ATR in risk management helps measure how wide normal price movement has become, so exposure, distance, and loss-boundary assumptions are not built on a fixed number that ignores volatility.

ATR is a volatility and range scale. It can show that the market is moving more or less than usual, but it does not confirm direction, trade quality, reversal, continuation, or profit potential. The reading becomes more useful when ATR is compared with planned exposure, a defined risk boundary, market structure, and directional evidence from outside ATR.

ATR measures average true range over a selected period. In risk management, the narrower question is whether current movement is small enough, wide enough, or unstable enough to change the assumptions behind planned exposure.

Key Points

- ATR measures movement range, not market direction.

- Higher ATR means wider normal fluctuation, not automatically better opportunity.

- Risk assumptions need planned exposure, a defined boundary, and structure, not ATR alone.

- Static distance assumptions can fail when volatility expands or contracts sharply.

What ATR Can and Cannot Prove in Risk Management

ATR can support a risk-management decision by showing whether recent movement has expanded, compressed, or become unstable. That matters because a distance that looks wide in a quiet market may be ordinary in a high-range market, while a distance that looks acceptable on one timeframe may be too narrow after volatility expands.

ATR cannot decide whether the market should move up or down. It also cannot establish that planned exposure is appropriate, that a loss boundary is logical, or that a chart structure is valid. Those judgments need separate evidence.

| ATR evidence | What it can support | What it cannot prove | What else must be checked |

|---|---|---|---|

| ATR is expanding | Recent movement is widening, so normal fluctuation may be larger than before. | That the move has better direction, better quality, or better profit potential. | Planned exposure, structure, directional evidence, and whether the risk boundary is still meaningful. |

| ATR is compressed | Recent movement is narrow, so a fixed distance may look larger relative to recent range. | That the market is safe, stable, or unlikely to break range. | Breakout risk, liquidity conditions, range boundaries, and whether price is accepting or rejecting key areas. |

| ATR spikes suddenly | The market may be reacting to a volatility shock or temporary range expansion. | That the new range will persist or that direction is confirmed. | Follow-through, acceptance, volume behavior, and whether structure changes after the spike. |

| ATR differs across timeframes | The risk scale may change depending on the chart timeframe and ATR period selected. | That one ATR setting is universally correct. | Whether the chosen period matches the decision horizon being analyzed. |

How ATR Changes Risk Assumptions

ATR is based on true range, which accounts for the largest of three range measures: the current high minus low, the distance from the current high to the previous close, or the distance from the current low to the previous close. This makes ATR sensitive to gaps and large range changes, not only intraday candle size.

The selected ATR period smooths those true range values. A shorter period can react faster to recent volatility shifts, while a longer period may smooth temporary changes. The chart timeframe is separate from the ATR period: a 14-period ATR on a daily chart does not describe the same movement scale as a 14-period ATR on an hourly chart.

Risk-management use: ATR can make distance assumptions more range-aware. It cannot replace a defined risk boundary, exposure control, or structural reason for the market idea.

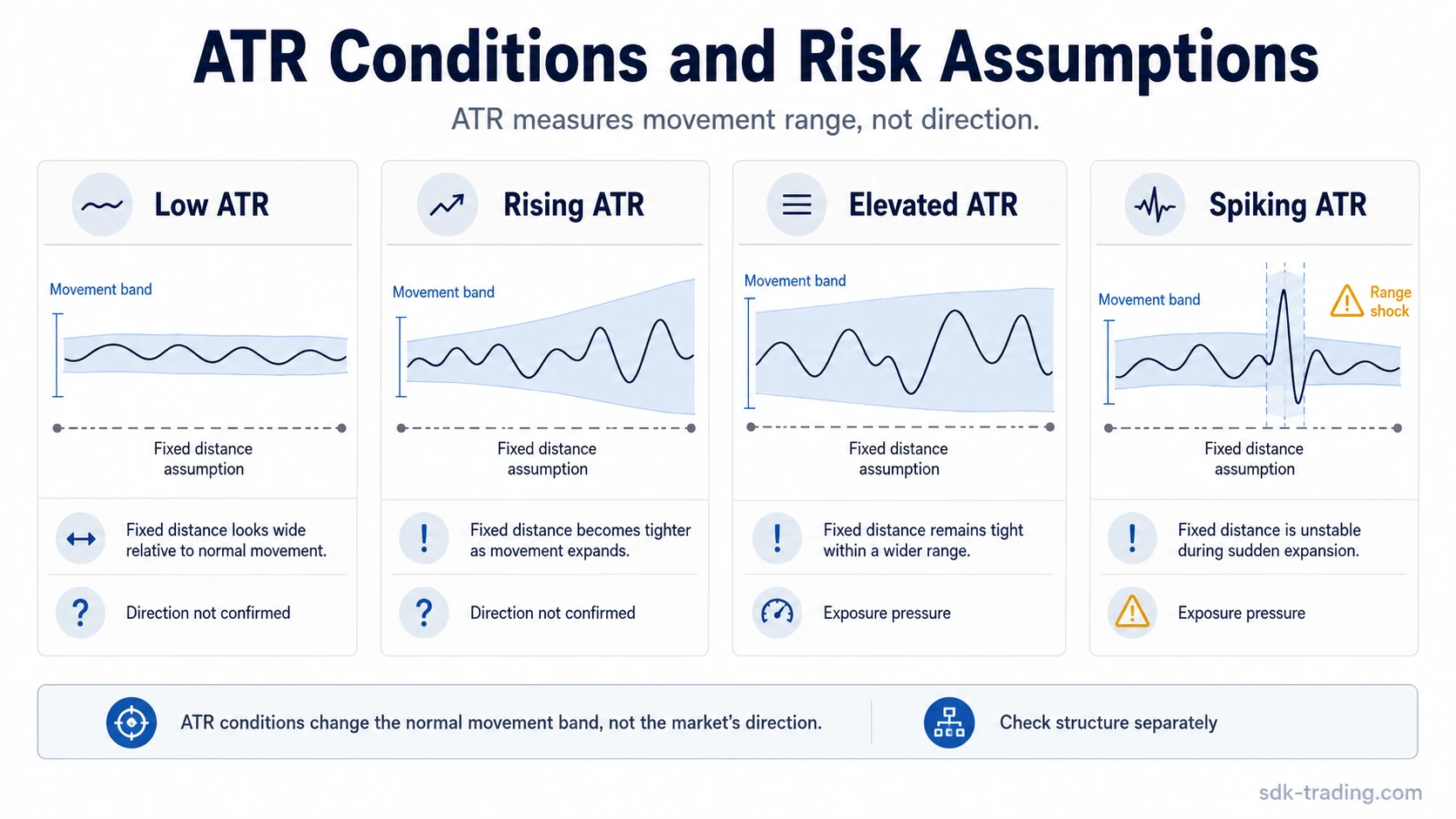

ATR Conditions: Low, Rising, Elevated, and Spiking

ATR becomes more useful when the reading is interpreted as a condition, not as a command. A low, rising, elevated, or spiking ATR reading can change the risk environment, but each condition still needs separate evidence before it affects a final risk decision.

| ATR condition | What it can suggest | What it cannot prove | Risk-management question |

|---|---|---|---|

| Low ATR | Recent price movement is compressed compared with the selected lookback period. | That the market is safer or that volatility cannot expand. | Would a sudden range expansion make the planned exposure too large? |

| Rising ATR | Range is expanding and normal fluctuation may be increasing. | That the direction of the move is reliable. | Does the position still make sense if ordinary fluctuation becomes wider? |

| Elevated ATR | The market is already moving in a wider range environment. | That the opportunity is better or more profitable. | Is exposure adjusted to the wider movement band? |

| Spiking ATR | A volatility shock, gap, or large range event may have distorted recent movement. | That the spike is permanent or directionally meaningful. | Is the reading still useful after the shock is separated from normal behavior? |

Common Misread: Wider ATR Does Not Mean Better Opportunity

A wider ATR reading can be tempting because larger movement creates the appearance of more room. The safer interpretation is different: wider movement also means adverse movement may be larger, ordinary pullbacks may travel farther, and a fixed distance assumption may stop describing the real movement band.

Common mistake: treating a higher ATR as stronger evidence for a market idea. Higher ATR only shows that the market has been moving more. Directional quality, acceptance, rejection, and structure must come from other evidence.

ATR risk-management example: Price begins rotating in a wider range after volatility expands. The old fixed distance is now crossed repeatedly during ordinary movement, even though the broader structure has not clearly changed. The issue is not that ATR proves the idea wrong; the issue is that the distance assumption was built for a quieter range. A stronger risk reading compares the new ATR condition with exposure, structure, and a clearly defined loss boundary. A weaker reading treats the old static distance as valid after the movement band has changed.

What ATR Is Enough to Show – and What It Is Not Enough to Show

ATR is enough to show that the movement scale has changed. It is not enough to show that a market idea has become more valid. This distinction prevents volatility from being mistaken for proof.

| Question | ATR can help answer | ATR cannot answer alone |

|---|---|---|

| How wide is recent movement? | Yes. ATR is designed to measure average true range over the chosen period. | It cannot explain why the movement is happening. |

| Is exposure too large for the current range? | Partly. ATR can reveal that ordinary movement has widened. | It cannot decide the correct position size without account risk, loss boundary, and instrument specifics. |

| Is the loss boundary meaningful? | Partly. ATR can show whether the boundary is inside or outside recent fluctuation. | It cannot establish that the boundary matches structure or acceptance logic. |

| Is the market direction confirmed? | No. ATR is direction-neutral. | Directional evidence must come from trend, structure, price behavior, or another defined method. |

ATR Risk Management vs ATR Trailing Stop

ATR risk management uses volatility to judge whether exposure and distance assumptions fit the current range environment. An ATR trailing stop uses ATR as part of a moving stop framework. Those ideas overlap, but they are not the same.

The risk-management use is broader and less tactical: ATR helps describe movement scale before any rule is chosen. A trailing-stop method adds a specific mechanism for moving a boundary as price changes. Confusing the two can turn a volatility reading into a mechanical instruction that ATR alone does not justify.

Where Bollinger Bands Fit Differently

ATR measures average true range as an absolute movement scale. Bollinger Bands frame volatility around a moving average using bands that expand and contract with price dispersion. Both can describe changing volatility, but they answer different questions.

ATR is often cleaner for thinking about distance, fluctuation, and exposure pressure. Bollinger Bands are more visual for judging how price behaves relative to an envelope. Neither tool turns volatility into a direction forecast by itself.

Limitations of ATR in Risk Management

ATR is historical and descriptive. It reflects what recent ranges have done, not what the next move must do. A volatility spike can lift ATR temporarily, a quiet period can compress it before expansion, and a poor period choice can make the reading too fast or too slow for the decision being made.

The main limitation is proof. ATR can improve the measurement of movement scale, but the risk case still needs a defined boundary, exposure logic, and structure. Without those pieces, ATR only says that movement has been wide, narrow, rising, or unstable.

FAQ

How is ATR used in risk management?

ATR is used to understand recent movement range so distance and exposure assumptions are not based on a fixed number that ignores volatility. It does not decide direction or trade quality.

Does high ATR mean higher risk?

High ATR can mean ordinary price movement is wider, which may increase exposure pressure if position size and loss boundaries are not adjusted to the volatility environment. It does not automatically mean the market is worse or better.

Can ATR predict market direction?

No. ATR is direction-neutral. It measures range, not whether price is more likely to move up or down.

What is the difference between ATR period and chart timeframe?

The chart timeframe defines the candles being measured, while the ATR period defines how many of those candles are averaged. A 14-period ATR on a daily chart describes a different range scale than a 14-period ATR on an hourly chart.