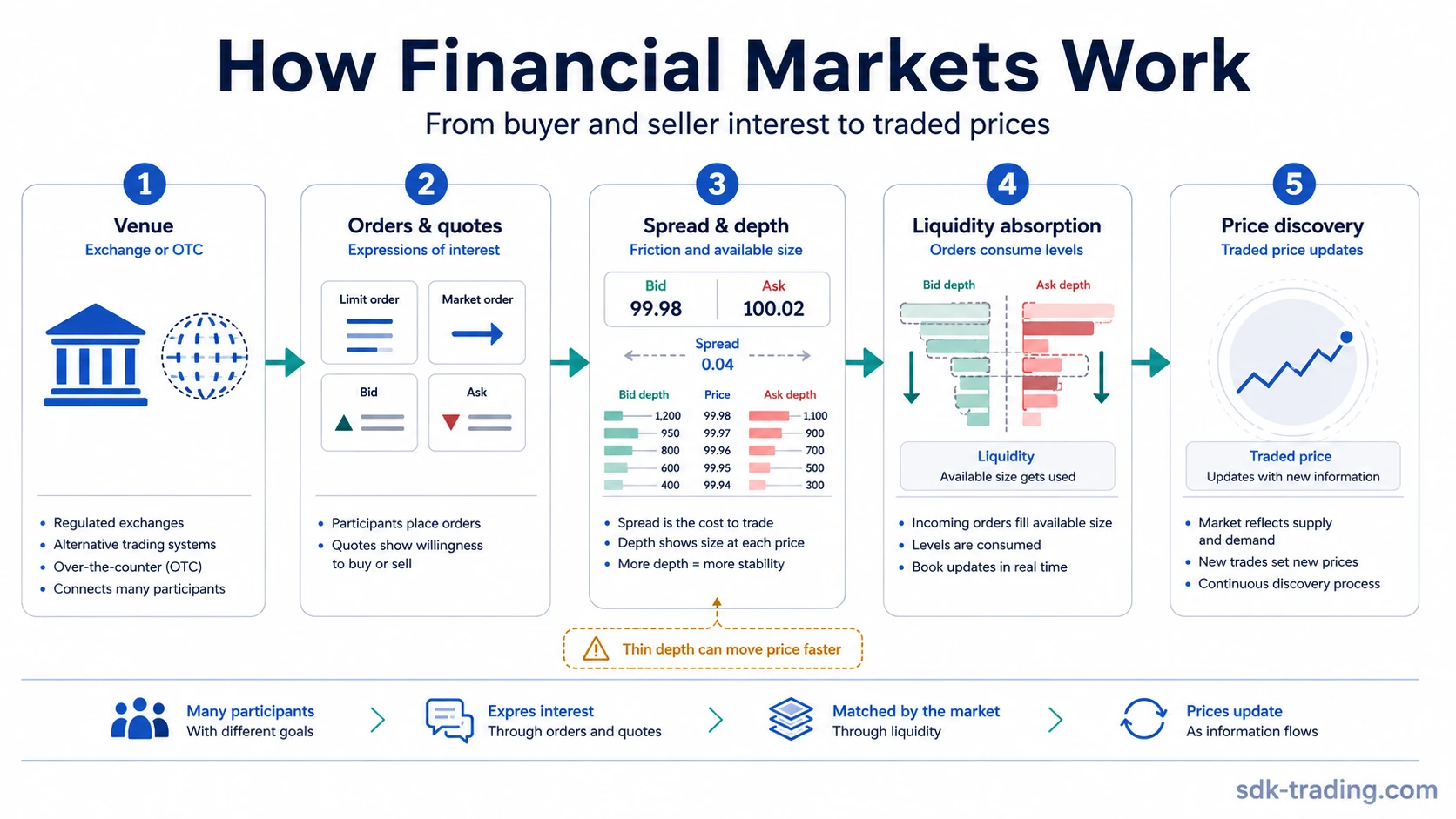

Financial markets work by organizing trading venues, orders, quotes, liquidity, and rules into a process that turns buyer and seller interest into traded prices.

A market is not just a place where prices appear. It is a structure that decides how participation is displayed, how orders meet, how quickly liquidity can be used, and how much friction exists between immediate buyers and sellers.

Definition: Financial markets work by turning buyer and seller interest into executable prices through venues, orders, quotes, liquidity, and transaction rules.

Key Points

- Venues organize where buyers and sellers interact.

- Orders and quotes create executable prices.

- Liquidity affects how smoothly transactions are absorbed.

- Price discovery changes as participation, depth, and urgency change.

Market Venues Organize Buyer and Seller Interest

The process starts with the venue. A venue gives participants a shared structure for submitting orders, viewing prices, accessing liquidity, and completing transactions under a rule set.

On a centralized exchange, orders are usually processed through a common matching system. That shared process helps concentrate liquidity, display bids and offers, and apply rules such as price priority and time priority.

Rules, clearing processes, and venue standards help define how transactions are matched, confirmed, and settled, even though they do not remove market risk.

Over-the-counter markets work differently. Instead of one central matching book, dealers or counterparties quote prices directly. Liquidity is still available, but it is distributed through relationships, quote streams, and dealer balance-sheet capacity rather than one visible exchange book.

| Market structure | How interaction works | What it changes |

|---|---|---|

| Centralized exchange | Orders meet inside a shared matching process. | Liquidity and prices are more visible in one venue. |

| OTC market | Dealers or counterparties quote directly. | Liquidity depends more on quote relationships and dealer participation. |

Orders, Quotes, and Price Discovery

Price discovery begins when participants express interest through orders and quotes. The bid is the highest active buying price. The ask is the lowest active selling price. The spread is the gap between them.

A market order prioritizes immediate execution and accepts available liquidity. A limit order sets a price boundary and waits until the market reaches that condition. These two behaviors constantly reshape the available book because some participants demand immediacy while others provide resting liquidity.

A traded price is not assigned from outside the market. It updates as orders arrive, quotes change, depth is consumed, and participants adjust what they are willing to buy or sell at the current moment.

Common mistake: A market price is not assigned by a single authority. It is discovered through executable interest, available liquidity, and the rules of the venue or quoting system.

| Term | Meaning | Why it matters |

|---|---|---|

| Bid | Highest active buying price | Shows where visible buying interest currently sits. |

| Ask | Lowest active selling price | Shows where visible selling interest currently sits. |

| Spread | Distance between bid and ask | Shows the friction between immediate buyers and sellers. |

| Depth | Available size at nearby prices | Shows how much activity can be absorbed before price moves further. |

Liquidity Explains Why Price Can Move Quickly

Liquidity describes how easily transactions can be absorbed without creating excessive price movement. A market can look calm when depth is available on both sides, but it can reprice quickly when that depth disappears.

| Condition | Implication | Limitation |

|---|---|---|

| Depth is available near the current price | Orders can usually be absorbed with less friction. | Visible depth can change or be pulled as conditions shift. |

| The spread widens | Immediate execution becomes more costly or less certain. | A wide spread does not explain the cause by itself. |

| One side of the book becomes thin | A cluster of urgent orders can move through several levels quickly. | The move still needs context before it can be interpreted as a broader market shift. |

A common scenario is a thin order book near the current price. If several urgent buy or sell orders arrive while nearby depth is low, those orders can consume multiple price levels before enough opposite liquidity appears. The movement may look sudden, but the mechanism is liquidity absorption rather than a guaranteed change in broader market direction.

Primary and Secondary Markets Serve Different Jobs

Primary markets are where new securities are issued and capital is raised. Secondary markets are where those securities trade between participants after issuance.

The distinction matters because the first process creates or distributes a security, while the second process continually reprices it through trading activity. Most chart-based market observation happens in secondary markets, where existing instruments change hands and prices update through ongoing participation.

Participants Shape How the System Works

Financial markets connect participants with different roles, constraints, and time horizons. Issuers raise capital, investors and traders seek exposure or liquidity, brokers provide access, exchanges organize matching, dealers quote prices, and regulators define parts of the rule environment.

- Issuers create securities or raise capital.

- Investors and traders create demand, supply, and changing urgency.

- Brokers transmit orders into market infrastructure.

- Dealers and market makers quote prices and affect spreads, depth, and execution conditions.

- Exchanges and clearing systems organize matching, settlement, and transaction rules.

These roles overlap in practice, but the mechanism stays the same: participation becomes visible through orders, quotes, and executed transactions. The market price changes as the balance between available liquidity and urgent demand changes.

Market Mechanics, Market Types, and Price Drivers Are Different

Market mechanics explain how trades happen. Price drivers explain why buyers or sellers become more active. Economic data, earnings expectations, policy changes, risk appetite, and positioning can all influence participation, but the price still changes through orders, quotes, liquidity, and execution.

Market categories answer a different question. Stock, bond, currency, derivatives, and commodity markets differ by instrument and structure, but each still depends on some version of buyer-seller interaction, quote formation, liquidity, and transaction rules.

The same mechanics can behave differently across market cycles, because liquidity, risk appetite, participation, and volatility do not stay constant across every regime.

FAQ

What is price discovery in financial markets?

Price discovery is the process through which traded prices update as buyers and sellers submit orders, change quotes, remove liquidity, or complete transactions. The visible price comes from market interaction rather than a fixed external assignment.

Why can prices move quickly without major news?

Prices can move quickly when liquidity is thin, when one side of the market withdraws, or when urgent orders consume several nearby price levels. In those conditions, the structure of available liquidity can matter as much as new information.

What is the difference between an exchange and an OTC market?

An exchange centralizes matching under a shared rule set, while an OTC market relies more on dealer relationships and direct quotes. Both connect buyers and sellers, but they organize liquidity in different ways.

How do primary and secondary markets differ?

Primary markets handle new issuance and capital raising. Secondary markets handle later trading between participants, where existing securities are repriced through ongoing buying, selling, liquidity, and execution.