ATR stop loss uses Average True Range to calculate a volatility-adjusted stop distance. The useful boundary is simple: ATR measures recent range and market noise, but it does not confirm direction, prove that a setup is valid, or identify the structural invalidation point by itself.

Definition: An ATR stop loss is a stop-distance method that uses the Average True Range value, usually multiplied by a chosen factor, to account for normal price movement before a stop level is reached.

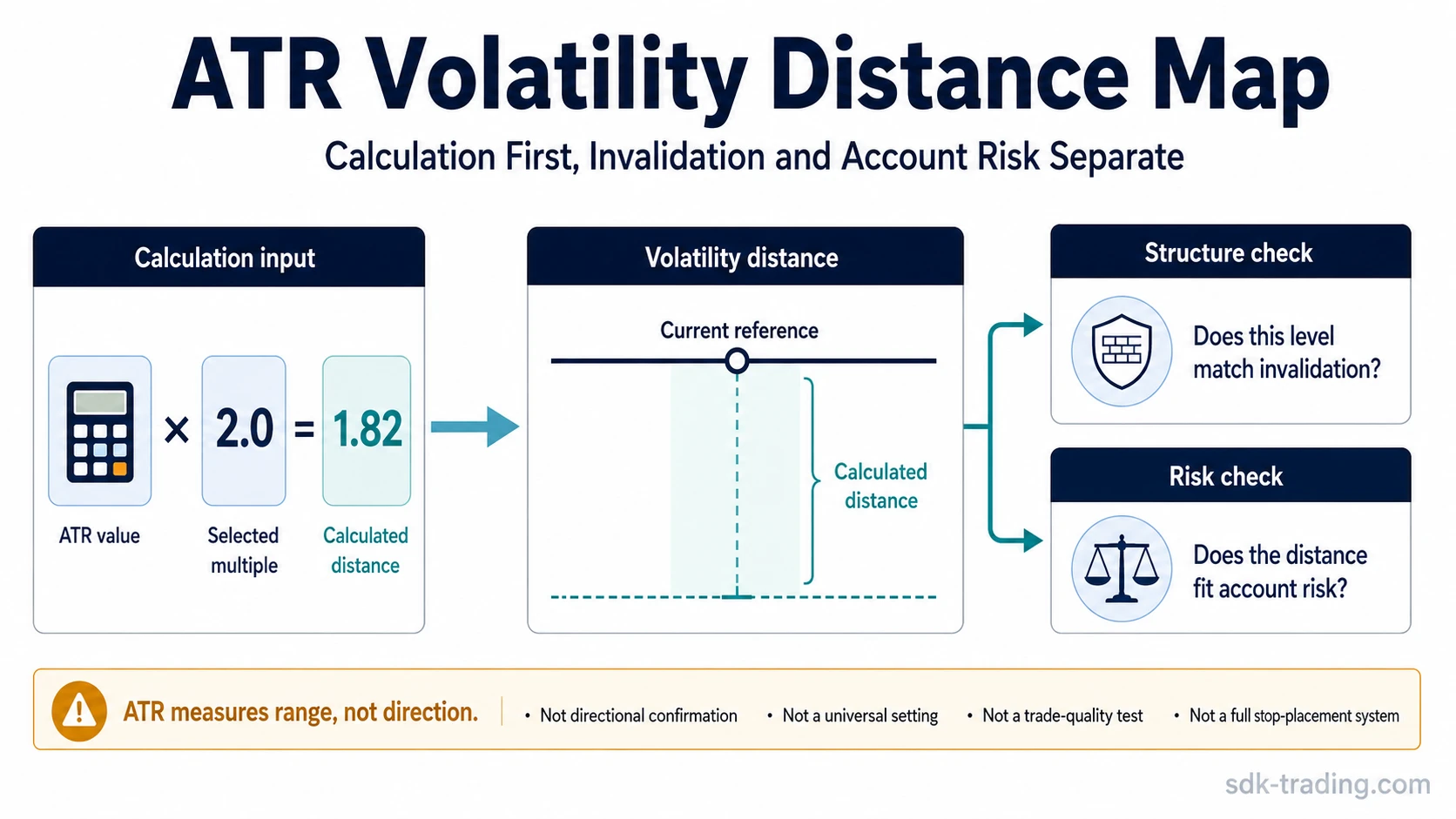

The common misread begins when ATR distance is treated as the whole stop decision. A wider ATR-based distance may sit outside more ordinary range movement, but the stop still has to relate to the market structure being invalidated and the account risk created by that distance.

Key Points

- ATR stop loss is based on volatility distance, not directional evidence.

- The basic calculation is ATR value multiplied by a selected ATR multiple.

- A wider ATR value increases the calculated stop distance and can increase account risk if position size is unchanged.

- ATR can help separate normal noise from a tighter fixed distance, but it cannot replace structural invalidation.

- ATR stop loss and ATR trailing stop are related, but they solve different problems.

What ATR Stop Loss Means

An ATR stop loss connects a stop loss distance to recent market range. If ATR is low, the calculated distance is usually tighter. If ATR expands, the calculated distance becomes wider. The calculation responds to volatility, not to whether the market is likely to rise or fall.

That makes ATR useful as a distance reference, but limited as a decision tool. A market can have a large ATR during disorderly movement, a small ATR before expansion, or a rising ATR after a sharp move has already occurred. In each case, the number describes range conditions. It does not decide whether the trade idea still makes sense.

Boundary: ATR can define a volatility allowance. Structure defines what would make the idea wrong. Account risk defines whether the resulting distance is acceptable for the position size.

How ATR Stop Loss Is Calculated

The basic educational formula is:

| Input | Meaning | Role in the calculation |

|---|---|---|

| ATR value | The recent average true range of price movement | Sets the volatility unit |

| ATR multiple | The selected factor applied to ATR | Expands or contracts the distance |

| Calculated stop distance | ATR value x ATR multiple | Creates the volatility-based distance |

For example, if ATR is 2 points and the selected multiple is 1.5, the calculated distance is 3 points. That is a distance calculation only. It does not say that 1.5 is the correct multiple, that 3 points is enough risk allowance, or that the market structure is valid.

Limitation: A formula can calculate distance, but it cannot decide the quality of the level. A stop placed at a volatility distance can still be poorly aligned if the actual invalidation area is closer, farther away, or structurally unrelated.

ATR Stop Loss and Volatility Conditions

ATR changes the stop-distance conversation because the same chart level can carry different risk under different volatility conditions. The practical issue is not only where the calculated distance lands. It is also what that distance implies for account exposure if the position size stays the same.

| Condition | What ATR changes | Practical limitation |

|---|---|---|

| Low ATR | The calculated stop distance becomes tighter. | A tight distance may sit inside normal noise if the market begins expanding. |

| Rising ATR | The calculated distance starts widening. | The wider distance may appear after volatility has already expanded. |

| High ATR | The calculated stop distance becomes larger. | Account risk can rise materially if position size is not adjusted. |

| ATR after sudden expansion | The formula may reflect the recent shock. | The distance may lag the current structure if volatility normalizes or compresses. |

| ATR near a structural level | The calculated distance can sit beyond ordinary range movement. | The level still needs a separate invalidation reason. |

The cleanest use is to treat ATR as a volatility input. It can help frame how much movement is ordinary relative to recent range, but the market can still reject, accept, or break a level for reasons that ATR alone does not describe.

ATR Stop Loss vs ATR Trailing Stop

ATR stop loss and trailing stop logic can both use volatility, but they are not the same concept.

| Concept | Main function | Key limitation |

|---|---|---|

| ATR stop loss | Calculates an initial or reference stop distance using volatility. | It does not prove where structural invalidation belongs. |

| ATR trailing stop | Moves the stop reference as price and volatility conditions change. | It can still trail too closely or too widely depending on market behavior. |

The distinction matters because a trailing mechanism changes the stop reference over time, while an ATR stop-loss calculation can be used simply to estimate a volatility-based distance. Confusing the two can turn a distance calculation into a moving exit process without checking whether that process fits the underlying structure.

When ATR Stop Loss Can Mislead

ATR can mislead when the calculated distance is treated as a valid stop location by default. The number can be mathematically consistent and still poorly matched to the market structure.

Illustrative scenario: Price is trading above a visible support area. A trader calculates one ATR below that area to avoid ordinary noise. The market then moves through support and stabilizes slightly beyond the ATR distance. The ATR-based distance described recent range, but the actual question was whether the support area had been accepted, rejected, or invalidated. The volatility allowance and the invalidation logic were related, but not identical.

The same issue appears when ATR expands sharply. A wider stop distance can look more tolerant, but it also increases the amount at risk per unit if position size is unchanged. That makes ATR part of risk containment, not a substitute for risk control.

Common mistake: Treating an ATR multiple as a universal setting turns a volatility measurement into a rule it was not designed to be. Different instruments, timeframes, liquidity conditions, and structure types can produce very different meanings from the same multiple.

How ATR Relates to Stop-Loss Risk

ATR stop loss changes the distance side of risk. Account risk also depends on position size. If the ATR-based distance widens and position size does not change, the amount at risk usually rises. If position size is adjusted, the same ATR distance can represent a different risk exposure.

This is why ATR should not be read in isolation. A volatility-based stop distance can be reasonable only when three pieces are separated:

- Range allowance: ATR estimates recent movement and noise.

- Structural invalidation: The chart or setup defines what would make the idea wrong.

- Account risk: Position size determines how much the wider or tighter distance matters financially.

ATR contributes to the first piece. It can inform the second piece, but it does not replace it. It affects the third piece because distance changes risk exposure when size is held constant.

Where ATR Stop Loss Fits Best

ATR stop loss fits best as a volatility-distance reference inside a broader risk process. It is most useful when the question is whether a stop distance is too tight for current range conditions or too wide for acceptable account risk.

It fits poorly when the question is directional. A higher ATR does not make a bullish or bearish outcome more valid by itself. A lower ATR does not mean risk has disappeared. ATR only describes the range environment that the stop distance must survive.

Clean interpretation: ATR can help estimate how much room price has recently needed to move. It cannot decide whether that room is justified, whether the idea is still valid, or whether the risk is acceptable.

FAQ

What is an ATR stop loss?

An ATR stop loss is a volatility-based stop-distance method that uses Average True Range to estimate how far a stop level may need to sit from price or structure to account for recent range movement.

How is ATR stop loss calculated?

The basic calculation is ATR value multiplied by a selected ATR multiple. The result is a stop-distance estimate, not a universal placement rule.

Is ATR stop loss the same as a trailing stop?

No. ATR stop loss calculates a volatility-based distance. An ATR trailing stop moves the stop reference as price and volatility conditions change.

Does ATR confirm trade direction?

No. ATR measures range and volatility. It does not confirm whether price is likely to rise, fall, continue, or reverse.

Can ATR replace a stop-loss invalidation level?

No. ATR can help estimate noise allowance, but invalidation depends on the structure or condition that would make the original idea wrong.