VWAP means volume-weighted average price. It is a price benchmark that weights each traded price by volume, so higher-volume trading has more influence on the line than lower-volume trading.

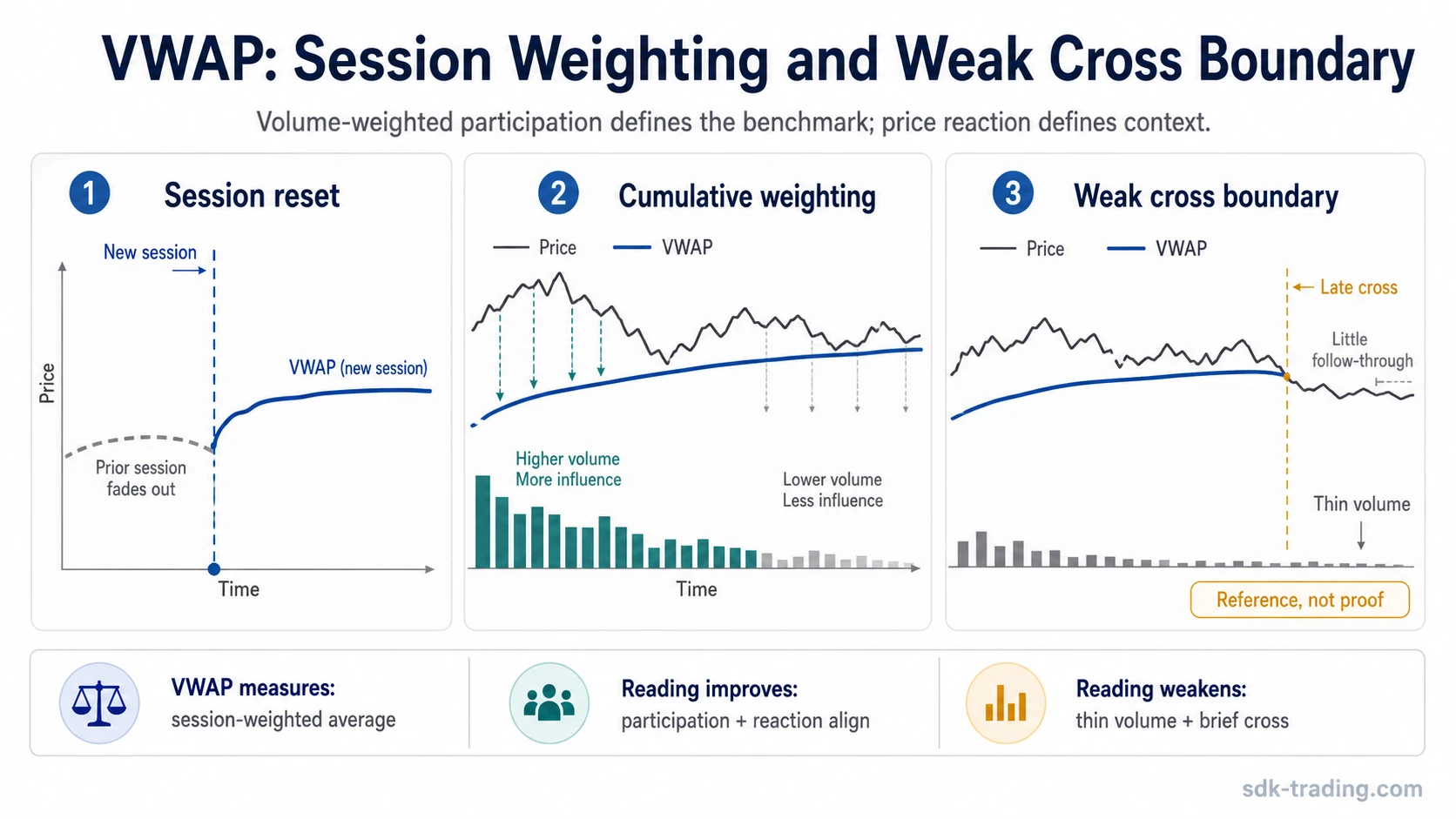

In most charting use, VWAP is calculated intraday and starts fresh at the beginning of each session. That session boundary matters because the line reflects cumulative price-volume activity from the current session, not a permanent average across all prior trading.

VWAP is useful as a reference for where meaningful volume-weighted participation has occurred. By itself, VWAP does not prove direction, reversal timing, trade quality, or confirmed support and resistance behavior.

Core VWAP Reading Points

- VWAP weights price by traded volume, not by time alone.

- Standard VWAP usually resets at the start of each trading session.

- A VWAP line can lag later in the session because earlier high-volume trading remains in the calculation.

- A clean VWAP reading needs participation and price behavior that support the same interpretation.

- A weak VWAP reading can appear when price crosses the line on thin volume or with little follow-through.

What Is VWAP?

VWAP is the average price of a security weighted by volume over a chosen calculation window, most often the current trading session. Instead of treating each price point equally, VWAP gives more weight to prices where more volume traded.

This makes VWAP different from a simple average of price. If a large amount of volume trades near one area, that area can pull the VWAP line toward it more strongly than a brief price move with little participation.

Because of that weighting, VWAP is often used as a benchmark. It can help compare current price behavior with the session’s volume-weighted participation, but the comparison still needs context from volume, price reaction, and the broader chart structure.

VWAP Formula and Calculation

The basic VWAP calculation divides cumulative price-volume value by cumulative volume. Many charting platforms use typical price for each bar, although the exact input can vary by data source and platform.

VWAP = cumulative (price input x volume) / cumulative volume

A common bar-based version uses typical price:

Typical price = (high + low + close) / 3

VWAP = cumulative (typical price x volume) / cumulative volume

The important mechanism is cumulative weighting. Each new bar adds more price-volume information to the numerator and more volume to the denominator. As the session develops, the line becomes harder to move unless new participation is large enough to influence the cumulative calculation.

| Calculation part | What it represents | Why it matters |

|---|---|---|

| Price input | The price used for each bar or trade | Defines the price level being weighted |

| Volume | The amount traded at that input | Controls how much influence that price has |

| Cumulative price x volume | The running total of weighted price activity | Builds the session’s weighted participation base |

| Cumulative volume | The running total of traded volume | Normalizes the weighted value into an average price |

Why VWAP Resets Each Session

Standard intraday VWAP usually begins again at the start of each trading session. The reset prevents older sessions from dominating the current session’s volume-weighted line.

Without a reset, the calculation would keep carrying previous price-volume activity forward. That can make the line less useful for reading the current session’s participation because older volume may overwhelm newer behavior.

The reset also explains why VWAP is often treated as an intraday benchmark. It describes the current session’s volume-weighted average, not the same type of long-term smoothing that a multi-day moving average provides.

VWAP as a Benchmark

VWAP can be used as a benchmark because it gives a reference for the average price paid or received across volume during a session. A price above or below VWAP may show where current price sits relative to that session’s weighted participation, but that relationship is only a starting point.

The stronger question is whether price behavior and participation agree with the session-weighted average. A move away from VWAP with expanding participation can carry different information than a brief cross with thin volume and no acceptance.

Institutional execution often uses VWAP as a benchmark for comparing execution quality against the session’s volume-weighted average. That benchmark use is different from treating the line as a complete trading system.

What VWAP Can and Cannot Tell You

VWAP can describe the session’s volume-weighted price reference. It cannot independently explain why participants acted, whether a move will continue, or whether a reaction around the line is meaningful enough to act on.

| VWAP can help show | VWAP does not prove |

|---|---|

| Where the session’s volume-weighted average price sits | Future direction |

| Whether current price is above or below that session reference | Trade quality |

| How high-volume areas influence the session average | Confirmed support or resistance |

| Whether late-session price changes are large enough to shift the cumulative line | Reversal timing |

| How a session-based benchmark differs from a price-only average | A complete strategy |

VWAP Diagnostic Boundary

A VWAP reading becomes more useful when the line is treated as a reference with conditions, not as a mechanical signal. The main boundary is whether price behavior and participation support the same interpretation.

| Diagnostic question | VWAP reading boundary |

|---|---|

| What does VWAP measure? | It measures a session-weighted average price based on traded volume. |

| What does VWAP not measure? | It does not measure future direction, trade quality, or confirmed support and resistance behavior. |

| What strengthens the reading? | Participation, price behavior, and acceptance or rejection around the line support the same interpretation. |

| What weakens the reading? | Thin volume, late-session lag, a brief cross, or a disconnected reaction can make the reading less meaningful. |

| What invalidates a simple reading? | The price reaction fails to match the participation context, or the calculation window is the wrong one for the question being asked. |

Clean, Weak, and Invalid VWAP Readings

The same VWAP position can mean different things depending on participation and price behavior. A clean reading has alignment between the volume-weighted line and the surrounding reaction. A weak reading lacks that support. An invalid reading comes from using the wrong context or treating the line as proof.

| Reading type | What it looks like | Interpretation boundary |

|---|---|---|

| Clean reading | Price behavior and participation support the same VWAP relationship. | The line is useful as part of the session context, not as a standalone decision. |

| Weak reading | Price crosses VWAP on thin volume or with little follow-through. | The cross needs more evidence before it becomes meaningful. |

| Invalid reading | The VWAP window does not match the question, or the line is treated as automatic support or resistance. | The interpretation should be reset around the correct calculation context and actual price behavior. |

VWAP vs Moving Average

VWAP and moving averages can both appear as lines on a chart, but they answer different questions. VWAP weights price by volume during the calculation window. Most moving averages smooth price over a chosen number of periods without giving higher-volume periods extra influence.

| Feature | VWAP | Moving average |

|---|---|---|

| Main input | Price and volume | Price |

| Typical window | Current session for standard intraday VWAP | Chosen number of bars, minutes, days, or periods |

| Main question | Where is the session’s volume-weighted average? | How is price smoothing over time? |

| Common mistake | Treating the line as an automatic signal | Treating smoothing as confirmation by itself |

VWAP vs Anchored VWAP

Standard VWAP usually starts from the beginning of the current session. Anchored VWAP starts from a selected event, swing point, date, or other chosen anchor.

The difference is the starting point. Session VWAP asks where price has traded on a volume-weighted basis during the current session. Anchored VWAP asks how price has behaved on a volume-weighted basis since the selected anchor.

Related Volume Concepts

VWAP sits inside the volume indicator family, but it should not be confused with every volume-based tool. Volume Profile maps volume by price level. OBV accumulates volume based on whether price closes higher or lower. VWAP produces a volume-weighted average line for the selected calculation window.

| Concept | Main focus | Boundary |

|---|---|---|

| VWAP | Volume-weighted average price over a window | It is a line, not a complete signal. |

| Anchored VWAP | Volume-weighted average from a chosen anchor | The anchor changes the calculation question. |

| Volume Profile | Volume distribution by price level | It maps participation zones, not a session average line. |

| OBV | Cumulative volume based on close direction | It is a close-direction volume line, not a price-weighted benchmark. |

Example of a Weak VWAP Reading

Late in a session, price may move back across VWAP after most of the day’s volume has already traded. The cross can look meaningful because the line is widely watched, but the cumulative calculation may barely move if the new volume is small compared with earlier participation.

The read becomes weaker when the cross happens on thin volume, price does not hold acceptance around the line, and the next reaction stalls quickly. In that case, the VWAP interaction is only a reference point. Stronger evidence would require participation and price behavior to support the same reading, rather than relying on the line cross alone.

Where VWAP Fits Among Day-Trading Indicators

VWAP is often used in intraday chart review because it connects price with traded volume inside the session. It works differently from oscillators, moving averages, and pure volume lines because it produces a session-based price benchmark rather than a momentum reading or a close-direction volume total.

That makes VWAP useful inside a broader set of technical indicators for day trading, but it still needs context. The line becomes more useful when it is compared with participation, acceptance, rejection, and the surrounding market structure.

VWAP Limitations

VWAP has several limitations. It is cumulative, so it can lag later in the session. It is session-dependent, so the chosen window matters. It is also sensitive to how the platform defines the price input and trading session.

| Limitation | Why it matters | Safer interpretation |

|---|---|---|

| Late-session lag | Earlier high-volume activity can dominate the calculation. | Check whether new participation is large enough to affect the line. |

| Thin-volume crosses | Price can cross the line without meaningful participation. | Look for acceptance, rejection, and follow-through before assigning weight to the cross. |

| Session dependency | VWAP changes when the calculation window changes. | Match the VWAP window to the question being asked. |

| Benchmark confusion | A benchmark can be mistaken for a complete signal. | Use VWAP as reference context, not proof of direction or trade quality. |

FAQ

What does VWAP stand for?

VWAP stands for volume-weighted average price. It is an average price weighted by traded volume during the calculation window, most often the current trading session.

Is VWAP the same as a moving average?

No. VWAP weights price by volume, while most moving averages smooth price over a chosen number of periods. VWAP is usually session-based; moving averages can use many different time windows.

Does VWAP reset every day?

Standard intraday VWAP usually resets at the start of each trading session. Some platforms also offer anchored or custom VWAP tools that begin from a selected point instead of the session open.

Is VWAP a buy or sell signal?

No. VWAP is a benchmark and reference line. A price move around VWAP needs context from volume, price behavior, and acceptance or rejection before the reading becomes meaningful.

What is the difference between VWAP and Anchored VWAP?

Standard VWAP usually starts from the beginning of the current session. Anchored VWAP starts from a chosen event, swing point, date, or other reference point.