Main focus | Boundary |

|---|---|---|

| Market psychology | Broad collective emotional and cognitive pressure influencing market behavior. | Useful for interpretation, but not proof of trade validity. |

| Market sentiment | Current attitude, mood, or measurable gauge around a market or asset class. | Narrower than psychology because it often captures a snapshot rather than the full behavioral backdrop. |

| Trading psychology | Individual trader discipline, emotion, bias, decision quality, and process control. | Focused on the trader’s own decisions rather than collective market behavior. |

| crowd psychology in trading | Group pressure, crowd behavior, and the influence of visible participation. | A narrower group-behavior layer inside the broader psychology of markets. |

| Herd mentality in investing | Imitation behavior and following others instead of independent criteria. | Requires evidence of imitation pressure, not just many participants moving in the same direction. |

| Market cycle psychology | Emotional sequence across cycle phases such as optimism, excess, fear, and repair. | Phase labels can organize context, but markets do not always move through a clean emotional sequence. |

| Stock market bubble | Extreme speculative excess and stretched belief in future upside. | Not every emotional or optimistic market is a bubble. |

Indicators That Can Reflect Market Psychology

Indicators can help observe market psychology, but they should be treated as evidence layers rather than mechanical signals. A single gauge may show stress, confidence, fear, or crowding, yet the interpretation changes when price behavior, breadth, liquidity, news, and positioning point in different directions.

| Observable | What it can reflect | Why it is not enough alone |

|---|---|---|

| Volatility gauges such as VIX | Demand for protection, uncertainty, or stress in equity markets. | Volatility can rise for several reasons and does not identify timing by itself. |

| Put/call ratio | Options positioning and relative demand for downside or upside exposure. | Hedging, speculation, and institutional positioning can produce different meanings. |

| Market breadth | How widely participation supports a move across many stocks or instruments. | Weak breadth can persist, and strong breadth can still fade if acceptance fails. |

| High-low measures | Whether more instruments are breaking to new highs or new lows. | The signal needs context from trend, volatility, and participation quality. |

| Margin debt or leverage measures | Risk appetite, speculative exposure, or vulnerability to forced adjustment. | Leverage data may be delayed depending on the source and does not directly time market turns. |

| Sentiment surveys and gauges | Reported optimism, pessimism, confidence, or caution. | Expressed mood can differ from actual positioning and price behavior. |

Interpretation note: Indicators are most useful when compared against each other. When sentiment, participation, price response, and positioning point toward the same behavioral pressure, the reading becomes more defensible. When they conflict, the market psychology label should stay provisional.

Market Psychology Diagnostic Boundary

A market psychology reading becomes useful only when the label is separated from proof. The same emotional narrative can be strong, weak, or overextended depending on what the market actually does around participation, price acceptance, and follow-through.

Narrative intensity is only useful when it can be checked against participation, acceptance, breadth, positioning, or another observable layer.

| Reading strength | What supports it | What weakens it | What becomes overreach |

|---|---|---|---|

| Stronger market psychology reading | Sentiment extreme aligns with participation, price behavior, volume, breadth, positioning, and narrative intensity. | Evidence is mixed, participation is narrow, or price fails to confirm the emotional interpretation. | The label is used as proof of a market call or a trading decision. |

| Weak or provisional reading | One or two signs suggest emotion, but price acceptance, breadth, or positioning remains unclear. | The move is explainable by ordinary volatility, liquidity, news, or fundamentals without clear collective pressure. | A thin emotional explanation is treated as if it explains the whole market move. |

| Invalid or overextended reading | None; the label is being carried by narrative more than observable behavior. | Price action contradicts the narrative, participation does not support it, or better explanations dominate. | Fear, greed, or crowd mood is used to bypass criteria, risk boundaries, or invalidation. |

Market Psychology Example in Context

Price advances into a prior resistance area after a long upward move. Optimistic commentary becomes more common, participation expands, and a sentiment gauge shows elevated confidence. The first reaction above resistance is tempting to label as broad enthusiasm.

The reading remains incomplete if price cannot hold above the tested area, breadth narrows, and the next recovery attempt stalls. A stronger market psychology interpretation would need the emotional backdrop to align with acceptance, participation quality, and follow-through. A weaker interpretation would treat the move as ordinary volatility or a failed test until better evidence appears.

Common Mistakes and Limits

Market psychology becomes risky when it is used as a shortcut. Emotional language can sound convincing, but a convincing label is not the same as evidence.

| Mistake | Safer interpretation |

|---|---|

| Mistaking any large move for collective psychology | Large movement begins the question. The stronger test is whether participation, acceptance, and context support a behavioral reading. |

| Treating sentiment extremes as timing proof | Extreme optimism or pessimism can persist. Price response and invalidation still matter. |

| Ignoring fundamentals, liquidity, or news | Some moves are better explained by new information, structural liquidity, or valuation changes than by crowd emotion alone. |

| Blurring market psychology with personal discipline | Collective market behavior and individual trading discipline are related, but they solve different problems. |

| Turning a market view into a trade decision | A market view and a trade expression remain separate decisions. Criteria, risk, and invalidation still need their own check. |

Limit: Market psychology can clarify why behavior appears stretched, defensive, crowded, or unstable. It cannot confirm that a trade is valid, that a reversal must occur, or that a trend must continue.

Related Concepts

Market psychology is easier to use when nearby concepts stay separate. Market sentiment captures the current mood or gauge. Herd mentality focuses on imitation. A bubble describes extreme speculative excess, not every emotional market.

Cycle-phase psychology adds another layer by describing how emotions may shift across different parts of a market cycle, while market psychology remains the broader collective behavior lens.

FAQ

What is market psychology in trading?

Market psychology in trading is the collective emotional and cognitive pressure that influences how participants react to risk, opportunity, price movement, uncertainty, and market narratives.

Is market psychology the same as market sentiment?

No. Market sentiment is usually a current attitude or measurable gauge, while market psychology is the broader behavioral backdrop that can include emotion, bias, positioning, narratives, and participation.

Can market psychology predict price direction?

No. Market psychology can help interpret behavior, but it does not prove timing, direction, continuation, reversal, or trade validity.

Which indicators can reflect market psychology?

Volatility gauges, put/call ratios, breadth, high-low measures, leverage data, positioning data, and sentiment surveys can reflect parts of market psychology, but none should be treated as proof on its own.