A VWAP strategy is a framework for reading where price trades in relation to the session’s volume-weighted average price. It uses VWAP as a session reference for context and confirmation, not as an automatic entry signal or a prediction tool.

The useful question is not simply whether price is above or below VWAP. The stronger question is whether price is accepting, rejecting, rotating around, or repeatedly crossing that reference while volume and market conditions support the reading.

The full calculation and indicator mechanics belong in the main VWAP explanation. In a strategy framework, VWAP should stay tied to context, acceptance, rejection, and failure conditions instead of becoming a standalone trading system.

Key Points

- VWAP strategy uses the session VWAP line as a reference for price location, not as a guaranteed support or resistance level.

- The reading changes depending on session context, trend behavior, liquidity, volume participation, and whether price accepts or rejects the VWAP area.

- Pullbacks, reclaim moves, and reversion readings are interpretation scenarios, not direct trade instructions.

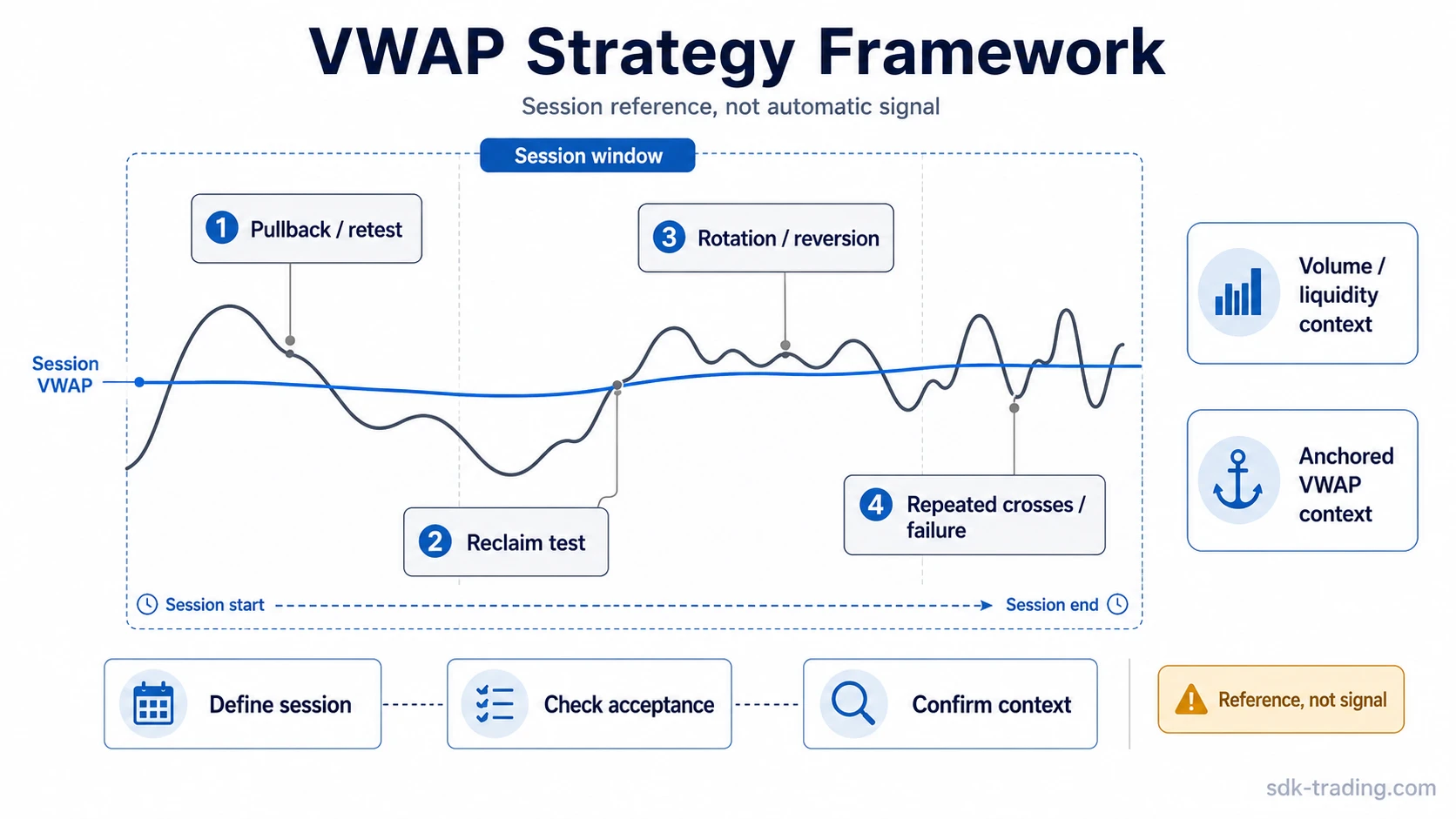

- Repeated VWAP crosses often signal a less useful environment because the reference is not separating price behavior clearly.

- Other volume tools can add context, but they should not be stacked mechanically to force a signal.

What a VWAP Strategy Means

A VWAP strategy means using volume-weighted average price as a decision reference inside a broader framework. The line helps organize the session: where price has traded relative to volume, whether the market is accepting one side of that reference, and whether a move away from VWAP has enough participation to matter.

The framework is conditional. A price move above VWAP can show that current trading is occurring above the session’s volume-weighted reference, but that does not prove control, continuation, or trade quality. A move below VWAP can show the opposite relationship, but it still needs context before the reading becomes useful.

Working definition: VWAP strategy is the use of VWAP as a session-based reference for reading price location, acceptance, rejection, and failure conditions. It is not a complete system by itself.

The same VWAP touch can mean different things depending on trend direction, volume behavior, and whether price holds, rejects, or rotates through the area. That is why the framework should separate context, condition, interpretation, and limitation.

The Session Boundary Behind VWAP

Most intraday VWAP readings are session-based. That means the calculation resets around the session window used by the chart or platform. This boundary matters because VWAP is not simply a moving average. It reflects the average traded price weighted by volume inside the selected session.

A session VWAP can be useful when the active trading day has enough participation to make the reference meaningful. It becomes weaker when early volume is thin, the session is distorted by news, or the market has not yet formed a stable range of participation.

A strategy reader should ask three boundary questions before using VWAP: what session is being measured, how much meaningful volume has occurred, and whether the current price relationship is clear enough to separate acceptance from noise.

Boundary note: A VWAP reading is only as useful as the activity included in its calculation window. If the selected window is not relevant to the decision being evaluated, the line can create false precision.

Core VWAP Strategy Conditions

The first step is to decide what VWAP is doing in the current session. It may act as a neutral reference, a trend filter, a rotation center, or a failed separator. The strategy should not assume that one role applies in every market.

| Condition | What it can indicate | Limit |

|---|---|---|

| Price holds mostly above VWAP | The session is trading above its volume-weighted reference. | It does not confirm continuation by itself. |

| Price holds mostly below VWAP | The session is trading below its volume-weighted reference. | It does not prove downside pressure will continue. |

| Price pulls back toward VWAP | The market is retesting a session reference after moving away from it. | A touch alone is not a setup. |

| Price reclaims VWAP after trading below it | The market is testing whether it can regain the session reference. | A reclaim can fail quickly if acceptance does not follow. |

| Price repeatedly crosses VWAP | The session may be rotational, choppy, or poorly separated. | VWAP becomes less useful as a directional reference. |

| VWAP conflicts with other volume context | The session reference may not align with broader participation. | The reading needs additional context, not stronger certainty. |

The practical sequence is simple: define the session, observe price location, check acceptance or rejection, compare volume behavior, then decide whether the reading is clear enough to use. If any step is unclear, the VWAP line should remain a reference, not a conclusion.

Pullback, Reclaim, and Reversion Readings

A VWAP pullback reading starts after price has moved away from the session reference and returns toward it. The important part is not the touch. The important part is whether price treats the area as a temporary pause, rejects it, or starts rotating through it.

A reclaim reading is different. It appears when price has traded below VWAP and then moves back above it. The useful question is whether price accepts above the reference after reclaiming it. Without acceptance, the move can be a temporary cross rather than a meaningful change in session behavior.

A reversion reading treats VWAP as a central reference inside a rotational session. This can be useful when price stretches away from VWAP and returns toward the session average, but it is also one of the easiest readings to misuse. A stretched price can keep moving if the market is trending or if new information changes the session balance.

Scenario logic example: Price moves above VWAP early, pulls back toward it, and volume expands during the retest. That can support the idea that the session reference is influencing current price behavior, but the interpretation weakens if price slices through VWAP repeatedly or if the pullback occurs during thin liquidity.

These readings are best treated as scenario labels. Pullback, reclaim, and reversion describe how price is interacting with VWAP. They do not define entries, exits, targets, or trade quality without additional process controls.

When VWAP Strategy Fails

VWAP strategy fails most often when the line is treated as more precise than it is. A session reference can be useful, but it cannot remove market uncertainty, liquidity risk, news risk, or the difference between a clean trend and a noisy rotation.

Common failure conditions:

- Price crosses VWAP repeatedly without clear acceptance on either side.

- Volume is too thin for the session reference to carry much informational weight.

- A news-driven repricing overrides normal session balance.

- The trader treats VWAP as fixed support or resistance instead of a reference.

- The setup depends only on price touching VWAP, with no confirmation or invalidation logic.

- VWAP is used outside the timeframe or session context it was meant to describe.

The reading weakens when price repeatedly crosses VWAP without acceptance, when liquidity is thin, or when a news-driven repricing overrides session balance. In those conditions, VWAP can still be visible on the chart, but its usefulness as a framework reference is reduced.

A safer interpretation treats confirmation as a condition, not a guarantee. The framework should ask whether the market is accepting the VWAP relationship, not whether the line has magically produced a signal.

How Anchored VWAP Changes the Reference

Session VWAP starts from the session boundary. anchored VWAP starts from a selected event, such as a swing point, earnings release, breakout, gap, or major reversal attempt. That changes the question being asked.

When session VWAP and anchored VWAP point to similar areas, the market may be referencing both short-term session activity and a broader event-based average. When they conflict, the reader should not force alignment. The conflict can show that the current session and the chosen anchor are describing different participation windows.

This distinction keeps the VWAP strategy page from absorbing the anchored VWAP topic. Session VWAP is mainly about current-session balance. Anchored VWAP is about volume-weighted price behavior from a chosen reference point.

How to Combine VWAP With Volume Tools

Volume tools can help confirm or challenge a VWAP reading, but they should not be used as a mechanical signal stack. Their value comes from showing different calculation lenses around participation, price result, and traded volume distribution.

Volume Profile can show where volume has concentrated by price level. This can help distinguish a VWAP reference from nearby high-volume or low-volume areas, but it should not be treated as proof that price must reverse or continue.

OBV reads volume cumulatively by close direction. It can provide context when price trades above or below VWAP, but it uses a different calculation lens and should not be expected to match VWAP behavior candle by candle.

Force Index combines price change with volume. It can help frame whether a move away from VWAP has force behind it, but it can also spike during unstable conditions where price movement is not cleanly accepted.

| Tool | What it adds to VWAP strategy | What it should not do |

|---|---|---|

| Session VWAP | Shows the current session’s volume-weighted price reference. | Act as a complete strategy. |

| Anchored VWAP | Adds an event-based reference from a selected starting point. | Replace the session boundary without reason. |

| Volume Profile | Shows traded volume distribution by price level. | Predict reversal or continuation. |

| OBV | Shows cumulative volume pressure by close direction. | Confirm VWAP automatically. |

| Force Index | Shows price-change and volume force in the move. | Turn a VWAP cross into a signal. |

VWAP Strategy Checklist

A checklist can keep the reading disciplined, but it should not become a mechanical trade trigger. The purpose is to filter context before drawing a conclusion from the VWAP line.

| Checklist question | What supports the reading | What weakens it | What not to infer |

|---|---|---|---|

| What session boundary is VWAP measuring? | The VWAP window matches the session or decision context being evaluated. | The chart window, trading session, or reference period does not match the decision context. | Do not treat a mismatched VWAP window as precise context. |

| Where is price relative to VWAP? | Price is clearly above, below, or rotating around the session reference. | Price repeatedly crosses VWAP without spending time on either side. | Do not infer control, continuation, or reversal from location alone. |

| Is price accepting or rejecting the VWAP area? | The market holds one side of VWAP after a retest, cross, or reclaim. | The move reverses immediately or becomes a sequence of temporary crosses. | Do not treat the first touch or cross as a complete signal. |

| Does volume participation fit the price result? | Volume behavior is consistent with the observed movement around VWAP. | Volume expands while the price result remains weak, unstable, or quickly reversed. | Do not force volume to confirm a VWAP reading automatically. |

| Are repeated crosses turning the reading into chop? | VWAP still separates price behavior clearly enough to define a useful reference. | VWAP becomes the middle of a noisy rotation with no clear acceptance. | Do not treat a choppy VWAP area as directional evidence. |

| Does anchored VWAP agree or conflict with the session VWAP? | Session and anchored references describe compatible participation windows. | The references describe different windows and point to conflicting context. | Do not force agreement between session and event-based references. |

| Do related volume tools confirm or challenge the reading? | Volume Profile, OBV, or Force Index adds context that fits the VWAP scenario. | The related tool shows a different participation, close-direction, or price-force reading. | Do not stack indicators mechanically until they appear to agree. |

This checklist is a structure for interpretation. It does not decide whether a trade should be taken. It only asks whether VWAP is providing clear enough information to remain part of the decision process.

FAQ

Is VWAP a trading strategy by itself?

No. VWAP is a reference line based on volume-weighted average price. A VWAP strategy uses that reference inside a broader process, but the indicator alone does not define trade quality.

Is VWAP better for intraday or swing trading?

Session VWAP is most commonly used in intraday contexts because it usually resets around the trading session. Swing traders may use anchored references when they want to measure from a selected event or turning point.

What does price above VWAP mean?

Price above VWAP means the market is currently trading above the session’s volume-weighted average reference. It does not automatically mean strength will continue or that a trade is justified.

Why can VWAP fail in choppy markets?

VWAP becomes less useful when price crosses it repeatedly without acceptance. In that environment, the line may describe the middle of a rotation rather than a clean directional reference.

How is anchored VWAP different from session VWAP?

Session VWAP usually measures from the session start. Anchored VWAP measures from a selected point, such as a swing high, swing low, gap, earnings event, or breakout area.