Market cycle psychology becomes risky when a trader treats an emotional phase label as confirmation instead of checking whether planned criteria still hold.

Market cycle psychology in trading describes how fear, greed, FOMO, panic, relief, hope, and euphoria can shape decisions as price moves through perceived market phases. The useful trading angle is process control, not prediction. A phase label may explain why pressure feels intense, but it does not confirm what price will do next.

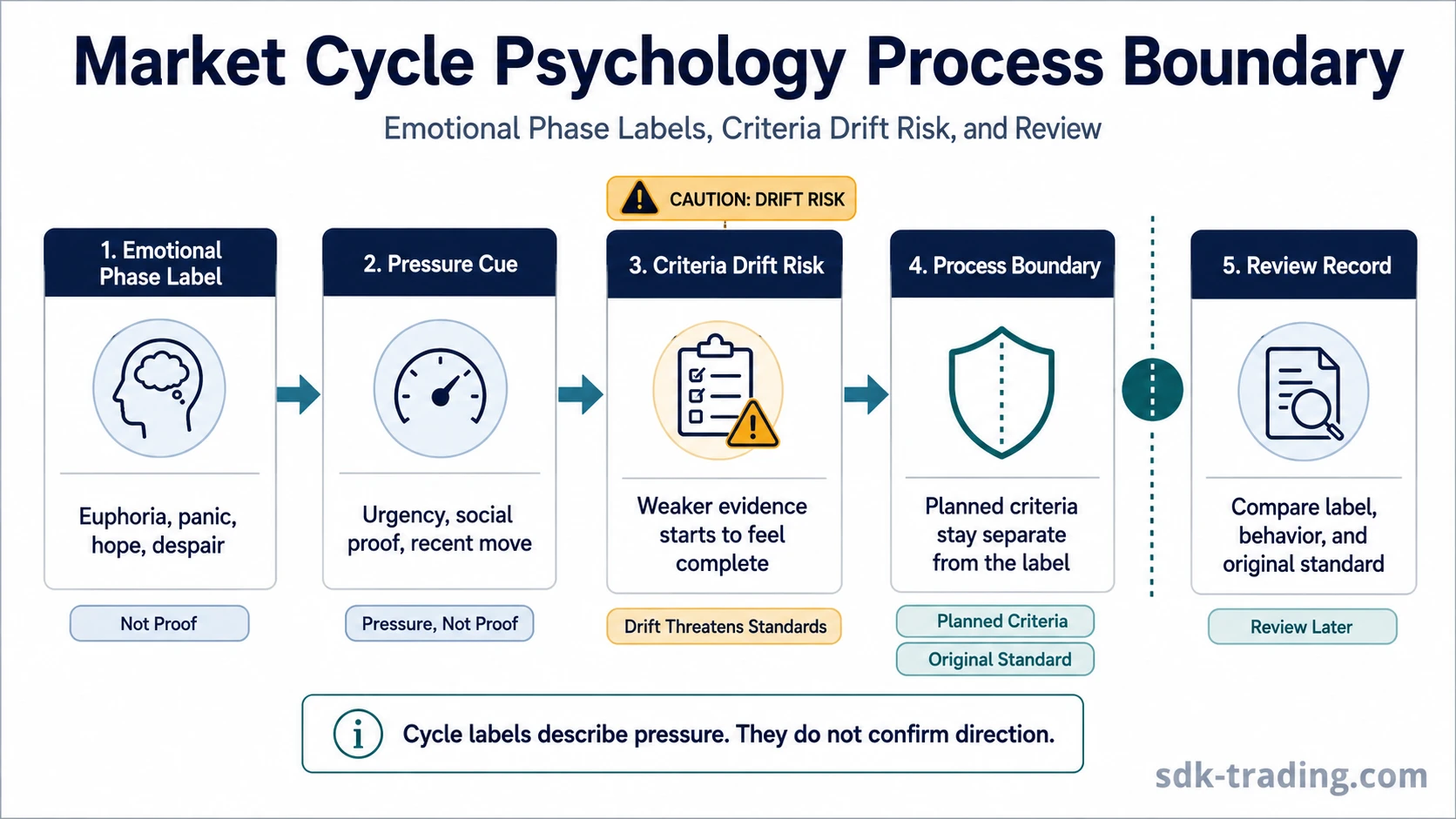

Definition: Market cycle psychology is the emotional behavior that can appear around perceived cycle phases, especially when traders attach a strong label to the market and adjust standards before the chart has provided enough process evidence.

Key Points

- Market cycle psychology can describe emotional pressure, but it does not confirm direction by itself.

- Cycle labels become dangerous when they replace planned criteria, risk boundaries, or later review.

- FOMO, panic, euphoria, and despair can make weak evidence feel more complete than it is.

- The safer reading separates the emotional label from observable price behavior, acceptance, rejection, and process discipline.

What Market Cycle Psychology Means in Trading

In trading, market cycle psychology connects emotional pressure with perceived cycle stages. Traders may describe a market as optimistic, euphoric, anxious, panicked, despairing, or hopeful. Those labels can be useful as language for crowd emotion, but they are still interpretations.

A cycle label becomes more useful when it is kept separate from the decision process. The trader can notice that the market feels euphoric or fearful while still requiring planned criteria, defined invalidation, and later review. That separation keeps the label from becoming a shortcut.

Market psychology covers the broader field of emotional and behavioral influence in markets. Market cycle psychology is narrower: it focuses on how perceived cycle stages can pressure trader standards.

Why Emotional Phase Labels Create Pressure

Phase labels can feel persuasive because they give a messy market a simple story. When price has already moved sharply, the label may appear to explain what has happened and what might happen next. That is where the risk begins.

During a rising phase, optimism can turn into urgency. A trader may fear being left behind and start accepting weaker evidence. During a falling phase, fear can turn into forced avoidance or reactive decisions. In both cases, the problem is not the emotion itself. The problem is the quiet shift in standards.

That pressure can also produce classic buy-high / sell-low behavior: confidence after a sharp advance can make late participation feel reasonable, while fear after a sharp decline can make reactive exits feel safer than the original process.

| Perceived phase pressure | Common decision risk | Safer process question |

|---|---|---|

| Optimism or euphoria | Chasing because the market feels strong | Do the planned criteria still exist, or did the label replace them? |

| Anxiety or panic | Reacting before the setup is actually invalidated | Has the original condition failed, or is the reaction mainly emotional? |

| Despair or disbelief | Dismissing early improvement because recent losses dominate memory | Is price behavior changing, or is the old phase label still controlling the read? |

| Hope or relief | Calling a recovery complete before acceptance is visible | Has the market accepted the new area, or is the read still provisional? |

The Common Misread: Treating a Cycle Label as Confirmation

The most important mistake is treating a phase label as if it were evidence. A trader may say the market is in panic, euphoria, accumulation, distribution, capitulation, or recovery and then act as though the label has confirmed the next move.

A label can organize observation, but it cannot replace observation. Price may look euphoric and still continue rising. Price may look fearful and still fail to recover. The label describes a possible emotional condition; it does not prove acceptance, rejection, reversal, continuation, or exhaustion.

Limitation: A market-cycle label is not a trading signal, not proof of direction, and not a decision system. It remains only one interpretation until price behavior, context, criteria, and later review support or weaken it.

Cycle Label Misread vs Safer Interpretation

The cleaner distinction is between naming the emotional phase and checking whether the decision process has changed. The label may be reasonable, but the process still needs evidence.

| Cycle label misread | Why it is risky | Safer interpretation |

|---|---|---|

| “The market is euphoric, so the move must be near the end.” | The label turns emotion into a timing claim. | Euphoria may warn that expectations are stretched, but price still needs evidence of rejection, failed acceptance, or weakening participation. |

| “The market is panicking, so the bottom must be close.” | Fear is treated as automatic exhaustion. | Panic can mark pressure, but recovery remains unresolved until selling pressure eases and buyers can reclaim meaningful areas. |

| “The cycle has turned, so weaker criteria are acceptable.” | The story lowers the standard for action. | The original criteria should remain visible. If they are missing, the phase label should not fill the gap. |

| “Everyone is acting the same way, so the phase is obvious.” | Social proof can make a weak read feel confirmed. | Behavioral consensus should be compared with actual structure, follow-through, and reviewable evidence. |

How Emotional Pressure Can Change Process Adherence

Market cycle psychology matters most when emotional pressure changes the trader’s process. FOMO can make late participation feel justified. Panic can make a planned review feel too slow. Euphoria can make caution feel unnecessary. Despair can make improvement feel impossible.

The process problem is criteria drift. A trader begins with one standard, then softens that standard because the market feels urgent, crowded, or emotionally obvious. The change may be subtle: a weaker setup is accepted, a planned review is skipped, or an unresolved condition is treated as complete.

Crowd psychology in trading focuses on how group emotion and social pressure shape behavior. Market cycle psychology can include that pressure, but the narrower issue here is whether the phase label caused the trader to change standards.

Process note: The useful review question is not whether the phase label sounded convincing. The useful question is whether the trader changed criteria because the market felt like it was in a familiar emotional stage.

Market Cycle Psychology Example in Context

Example: Price has advanced for several sessions and starts pushing into a prior resistance area. Commentary around the move feels increasingly confident, and the market begins to look euphoric. The tempting read is to label the move as late-cycle excitement and assume exhaustion is near.

A safer reading keeps the label separate from confirmation. If price keeps accepting the upper area, the euphoria label does not prove reversal. If price briefly trades above the area, closes weak, and the next recovery attempt stalls, the emotional label becomes more relevant because behavior has started to support a failed-acceptance read. If neither acceptance nor rejection is clear, the cycle label remains unresolved.

Market Psychology, Crowd Psychology, Herd Mentality, and Bubbles

Market cycle psychology overlaps with nearby trading psychology concepts, but each one answers a different question. The distinction matters because broad emotional language can blur separate decision problems.

| Concept | Main focus | How it differs from market cycle psychology |

|---|---|---|

| Market psychology | Broad emotional and behavioral forces in markets | It covers the wider behavioral field, while market cycle psychology focuses on emotional phase labels and process drift. |

| Crowd psychology in trading | Group emotion and social pressure | It emphasizes collective behavior, while cycle psychology emphasizes how phase labels affect criteria. |

| Herd mentality in investing | Imitation of majority behavior | It focuses on copying the crowd. Herd mentality in investing can appear inside a cycle phase, but imitation is not the same as phase interpretation. |

| Stock market bubble | Speculative excess and stretched participation | A stock market bubble can involve euphoria, but a bubble reading needs more than a single emotional label. |

Review Boundary for Cycle-Label Drift

A review boundary makes the drift visible after the decision. Instead of asking whether the label was right, the review checks whether the trader followed the original process while the label was emotionally persuasive.

- Original criteria: What had to be present before the decision?

- Changed standard: Was any requirement softened after the market was labeled as euphoric, fearful, panicked, or hopeful?

- Evidence gap: Did the label replace price behavior, acceptance, rejection, or follow-through?

- Pressure source: Did urgency, social proof, recent losses, or recent gains change the interpretation?

- Review record: Can the decision be checked against the original plan without relying on hindsight?

Boundary: Review does not make the original decision right or wrong by itself. It only shows whether the process stayed intact while the market felt emotionally convincing.

FAQ

When does market cycle psychology become risky?

It becomes risky when the trader treats a perceived phase label as confirmation and starts changing criteria before price behavior, context, and reviewable evidence support the interpretation.

Can market cycle psychology predict the next market move?

No. It can describe emotional pressure and possible behavior patterns, but it does not predict direction or confirm a trade by itself.

Why can cycle labels create poor decisions?

Cycle labels can make an incomplete read feel complete. The risk is that the trader softens criteria because the market feels euphoric, fearful, panicked, or hopeful.

How should a trader review a market-cycle label?

The review should compare the label with the original criteria, the observed market behavior, and any change in standards caused by emotional pressure.