Market prices move when buying or selling pressure is large enough relative to the liquidity available at the current price. A move can reflect new orders, changing expectations, thinner liquidity, or a catalyst that forces repricing, but price movement alone is not a forecast or a trading signal.

In trading, the question is not only whether price moved, but what made the current price area unable to absorb pressure without adjusting. That condition may come from aggressive orders, a thin order book, a surprise catalyst, shifting sentiment, or participants reacting around a widely watched reference area.

Definition: Market price movement is the visible result of repricing when buyers and sellers no longer agree at the previous price under the available liquidity, information, and participation conditions.

Key Points

- Price moves when buying or selling pressure exceeds available liquidity at the current price.

- Catalysts matter when they change expectations or trigger new order flow.

- Short-term and longer-term price drivers can be different even when the chart shows one price move.

- Movement is evidence of repricing, not proof that the move will continue or reverse.

What Moves Market Prices?

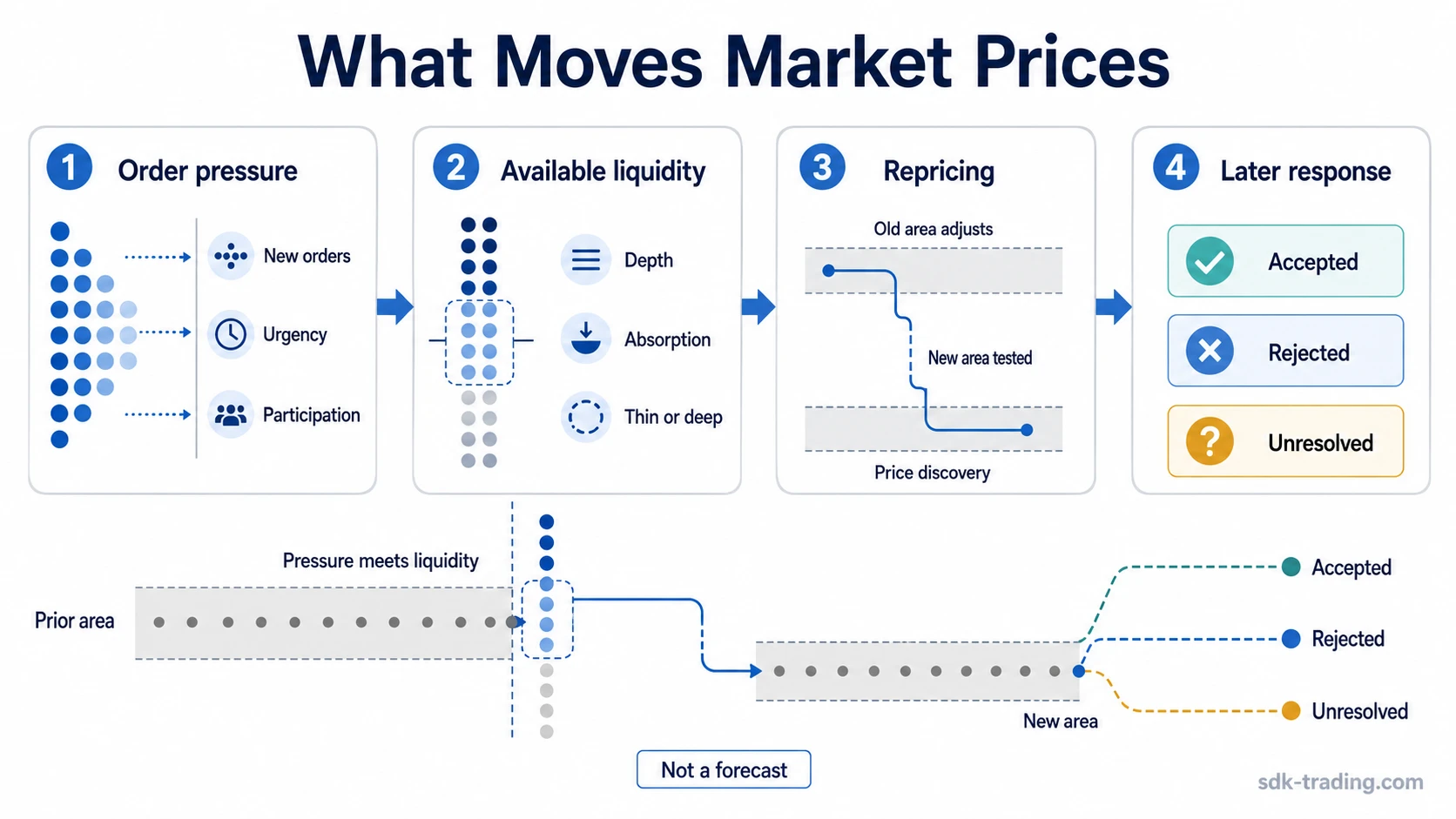

Market prices move because participants submit, remove, or adjust orders at prices where available liquidity is not enough to keep the previous price stable. When buyers are willing to lift available offers faster than sellers replenish them, price can rise. When sellers are willing to hit available bids faster than buyers replenish them, price can fall.

Supply and demand are the broad explanation, but the trading mechanism is more specific. Price changes when pressure meets the actual depth available at current prices. A market can move sharply on modest activity if liquidity is thin, or barely move on heavy volume if liquidity is deep enough to absorb the pressure.

The Core Mechanism: Orders, Liquidity, and Repricing

Every trade needs a buyer and a seller, but not every buyer or seller agrees at the same price. The bid is where buyers are currently willing to transact, and the ask is where sellers are currently willing to transact. When new orders consume the liquidity available near the current bid or ask, price has to move to the next area where another willing participant exists.

Order flow describes the pressure created by incoming buy and sell orders. Liquidity describes how much size can be absorbed without a large price change. Price discovery is the adjustment process that tests where enough buyers and sellers are willing to transact after information, positioning, or urgency changes.

Important distinction: Volume shows participation, but liquidity shows how much pressure the market can absorb. A high-volume move can still fail if later participation does not accept the new price area.

Main Conditions That Can Move Price

Different conditions can create the same visible result: a price move. The interpretation changes when the driver is order pressure, thinner liquidity, expectation change, sentiment, or a reaction around a technical reference area.

| Condition | What it may imply | Common misread | Safer reading |

|---|---|---|---|

| Order-flow imbalance | Buyers or sellers are acting with more urgency at the current price. | The move proves direction. | The move shows pressure now; later acceptance is still needed. |

| Thin liquidity | Less available depth can make price more sensitive to new orders. | A large move always means strong conviction. | The move may reflect poor depth as much as strong demand or supply. |

| News or catalyst | New information can force participants to reprice quickly. | All news should move price in the expected direction. | The reaction depends on surprise, positioning, and what was already expected. |

| Expectation change | Participants may adjust value assumptions, risk tolerance, or timing. | Known information should create a fresh move. | Price often reacts more to changed expectations than to information already priced in. |

| Macro, rates, or policy pressure | Discount rates, funding conditions, and risk appetite can alter participation. | One macro input explains every move. | Macro inputs matter most when they change positioning, liquidity, or expected returns. |

| Sentiment and positioning | Crowded positioning can make price more sensitive to surprise or forced adjustment. | Sentiment alone is enough to forecast price. | Sentiment is more useful when paired with price response, liquidity, and follow-through. |

| Technical reference area | Participants may react near prior highs, lows, ranges, or widely watched levels. | The level itself causes the move. | The level matters because participant behavior can concentrate around it. |

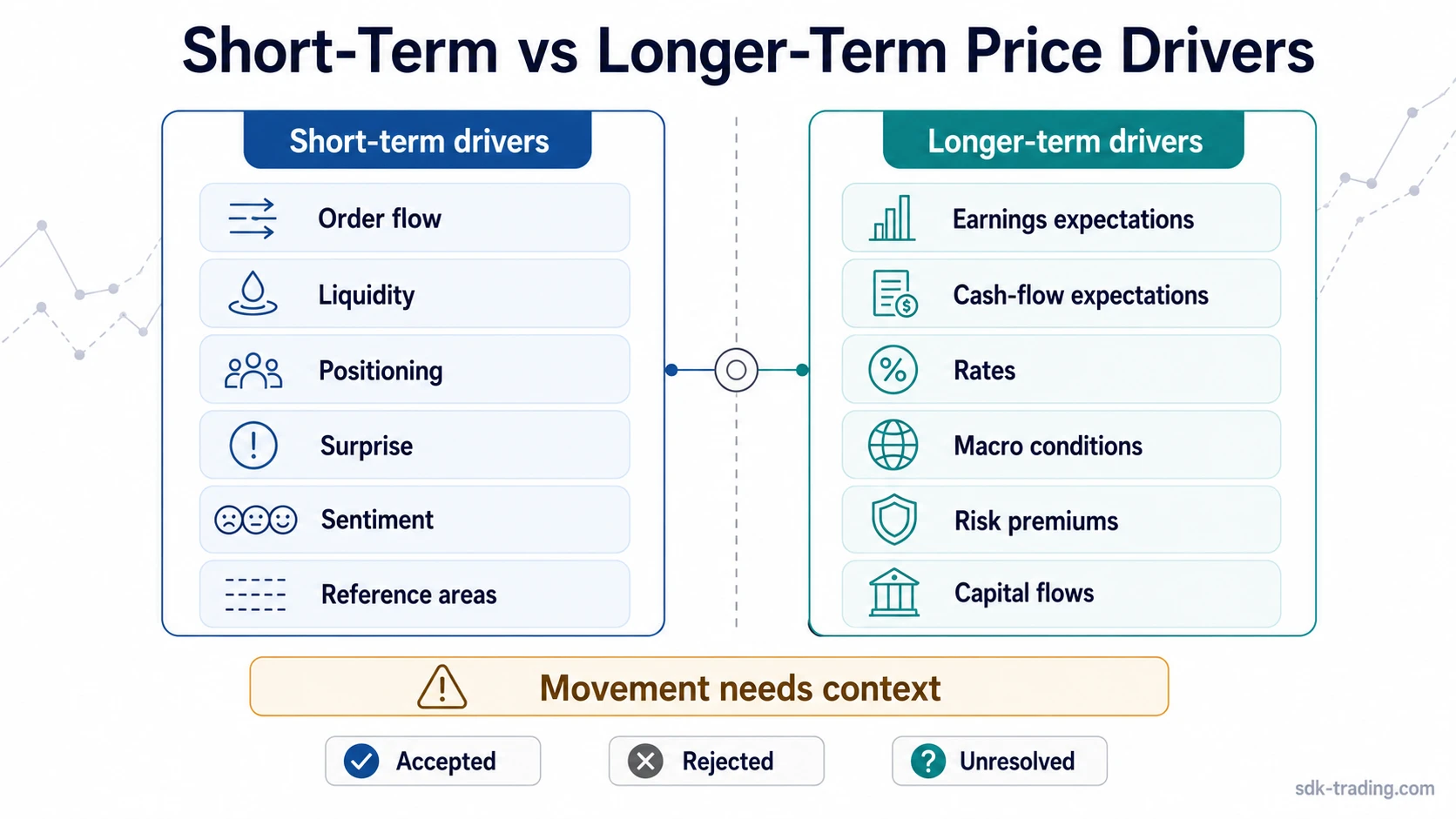

Short-Term vs Longer-Term Price Drivers

Short-term price movement is often dominated by order flow, liquidity, positioning, surprise, and sentiment. These drivers can create fast movement even when the longer-term story has not changed much.

Longer-term price movement tends to depend more on changing expectations about earnings, cash flows, rates, inflation, risk premiums, capital flows, and broader market conditions. That does not make longer-term moves deterministic. It means the market may need more durable evidence before a repricing becomes accepted beyond the initial reaction.

| Time horizon | Drivers that often matter more | Interpretation limit |

|---|---|---|

| Short-term | Order flow, liquidity, positioning, surprise, sentiment, technical reference areas. | Fast movement can fade if the new price area is not accepted. |

| Longer-term | Earnings expectations, cash-flow expectations, rates, macro conditions, risk premiums, capital flows. | Fundamental or macro logic can take time to appear in price and can be offset by other forces. |

Why Price Movement Is Not the Same as Prediction

A price move confirms that repricing happened. It does not confirm why every participant acted, and it does not prove what will happen next. The same upward move can come from durable demand, short covering, thin liquidity, or a temporary reaction to news. The same downward move can come from fresh supply, forced selling, risk reduction, or a failed attempt to hold a higher area.

Limitation: Price movement is evidence, not a complete conclusion. The interpretation becomes more useful only after pressure, liquidity, expectation change, and later acceptance or rejection are separated.

Common mistake: Treating movement as a signal by itself. A sharp move can look meaningful, but without context it may only show that the previous price area could not absorb pressure at that moment.

Simple Market Price Movement Example

A common scenario is that unexpected news reaches a market when available liquidity is thin. Buyers or sellers respond quickly, and price moves through several nearby price areas because there is not enough resting liquidity to absorb the pressure. The first move shows repricing, but the later test matters: if trading continues to hold in the new area, the repricing is being accepted for now; if price quickly returns to the prior area, the first move may have reflected urgency or thin liquidity more than durable agreement.

The diagnostic point is the sequence. First comes pressure. Then comes repricing. After that, the market either accepts the new area, rejects it, or stays unresolved. That sequence keeps the first move in context instead of treating it as the full explanation.

How Individual Price Moves Relate to Market Cycles

Individual moves can later become part of a broader market-cycle reading when repeated repricing, participation changes, and acceptance or rejection around key areas start to form a wider structure. A single move does not define the cycle by itself.

Cycle interpretation needs repeated evidence. One repricing event may show pressure. A series of accepted repricing events can suggest a broader shift in control, participation, or risk appetite. A failed repricing attempt can instead show that the market tested a new area but did not accept it.

FAQ

What is the main reason market prices move?

Market prices move when buying or selling pressure is large enough relative to available liquidity at the current price. Supply and demand matter, but the immediate mechanism is pressure meeting the depth available in the market.

Does news always move market prices?

News can move market prices when it changes expectations, order flow, or positioning. If the information was already expected, or if liquidity absorbs the reaction, the price response may be limited.

Is volume enough to explain a price move?

Volume shows participation, but it does not prove follow-through by itself. A move also depends on available liquidity, the quality of participation, and whether the new price area is later accepted or rejected.

Do technical levels cause price to move?

Technical reference areas do not cause movement by themselves. They can matter because many participants may react around prior highs, lows, ranges, or other visible areas, which can concentrate order flow.

Can price movement predict the next move?

Price movement shows that repricing has occurred, but it does not predict the next move on its own. The interpretation needs context, liquidity, expectations, and later market acceptance or rejection.