Market cycles are recurring phases or behavior states in financial markets, where price direction, participation, volatility, liquidity, and sentiment change over time.

They help describe market conditions, but they are not precise tools for calling exact tops, bottoms, entries, or exits. A cycle label is useful only when it stays conditional: the market may appear to be shifting from one state to another, but later behavior still has to confirm whether that shift is being accepted or rejected.

Definition: Market cycles are recurring changes in financial-market behavior. They describe how markets can move through accumulation, expansion, distribution, contraction, or other behavior states as participation, liquidity, volatility, and price response change.

Key Points

- Market cycles describe recurring market behavior, not a fixed calendar sequence.

- Cycle phases are easier to label after the fact than in real time.

- Timeframe, market type, liquidity, volatility, and participation can all change the interpretation.

- A phase interpretation weakens when price action, participation, and surrounding market evidence do not align.

What Are Market Cycles?

Market cycles are the broad shifts in behavior that appear as markets move from quiet accumulation or base-building conditions into expansion, then into distribution, topping behavior, contraction, or renewed stabilization. The labels are useful because they organize changing market conditions into a readable framework.

The labels are also imperfect. A market does not have to pass through every phase cleanly, and the same asset can look constructive on one timeframe while still being weak on another. A cycle framework should describe what is happening, not force the market into a sequence it has not shown.

In trading and technical analysis, the practical value is classification. A trader can use the idea of market cycles to separate a quiet range, a strong expansion, a late-stage advance, and a weakening decline. That classification remains only a working interpretation, not a prediction.

Market Cycle Reading Boundary

A market-cycle interpretation starts with a simple question: has market behavior changed enough to justify a different view of the environment? The answer depends on more than price direction. Participation, volatility, liquidity, sentiment, breadth, and the market’s response to new information all matter.

| Boundary question | Safer interpretation | Common overreach |

|---|---|---|

| What is the concept? | A way to classify recurring market behavior across changing conditions. | Treating the label as proof that a new phase has already started. |

| What supports the reading? | Price, participation, volatility, and related-market behavior point in the same direction. | Using one strong move as enough evidence for a full cycle shift. |

| What weakens the reading? | The move fades back into the prior range, participation narrows, or volatility expands without acceptance. | Assuming that a sharp move must begin a lasting trend. |

| What invalidates the reading? | Later behavior contradicts the phase label through failed acceptance, failed continuation, or conflicting market context. | Keeping the same phase label after the market has stopped confirming it. |

The strongest interpretations are not built from one chart feature. They are built from agreement between behavior, context, and follow-through. A phase label becomes less reliable when phases overlap, the timeframe is unclear, or related markets send conflicting messages.

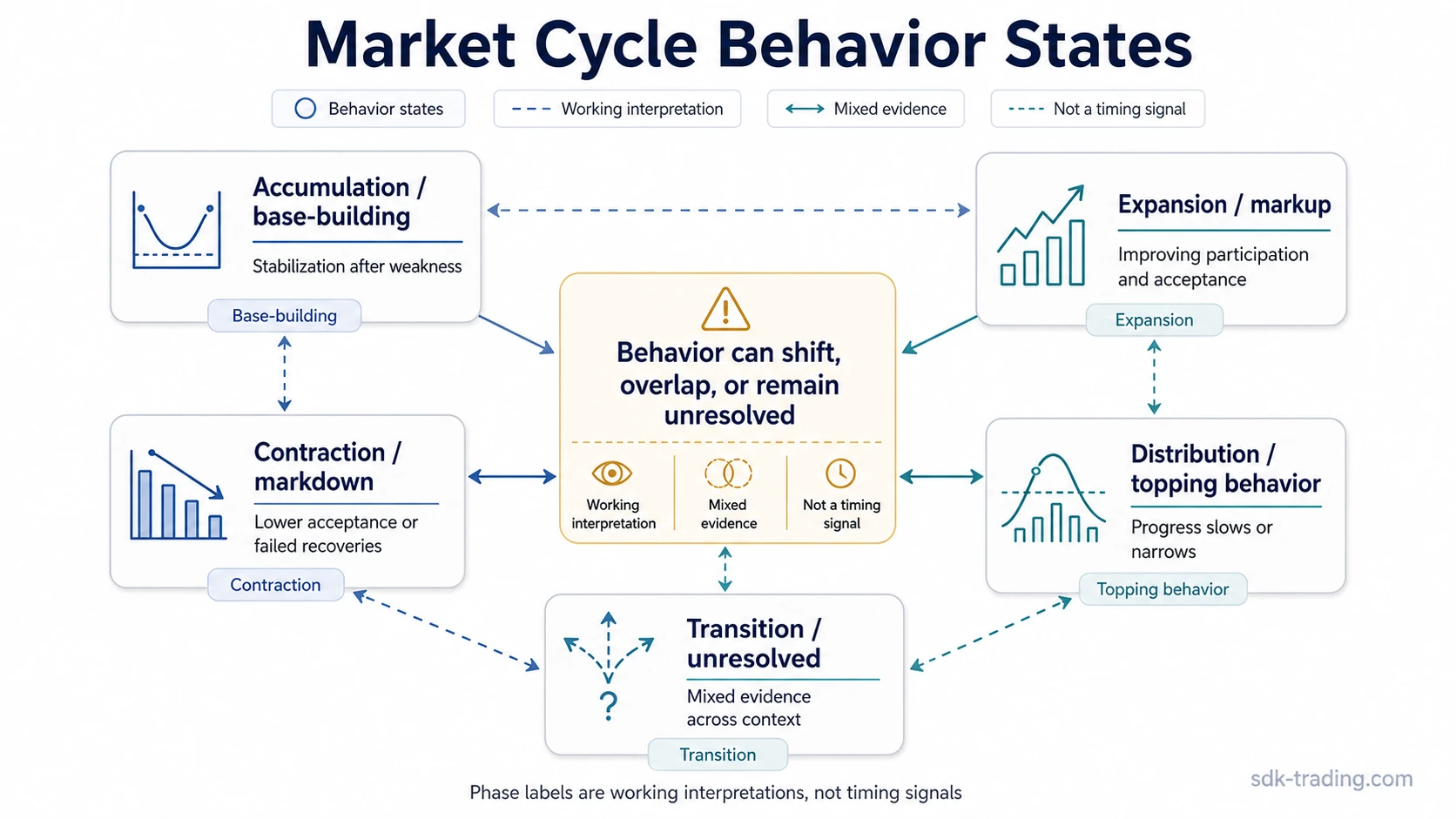

Market Cycle Phases and Behavioral States

Market cycles are often described with phase labels. Those labels are useful, but they should be treated as behavioral states rather than mandatory steps. Markets can compress phases, revisit earlier ranges, fail to confirm an apparent transition, or show different states across different assets.

| Phase or state | Typical observable behavior | Interpretation limit |

|---|---|---|

| Accumulation or base-building | Price stabilizes after weakness, volatility may contract, and selling pressure may become less effective. | A quiet range is not automatically accumulation; it can also be temporary balance before another decline. |

| Expansion or markup | Price leaves a prior range, participation improves, and pullbacks may become shallower if acceptance holds. | A breakout or strong advance does not prove durable expansion unless follow-through remains supportive. |

| Distribution or topping behavior | Upward progress slows, volatility may increase, rallies may lose quality, and participation can narrow. | Sideways behavior near highs is not always distribution; it can also be consolidation before continuation. |

| Contraction or markdown | Price breaks lower, recoveries fail more often, volatility may expand, and risk appetite can deteriorate. | A decline does not define the whole cycle by itself; the reaction after the decline matters. |

| Transition or unresolved state | Signals conflict, ranges widen, price rejects both extremes, or different timeframes disagree. | Forcing a clean phase label too early can create false confidence. |

The transition state matters because many cycle errors happen there. The market may look as if it has started a new phase, but the move remains unresolved until price behavior, participation, and context give a clearer answer.

How Market Cycles Work

Market cycles develop because market participants respond differently as conditions change. Demand and supply shift, liquidity expands or contracts, volatility changes, and sentiment moves between caution and confidence. These forces do not operate in isolation.

Price can rise because participation broadens, because liquidity improves, because expectations become more favorable, or because sellers are no longer able to push price lower. Price can fall because liquidity tightens, risk appetite weakens, volatility rises, or buyers stop supporting prior ranges. The mechanism behind a move is often more important than the move alone.

What moves market prices is the underlying driver question. Market cycles organize those drivers into changing states: early stabilization, expansion, late-stage pressure, contraction, and unresolved transition.

Market Cycles Across Timeframes and Markets

A cycle interpretation depends heavily on the observation window. A short-term chart can show an expansion while the broader structure is still a recovery inside a larger decline. A long-term chart can still be in a broad advance while shorter windows go through corrections, volatility bursts, or temporary distribution behavior.

Trading timeframes explained is directly connected to cycle interpretation because the same market can show different behavior states depending on whether the focus is intraday, swing, position, or long-term analysis.

Market type also matters. Equity indices, individual stocks, commodities, currencies, crypto assets, and fixed-income markets can respond to different drivers. Some markets may show strong trend persistence, while others may cycle through ranges more often. Types of financial markets helps separate those environments before applying the same cycle label everywhere.

Market Cycles vs Market Timing

Market cycles classify conditions. Market timing tries to identify when a move should begin or end. Confusing the two creates one of the main risks in cycle analysis.

A cycle label can describe a market that appears to be expanding, contracting, distributing, or stabilizing. It cannot prove the exact moment when a top or bottom will form. Even a well-supported interpretation can fail if the market rejects the expected behavior, returns to a prior range, or shows stronger evidence in the opposite direction.

The safer use is diagnostic: identify the current behavior state, check whether the evidence agrees, and avoid treating the phase label as a trade instruction. A market-cycle framework is a map of changing conditions, not a timing engine.

Why Market Cycle Readings Can Fail

Cycle readings often fail because the market is less orderly in real time than it appears on a completed chart. A finished chart can make each phase look clean. During the actual transition, price may move back and forth between ranges, participation may narrow, and volatility may change before the market chooses a clearer direction.

Common mistake: Treating market cycles as fixed calendar sequences can create false precision. Cycle readings depend on market behavior, timeframe, liquidity, volatility, and participation. They are not made stronger by forcing every market into the same phase order.

| Failure condition | Why it matters | Safer reading |

|---|---|---|

| One timeframe dominates the interpretation | The cycle may look clear only because the observation window is too narrow. | Check whether the same behavior appears on the relevant timeframe for the question being studied. |

| Participation does not confirm the move | A price move with narrow participation may fade or remain unstable. | Treat the phase label as provisional until broader behavior confirms it. |

| Volatility expands without acceptance | A sharp move can look like a new phase but still return to the prior range. | Separate the volatility event from the cycle shift. |

| Related markets contradict the interpretation | Different markets can reveal pressure or support that the main chart does not show clearly. | Keep the interpretation conditional when cross-market behavior is mixed. |

| The phase label becomes retrospective | Completed charts make transitions look easier than they were in real time. | Use the label as a working interpretation, not a conclusion. |

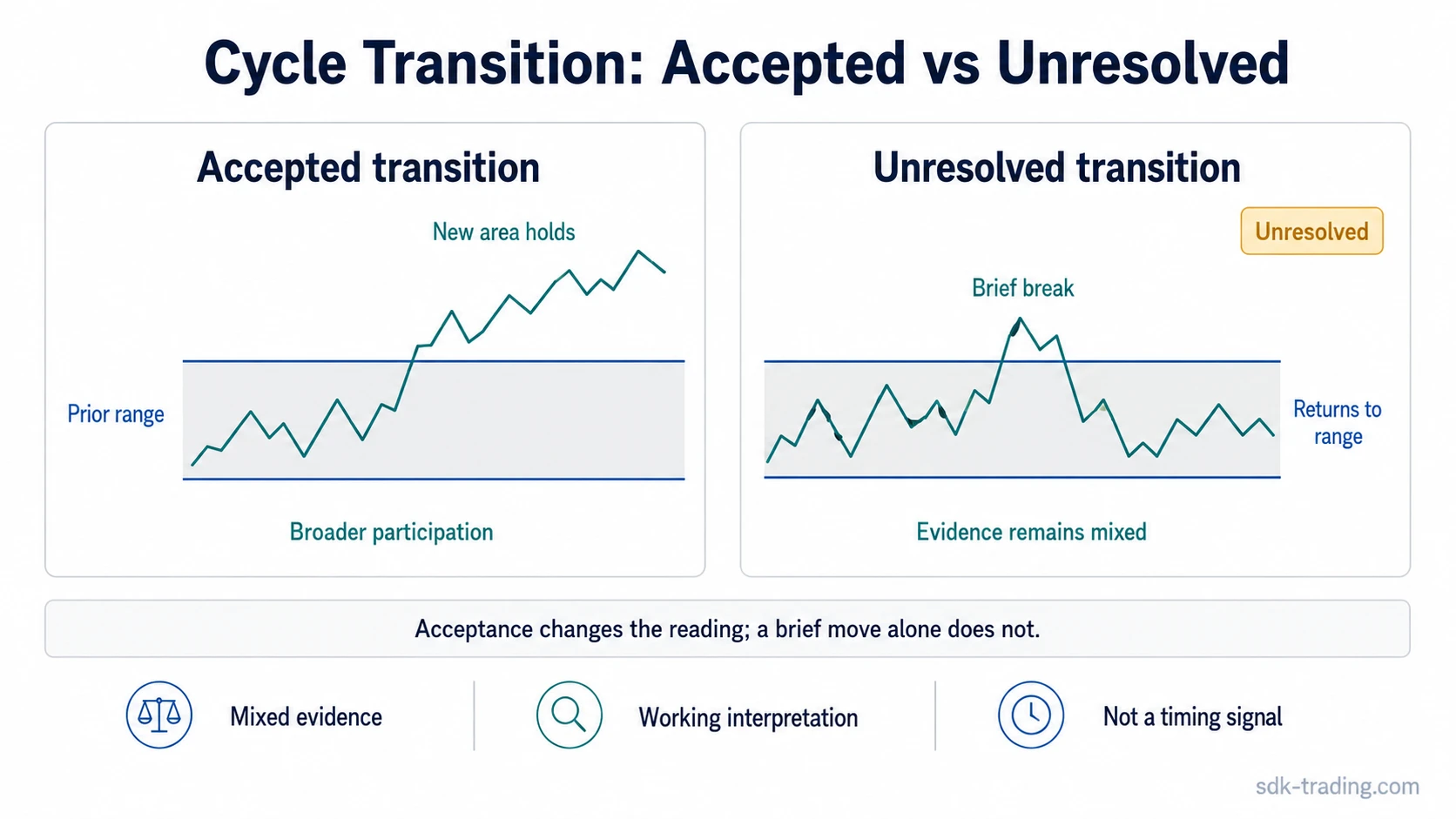

Practical Market Cycle Scenario

Price trades in a broad range after a decline. Volatility contracts, and each selloff becomes less effective, which can make the range look like early stabilization. The interpretation becomes more defensible only if price begins leaving the range with broader participation and holds above the prior area instead of immediately falling back into it.

The same behavior remains unresolved if price briefly breaks higher, volatility expands, and then price quickly returns to the middle of the range. In that case, the move may have been a failed transition rather than a confirmed expansion phase.

The first move is only a proposed transition. The stronger evidence comes from whether price holds the new area, participation broadens, and the prior range stops acting as the main reference point.

Business Cycle vs Market Cycle

A business cycle describes changes in economic activity, such as expansion, slowdown, recession, and recovery. A market cycle describes changes in financial-market behavior. The two can influence each other, but they are not the same lens.

Financial markets can move before, during, or after changes in economic data. A market can also price liquidity, policy expectations, earnings expectations, positioning, or risk appetite before the broader economic backdrop looks obvious. That is why market-cycle analysis should remain focused on market behavior rather than becoming a full economic forecast.

Using Market Cycles as a Classification Framework

The safest use of market cycles is classification. The framework can help separate an improving environment from a weakening one, or a trending phase from an unresolved transition. It should not be used as a standalone reason to act.

A stronger interpretation usually has several aligned features: price behavior supports the phase label, participation is consistent with the interpretation, volatility is not contradicting the move, and related markets do not create obvious conflict. A weaker interpretation appears when only one feature supports the label while the rest of the evidence remains mixed.

Market cycles become more useful when they reduce confusion rather than increase certainty. The main job is to describe the current environment clearly enough to avoid forcing a strategy, a forecast, or a timing claim onto incomplete evidence.

FAQ

Are market cycles the same as market timing?

No. Market cycles classify changing market conditions, while market timing tries to identify when a move should begin or end. A cycle label should not be treated as an exact timing signal.

Do market cycles always follow the same phases?

No. Markets can overlap phases, skip clean transitions, revisit prior ranges, or show different states across different timeframes. Phase labels are descriptive, not mandatory steps.

Why can a market cycle reading fail?

A reading can fail when price behavior reverses, participation does not confirm the move, volatility changes abruptly, the timeframe is unclear, or related markets contradict the interpretation.