Types of financial markets in trading are categories based on what is being traded, how the instrument is structured, and where transactions take place. Equity, debt, currency, commodity, derivative, and money markets all produce prices, but each one reflects a different claim, contract, venue, and liquidity profile.

Definition: Types of financial markets are structural categories that group markets by traded instrument, economic function, and trading venue. The category changes the background for reading price movement, but it does not create a trade signal or predict direction.

A stock chart, a currency pair, a futures contract, and an options contract can all show rising or falling prices. The traded instrument is different in each case. A share represents ownership, a currency pair expresses relative monetary value, a futures contract gives standardized exposure to an underlying market, and an option depends on contract terms such as expiry, strike, and volatility sensitivity.

Key Points

- Financial markets can be grouped by the instrument, claim, or contract being traded.

- The main categories include equity, debt, currency, commodity, derivatives, and money markets.

- Primary markets create new instruments, while secondary markets trade instruments that already exist.

- Exchange-traded and OTC markets differ in standardization, quote visibility, and counterparty structure.

- Market type affects the classification check behind price movement, not trade direction or outcome.

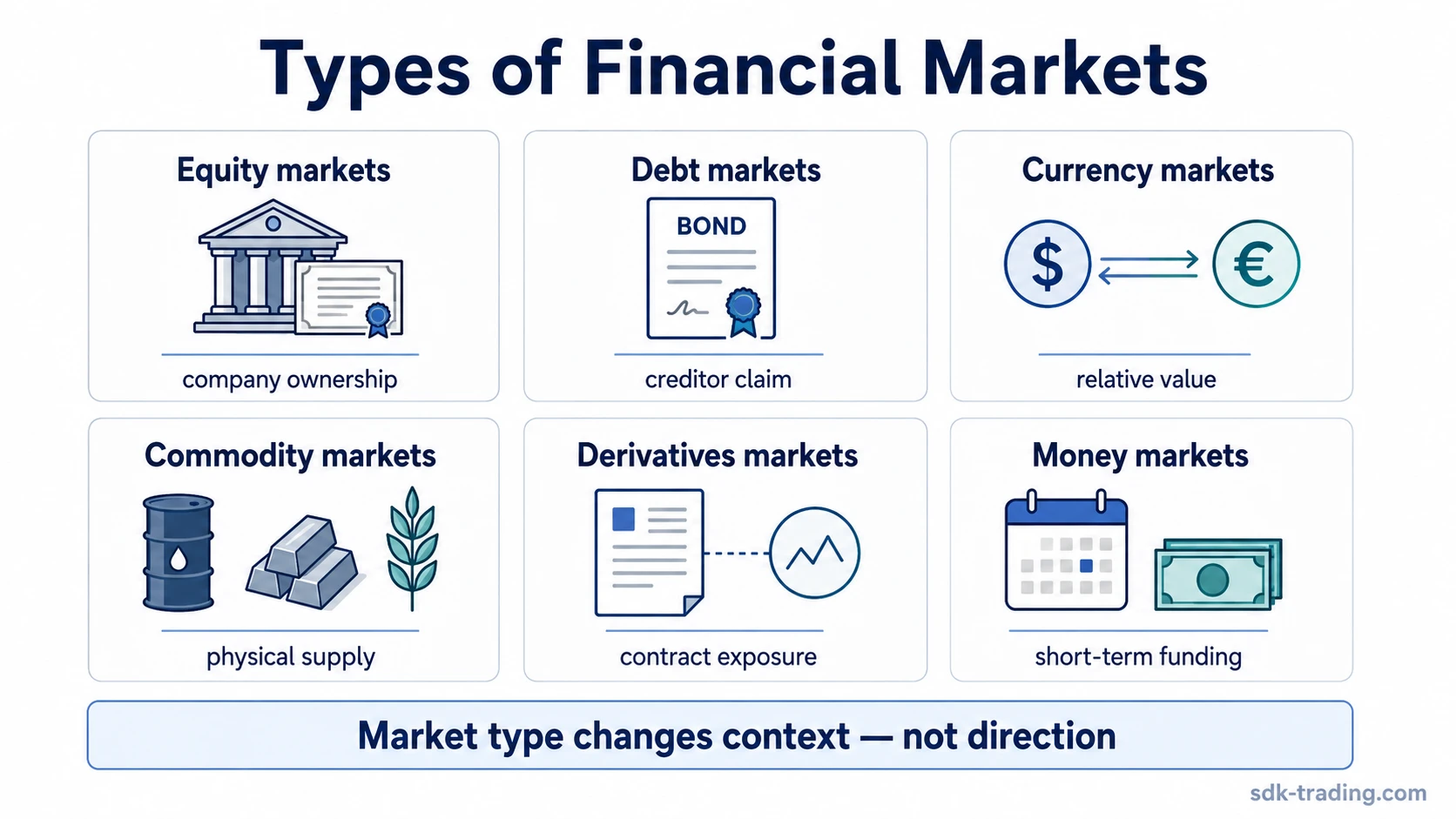

Main Types of Financial Markets

The main types of financial markets separate ownership claims, creditor claims, relative currency values, physical-goods exposure, contract-based exposure, and short-term funding instruments. The useful distinction is not only what appears on the chart, but what the chart represents.

| Market type | What is traded | Structural feature | Trading-context implication |

|---|---|---|---|

| Equity markets | Shares of companies | Ownership claim on corporate assets and earnings | Price movement can reflect company-specific information, sector conditions, broad risk appetite, and market-cycle pressure. |

| Debt markets | Bonds and other credit instruments | Contractual creditor claim with interest and principal terms | Rate sensitivity, duration, credit risk, and issuer quality can matter as much as the price pattern itself. |

| Currency markets | Currency pairs | Relative value between two monetary units | Every quote compares one currency against another, so both sides of the pair affect the reading. |

| Commodity markets | Energy, metals, agricultural products, and related contracts | Exposure linked to physical supply, storage, production, and demand | Seasonality, inventories, contract design, and supply shocks can change the meaning of a price move. |

| Derivatives markets | Contracts based on an underlying asset, rate, index, currency, commodity, or benchmark | Value derived from another reference market | Expiry, margin, leverage, volatility, and payoff structure can affect the reading beyond the underlying chart. |

| Money markets | Short-term funding instruments | Short maturity and liquidity-management function | Pricing is often tied to funding conditions, policy rates, and short-term liquidity rather than long-term ownership value. |

How the Main Market Types Differ

Equity markets organize trading in company shares. Because a share is an ownership claim, equity prices can respond to earnings expectations, sector rotation, balance-sheet concerns, corporate news, and broad changes in risk appetite.

Debt markets organize trading in instruments such as government bonds, corporate bonds, and other credit claims. These instruments are built around borrowed capital, interest payments, maturity, and repayment terms, so rates, duration, inflation expectations, and credit spreads can strongly influence price movement.

Currency markets trade relative monetary value. A forex quote normally appears as a pair, so the price reflects one currency measured against another rather than a single asset priced in isolation.

Commodity markets are tied to physical goods such as energy products, metals, and agricultural inputs. Trading may occur through spot markets, futures contracts, or other standardized structures, but the underlying exposure remains connected to production, storage, inventories, transportation, and consumption demand.

Derivatives are contracts whose value depends on an underlying asset, index, rate, commodity, currency, or benchmark. Futures, options, swaps, and many structured contracts belong to this category. A derivative does not always represent direct ownership of the underlying market, so contract design matters.

Limitation: A derivative chart can resemble the chart of its underlying market while still carrying different risk and contract behavior. The visible price path is only one part of the instrument design.

Money markets handle short-term funding and liquidity instruments. Treasury bills, commercial paper, repurchase agreements, and similar short-maturity instruments are usually linked to cash management, funding conditions, and short-term rates. Changes in money-market conditions can also influence broader market cycles when funding pressure or liquidity changes spread into risk assets.

Primary and Secondary Markets

Primary markets are where financial instruments are issued for the first time. A company selling new shares or a government issuing new bonds is using the primary market because capital moves from investors to the issuer.

Secondary markets are where already issued instruments trade between participants. Most day-to-day chart activity in stocks, bonds, ETFs, futures, and many other instruments belongs to this secondary layer. Ownership changes hands, but the instrument itself was already created earlier.

| Market layer | Main function | Trading relevance |

|---|---|---|

| Primary market | Creates or issues a new instrument | Important for issuance events, offerings, and capital raising. |

| Secondary market | Allows existing instruments to trade | Most chart-based trading activity takes place here. |

Exchange-Traded and OTC Markets

Financial markets can also be classified by venue model. Exchange-traded markets use centralized venues with standardized rules, published quotes, and defined listing or contract requirements.

Over-the-counter markets operate through dealer networks or bilateral negotiation rather than a single centralized exchange. OTC structure can affect quote visibility, counterparty relationships, liquidity fragmentation, and how easily a market price can be compared across participants.

Exchange-traded markets usually provide more standardized trading rules and clearer public quote structure. OTC markets can offer flexibility, but price visibility and liquidity may depend more on dealer networks and counterparty access.

How Market Type Changes Trading Context

Market type changes the background conditions behind a chart. The same visual move can carry a different meaning depending on whether the instrument is a share, bond, currency pair, commodity contract, derivative, or short-term funding instrument.

| Classification check | Why it changes the reading |

|---|---|

| Liquidity | Thin liquidity can make price movement sharper, less continuous, or more sensitive to order flow. |

| Trading hours | Session structure can affect gaps, volatility windows, and how price reacts to new information. |

| Contract terms | Expiry, margin, settlement, and leverage can affect behavior even when the underlying market looks similar. |

| Pricing drivers | Company earnings, interest rates, policy changes, inventories, and funding stress affect different market types in different ways. |

| Venue model | Centralized exchange trading and OTC negotiation can produce different levels of transparency and quote consistency. |

Common Mistakes When Comparing Market Types

A common mistake is treating every market chart as if it represents the same kind of instrument. A rising line in an equity market, a bond market, a currency pair, and a futures contract may look similar, but the underlying claim and market design can be very different.

Common mistake: market category is not a trading signal. It helps define the instrument behind price activity. Directional analysis still depends on actual market behavior, liquidity, conditions, and risk.

Another mistake is confusing a market type with a trading style. Equity, forex, commodity, and derivatives markets describe what is traded. Day trading, swing trading, scalping, and position trading describe holding-period and execution style. The two classifications can overlap, but they are not the same idea.

Note: Some instruments combine categories. Convertible bonds, commodity-linked notes, and some digital or tokenized instruments can mix features from more than one market type. Classification should start with the instrument’s claim, venue, liquidity, and contract terms.

Simple Market Type Example

A strong upward price move can look similar across a stock, a currency pair, a crude oil futures contract, and an options contract. The classification check changes what should be examined next.

For the stock, company news, sector behavior, and broad equity conditions may matter. For the currency pair, both currencies in the quote have to be compared. For the futures contract, expiry, inventories, and supply conditions can affect the move. For the options contract, the underlying asset is only part of the picture because volatility, time decay, strike selection, and expiry also shape the contract price.

The market type does not decide direction. It defines the background questions that make the price move easier to interpret.

FAQ

What are the main types of financial markets?

The main types of financial markets include equity markets, debt or bond markets, currency markets, commodity markets, derivatives markets, and money markets. Markets can also be grouped by structure, such as primary versus secondary markets or exchange-traded versus OTC markets.

What is the difference between primary and secondary markets?

Primary markets create new financial instruments through issuance. Secondary markets allow already issued instruments to trade between participants. Most chart-based trading activity happens in secondary markets.

What is the difference between exchange-traded and OTC markets?

Exchange-traded markets use centralized venues with standardized rules and clearer public quote structures. OTC markets rely more on dealer networks or bilateral negotiation, so quote visibility, liquidity, and counterparty access can differ.

Is a market type the same as a trading style?

No. A market type describes what is traded and how the market is structured. A trading style describes how long a trader usually holds positions and how decisions are organized.

Does a market type create a trading signal?

No. A market type defines the structure behind the instrument and venue. It can change how price movement is interpreted, but it does not predict direction or create an entry, exit, target, or outcome.