An ATR trailing stop reacts to market range, not market direction. It uses Average True Range to create a trailing threshold that adjusts as volatility changes, but the threshold itself does not show whether a move is strong, weak, or worth acting on.

The safer reading is distance context. When recent candles become wider, the ATR-derived threshold usually moves farther away from price. When recent range contracts, the threshold may sit closer. That change reflects the recent movement environment, not a separate judgment about direction or quality.

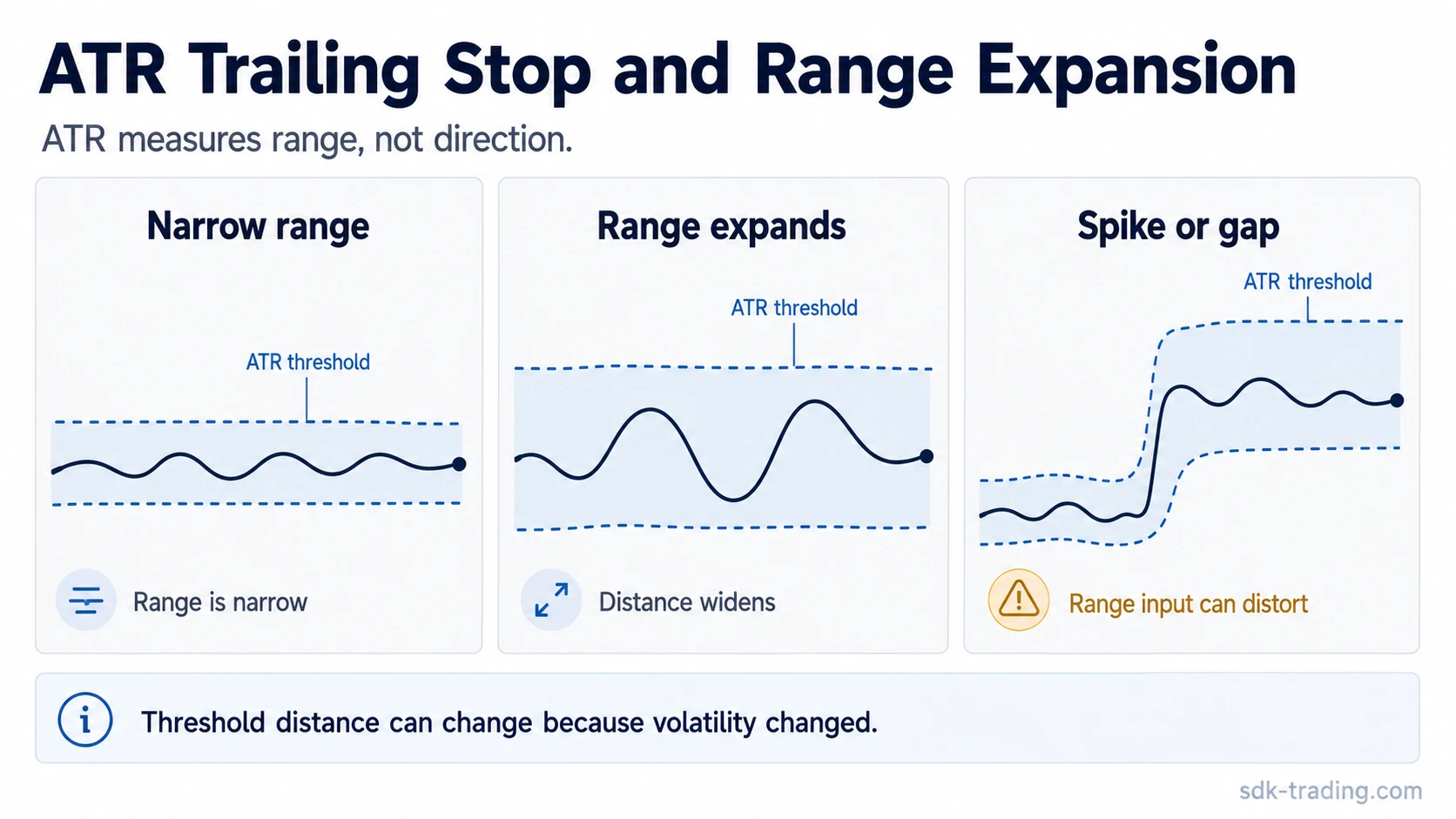

What an ATR Trailing Stop Shows

An ATR trailing stop is a volatility-adjusted level that follows price using recent range as its input. The level is usually calculated from an Average True Range value multiplied by a chosen factor, then offset from a trailing reference such as price, high, low, close, or another platform-defined reference.

The result is a moving threshold. It can help frame whether price has moved beyond a volatility-based boundary, but it should not be read as proof that the market has changed direction cleanly. A threshold can move because volatility changed, even when the directional evidence remains mixed.

Safe interpretation: ATR measures range. An ATR trailing stop converts that range into a trailing threshold. Range expansion can widen the threshold without making the underlying move more dependable.

How the ATR Trailing Stop Is Calculated

The exact formula can vary by charting platform, but most ATR trailing stop calculations use the same basic parts: an ATR period, a true range calculation, a multiplier, and a trailing reference point.

| Calculation part | What it controls | Why it matters |

|---|---|---|

| ATR period | How many candles are averaged | A shorter period reacts faster, while a longer period smooths more recent noise. |

| True range basis | The candle range input used by ATR | Gaps and large candles can expand the range input sharply. |

| Multiplier or factor | How far the threshold is offset from the reference | A larger multiplier creates a wider threshold; a smaller multiplier creates a tighter one. |

| Trailing reference | The price point the ATR distance is applied from | Different implementations may trail from close, high, low, or another reference. |

A simplified way to think about the mechanism is: recent range is measured, multiplied, and then used as a distance offset. The calculation does not evaluate trend quality on its own.

What the ATR Multiplier Changes

The multiplier controls how sensitive the ATR trailing stop is to price movement. A higher multiplier places the threshold farther away from the trailing reference. A lower multiplier places it closer.

A wider threshold may reduce reactions to ordinary candle noise, but it can also respond more slowly. A tighter threshold may react sooner, but it can also be more vulnerable to normal back-and-forth movement. Neither setting is automatically better because the useful setting depends on range behavior, chart timeframe, and the reason the threshold is being watched.

| Parameter choice | Likely effect | Main trade-off |

|---|---|---|

| Higher multiplier | Wider threshold | Less sensitive, but slower to react |

| Lower multiplier | Tighter threshold | More responsive, but more exposed to noise |

| Shorter ATR period | Faster range adjustment | Can overreact to short-term volatility |

| Longer ATR period | Smoother range estimate | Can adapt slowly after volatility changes |

Condition, Misread, Safer Reading

The main mistake is treating the ATR trailing stop as if it explains more than it measures. The threshold reflects a volatility-adjusted distance assumption. It does not replace separate context for direction, structure, momentum, or risk.

| Condition | Common misread | Safer reading |

|---|---|---|

| Low ATR | Risk is low | Recent range is narrow; sharp expansion can still occur. |

| Rising ATR | The move is stronger | Range is expanding; direction still needs separate evidence. |

| ATR spike | The threshold is more dependable | One extreme move may distort the distance calculation. |

| Price crosses the threshold | The move is automatically meaningful | It may mark a threshold breach or a context change to review, not trade quality. |

| Threshold distance changes | The reading is more reliable | The range assumption changed; separate context still matters. |

When ATR Trailing Stops Become Misleading

An ATR trailing stop becomes less stable when the recent range input is distorted. A gap, news-driven candle, or sudden volatility burst can expand ATR quickly, which then pushes the threshold farther away from the trailing reference.

Lag is another limitation. Because ATR is based on prior range, the threshold adjusts after volatility has already appeared. In a choppy market, price can move across a volatility-adjusted level without giving a clean reading of broader structure.

Parameter sensitivity also matters. A period and multiplier that look reasonable in one range environment may become too tight after a volatility spike or too wide after range contracts. The threshold should be read as a changing measurement, not a fixed quality filter.

Modified calculation note: Some implementations may smooth or modify ATR trailing stop behavior to reduce sensitivity to extreme moves. That can make the threshold less jumpy, but it does not remove the basic limitation: a range-based input still does not decide direction.

ATR Trailing Stop vs Other Volatility Tools

An ATR trailing stop uses ATR as a range-based distance input. Its focus is the moving threshold created from recent candle movement.

Bollinger Bands use a volatility envelope around a moving average, so they are usually read as bands around price rather than as a single trailing threshold.

The standard deviation indicator focuses on dispersion around an average, which is different from ATR’s true-range-based movement measurement.

| Tool | Main input | Typical reading |

|---|---|---|

| ATR trailing stop | ATR range multiplied into a trailing distance | Volatility-adjusted threshold |

| ATR | True range average | Recent movement range |

| Bollinger Bands | Moving average plus volatility envelope | Price position inside expanding or contracting bands |

| Standard deviation | Dispersion around an average | How spread out values are around the mean |

Practical Scenario: Range Expansion Changes the Threshold

Imagine price has been moving in relatively narrow candles for several sessions. ATR remains low, so the trailing threshold sits relatively close to the trailing reference. Then a wider candle appears, followed by a gap and a session with larger intraday movement.

As those wider ranges enter the ATR calculation, the ATR value rises. The threshold moves farther away because the calculation now assumes a wider normal movement band. That wider distance does not mean the market direction became more dependable. It means recent range expanded.

The safer reading is to separate the threshold change from the directional interpretation. The ATR trailing stop can show that the volatility-adjusted distance has changed, while separate structure, momentum, and context still determine whether the move has a cleaner interpretation.

Key Points

- An ATR trailing stop is a volatility-adjusted trailing threshold.

- ATR measures range, not direction.

- The ATR period controls how much recent movement is averaged.

- The multiplier controls how wide or tight the threshold becomes.

- Gaps and volatility spikes can distort the threshold distance.

- A threshold breach can flag a context change, but it does not prove trade quality.

- A safer reading is distance context, not standalone confirmation.

ATR Trailing Stop FAQ

What does an ATR trailing stop show?

An ATR trailing stop shows a trailing threshold based on recent market range. It adjusts as ATR changes, so the level can widen during higher range conditions and tighten when range contracts.

How is an ATR trailing stop calculated?

Most versions calculate ATR over a selected period, multiply that ATR by a chosen factor, and offset the result from a trailing reference such as price, high, low, or close. Exact implementation can vary by platform.

Does an ATR trailing stop show direction?

No. ATR is a range measure. An ATR trailing stop can show a volatility-adjusted threshold, but direction and quality require separate evidence.

Why can an ATR trailing stop give false readings?

False readings can appear when the market is choppy, when ATR lags a sudden change, or when a gap or spike distorts the recent range input. In those cases, the threshold may move because volatility changed rather than because the broader context improved.