A fear and greed cycle in trading is a decision-pressure pattern where greed can push a trader toward urgency and overcommitment, while fear can compress judgment after stress appears. It is not a buy/sell model, a live sentiment score, or proof that the market must reverse.

The useful use is internal and diagnostic. The cycle helps separate current market evidence from the trader’s emotional weighting of that evidence. Greed can make new opportunity feel more important than the plan allows. Fear can make recent stress feel more decisive than the evidence supports.

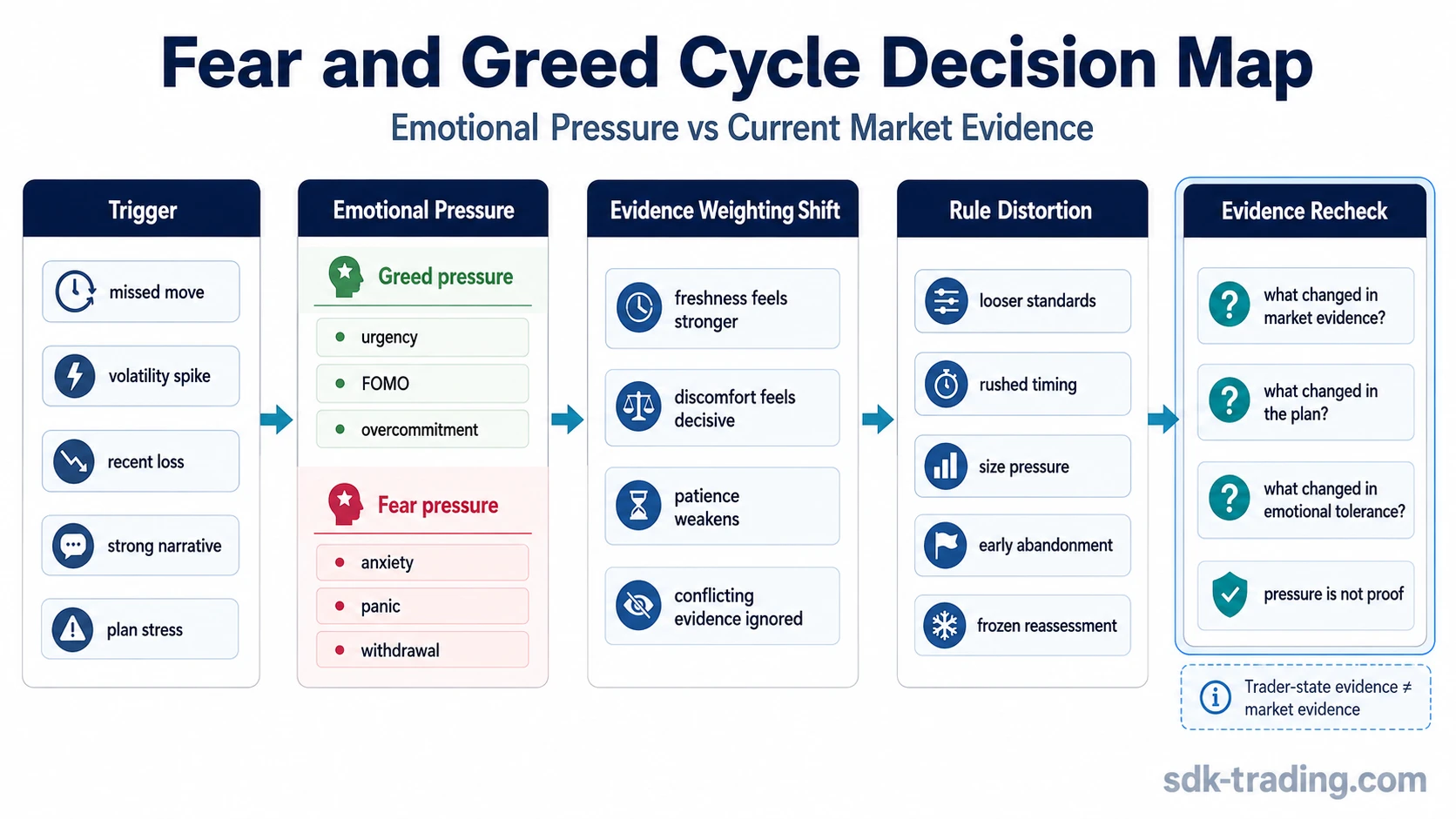

Core idea: the fear and greed cycle describes how emotional pressure can move from opportunity-seeking to urgency, anxiety, panic, withdrawal, or reassessment. The trading question is not whether fear or greed is present. The question is whether those emotions are changing rule adherence, patience, position judgment, or evidence review.

What the fear and greed cycle means in trading

In trading psychology, the fear and greed cycle belongs to emotional discipline. It describes a recurring shift in trader state: confidence and opportunity focus can become greed pressure, greed pressure can become urgency, and later stress can turn into fear pressure, hesitation, panic, or avoidance.

The cycle is not the same as market sentiment. Market sentiment describes a broader crowd condition. The fear and greed cycle describes how a trader may react to that condition. A market can be euphoric while an individual trader remains disciplined, and a trader can feel fear even when the evidence has not materially changed.

Trading discipline context: emotional discipline is the broader skill. The fear and greed cycle is one way emotional discipline can break down when the trader starts weighting pressure more heavily than evidence.

How greed pressure can shift trading decisions

Greed pressure often begins with opportunity focus. A trader sees movement, hears stronger narratives, notices others acting, or feels that patience is becoming expensive. The problem is not optimism by itself. The problem appears when optimism starts reducing the quality of the evidence check.

Greed can distort a decision by making the trader accept weaker confirmation, increase size beyond the plan, chase a move after the cleanest point has passed, or reinterpret hesitation as lost opportunity. In that state, the trader may still use analytical language, but the underlying decision has shifted from evidence review toward urgency.

This is where FOMO trading becomes the closer concept. FOMO is the more specific greed-side pressure that appears when the trader fears missing a move and starts treating participation as more important than process quality.

How fear pressure can shift trading decisions

Fear pressure usually becomes stronger after stress appears. A move goes against the trader’s expectation, volatility increases, recent losses affect confidence, or the trader begins to focus more on avoiding discomfort than reading the current structure.

Fear can distort judgment by making the trader close the evidence review too early, abandon a plan without checking invalidation, hesitate when a valid reassessment is needed, or avoid future setups because the last experience still feels too present. Fear may also create the opposite problem: the trader may freeze and refuse to reassess because accepting the evidence feels uncomfortable.

The fear-side extreme connects naturally to panic selling, where pressure can turn into reactive exit behavior. Panic selling is not the whole fear and greed cycle, but it is one clear outcome when fear pressure overwhelms evidence review.

Fear and greed cycle phases

The cycle does not have to appear in a perfect sequence. The phases below are best treated as a diagnostic map, not as a fixed market script.

| Phase | Typical pressure | Decision risk | Cleaner evidence question |

|---|---|---|---|

| Opportunity focus | The trader sees potential and becomes more attentive to upside or continuation. | Normal interest can begin turning into selective evidence use. | Has the evidence improved, or has attention only shifted toward opportunity? |

| Greed pressure | The trader wants more exposure, faster action, or looser standards. | Risk tolerance may expand without a matching improvement in structure. | Would the same decision still make sense without urgency? |

| Euphoria or overconfidence | The trader feels unusually certain or dismisses conflicting information. | Position quality can become secondary to conviction. | What evidence would weaken the idea, and is it being ignored? |

| Anxiety | The trader starts monitoring discomfort more than market behavior. | Noise may feel like confirmation that something is wrong. | Has the setup changed, or has emotional tolerance changed? |

| Fear pressure | The trader becomes focused on avoiding further stress. | Rules may be abandoned, rushed, or defended for emotional relief. | What does the plan say should be reassessed now? |

| Panic or withdrawal | The trader wants immediate relief or avoids decisions altogether. | Action or inaction may become pressure-driven rather than evidence-driven. | Which facts are current, and which reactions come from recent stress? |

| Reassessment | The trader slows the loop and separates pressure from evidence. | The main risk is forcing a lesson before the facts are reviewed clearly. | What changed in market evidence, execution quality, and emotional state? |

How to separate emotional pressure from market evidence

The cleanest use of the fear and greed cycle is a short evidence recheck. A trader can ask whether the decision is being driven by current information or by the need to reduce emotional discomfort.

| Emotion pressure | Decision distortion | Evidence recheck question | Related concept |

|---|---|---|---|

| Greed | Accepting weaker conditions because the move feels urgent. | Has confirmation improved, or has patience weakened? | FOMO trading |

| Overconfidence | Ignoring conflicting evidence because the idea feels obvious. | What would invalidate or weaken the current interpretation? | Market euphoria |

| Anxiety | Reading normal uncertainty as a reason to abandon the plan. | Is the discomfort new, or is the evidence materially different? | Trading anxiety |

| Fear | Reducing judgment to immediate relief from stress. | Which action would still make sense after the pressure fades? | Panic selling |

| Frustration | Trying to recover emotional balance through the next decision. | Is the next decision based on the current setup or the prior outcome? | Trading frustration |

A practical scenario is a trader who sees a strong move after waiting for a cleaner setup. Greed pressure may say that waiting was a mistake and that immediate participation is necessary. A cleaner review asks whether the original conditions have improved, weakened, or simply moved without the planned confirmation.

Common mistake: treating emotion as proof

The common mistake is treating emotional intensity as market evidence. Strong greed does not prove opportunity quality. Strong fear does not prove danger by itself. Both emotions may appear around real market changes, but neither one explains whether the current evidence is strong enough.

Important distinction: emotional pressure is evidence about the trader’s state. It is not automatic evidence about the market. The market evidence still has to come from structure, context, confirmation, invalidation, liquidity, volatility, or whatever inputs the trading plan actually uses.

This distinction prevents two opposite errors. The first is chasing because greed feels like opportunity. The second is retreating because fear feels like proof. In both cases, the emotional state may be real, but the market interpretation still requires a separate check.

Limitations of the fear and greed cycle

The fear and greed cycle is useful because it gives language to emotional pressure. Its limitation is that it can become too broad if it is used as a complete market explanation. A trader can feel greedy in a weak setup, fearful in a valid setup, calm in a risky setup, or confident in a setup that later fails.

Fear and greed can also reflect real information. A trader may feel fear because volatility, liquidity, or invalidation risk has actually changed. A trader may feel opportunity because evidence has improved. The discipline problem appears when the feeling replaces the evidence review instead of prompting a better one.

Limitation example: a sudden increase in stress after a fast move does not automatically mean the trader should reverse course. It means the trader should separate three items: what changed in the market, what changed in the plan, and what changed in emotional tolerance.

Related trading psychology concepts

Greed-side pressure is closest to FOMO trading, because both involve urgency, missed-move pressure, and reduced patience. Fear-side pressure is closest to panic selling, because both involve stress-driven reaction and a weaker separation between evidence and emotional relief.

Nearby concepts include market euphoria, trading anxiety, trading frustration, and emotional discipline. Each concept isolates a different part of the decision process. The fear and greed cycle connects them by showing how emotional pressure can move from opportunity-seeking to stress response.

FAQ

Is the fear and greed cycle a trading signal?

No. The fear and greed cycle is a trading psychology framework for reviewing emotional pressure. It does not confirm direction, timing, entry quality, or exit quality by itself.

How is the fear and greed cycle different from a fear and greed index?

A fear and greed index usually summarizes market sentiment inputs. The trading psychology cycle focuses on how a trader’s own pressure can change evidence weighting, patience, and rule adherence.

Can fear or greed ever reflect real market evidence?

Yes. Fear or greed can appear when market conditions actually change. The key is to check whether the evidence changed first, instead of treating the emotional intensity as proof.