Trading biases are repeatable distortions in how traders filter evidence, form confidence, feel risk, and review outcomes. A bias is not proven only because a trade lost money, and a good result does not automatically mean the decision process was clean.

Key points

- Trading biases distort how decisions are formed and reviewed, not only the final outcome.

- Different biases affect different layers: evidence, reference points, recent memory, confidence, risk discomfort, commitment, and review.

- Recent results, prior conviction, uncomfortable risk, and post-outcome stories can all change how the same information is interpreted.

- A losing trade can come from a reasonable process, while a profitable trade can still contain biased reasoning.

What trading biases are

Trading biases are recurring mental shortcuts or emotional distortions that make market decisions less objective. They can affect what evidence a trader notices, how strongly a thesis is believed, how risk feels, whether a position is held too long, and how the trade is explained afterward.

The useful question is not simply whether the trade made or lost money. The better question is which part of the decision became less balanced. A trader may ignore conflicting evidence, anchor to an earlier view, overreact to recent outcomes, become too confident, avoid taking a loss, defend a prior commitment, or rewrite the story after the result is known.

This makes trading psychology more practical when bias labels are tied to observable review points. Instead of asking only whether the trade was wrong, the review can ask what changed the evidence review, confidence level, risk decision, or post-trade explanation.

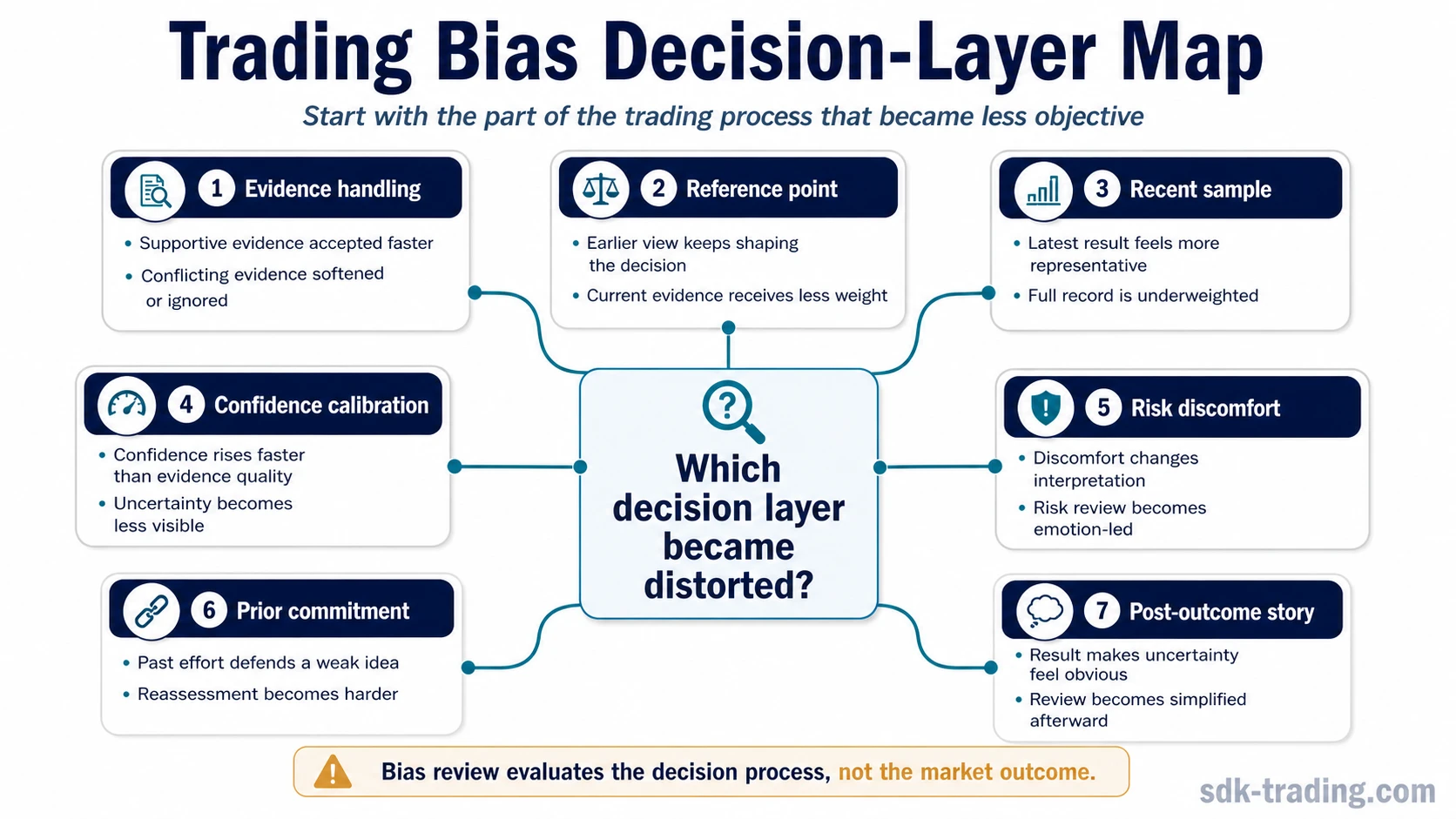

Where biases appear in the trading process

Trading biases can appear before, during, and after a decision. Some affect the evidence a trader accepts. Others affect confidence, risk exposure, patience, or the way a result is interpreted after the fact.

| Decision layer | How bias can appear | Common bias label | Review question |

|---|---|---|---|

| Evidence handling | The trader accepts supportive information more easily than conflicting information. | Confirmation bias | Was opposing evidence reviewed with the same standard? |

| Reference point | An earlier level, thesis, or first impression keeps shaping the decision after conditions change. | Anchoring bias | Is the current view still based on present evidence? |

| Recent sample | The most recent trade, streak, or market move receives too much weight. | Recency bias | Is the latest information being treated as more representative than it is? |

| Confidence calibration | Confidence rises faster than the evidence quality behind the decision. | Overconfidence bias | Does confidence match the strength of the decision record? |

| Loss or risk discomfort | The trader avoids realizing an unfavorable outcome or changes the plan mainly to reduce discomfort. | Loss aversion / disposition effect | Is the decision based on structure or on the discomfort of accepting loss? |

| Prior commitment | Past effort, time, or emotional investment makes the trader defend a weak idea. | Sunk cost fallacy | Would the same decision be made if no prior commitment existed? |

| Post-outcome story | The result makes the earlier uncertainty feel obvious in hindsight. | Hindsight bias | Does the review preserve what was actually known before the result? |

Common trading bias categories

A broad list of biases is less useful than a classification by decision layer. The categories below help separate problems that can look similar after a trade is finished.

| Category | What becomes distorted | Example of the distortion |

|---|---|---|

| Cognitive evidence bias | Information selection and interpretation | A trader gives more weight to evidence that supports the original thesis and softens evidence that challenges it. |

| Memory and sample bias | What feels representative | A recent sequence of favorable or unfavorable outcomes changes confidence more than the full decision record supports. |

| Confidence bias | Belief strength versus evidence quality | The trader becomes more certain even though the evidence remains mixed or incomplete. |

| Risk-response bias | Reaction to discomfort, loss, or uncertainty | The trader changes the interpretation because accepting the planned risk feels uncomfortable. |

| Commitment bias | Attachment to a prior decision | The trader keeps defending an idea because time, effort, or identity has already been invested in it. |

| Review bias | Post-outcome explanation | The final result makes the earlier decision appear more obvious than it actually was at the time. |

Trading bias examples

The examples below are illustrative scenarios. They do not describe a specific asset, result, entry, exit, target, or performance outcome.

Evidence filtering: A trader begins with a clear thesis and then mainly notices information that agrees with it. Conflicting evidence is explained away as noise. The issue is not having a thesis; the issue is testing supportive and opposing evidence with different standards.

Recent-result distortion: After several similar outcomes, a trader starts treating the latest sample as if it makes the next decision easier. The process becomes weaker if confidence changes more than the evidence record justifies.

Risk discomfort: A trader knows the original reasoning has weakened but keeps searching for reasons to avoid accepting that change. The bias is not the presence of discomfort; the problem is allowing discomfort to replace the decision criteria.

Post-outcome simplification: After the result is known, the earlier uncertainty is compressed into a cleaner story. The review sounds obvious afterward even though the pre-decision record contained mixed evidence and alternative paths.

Why outcome alone is not enough to identify bias

A bias label should not be assigned only because the trade result was unfavorable. The label should come from the distorted layer: how evidence was filtered, how confidence was formed, how risk was handled, how commitment was defended, or how the result was reviewed.

Outcome-only review creates two opposite mistakes. A losing trade may be treated as biased even when the decision was reasonable under uncertainty. A profitable trade may be treated as high-quality even when the reasoning depended on selective evidence, excessive confidence, or refusal to reassess.

A better review keeps the pre-trade record separate from the post-trade story. The trader can then ask whether the decision was supported by the evidence available at the time, not whether the result makes the decision look good or bad afterward.

How trading biases affect evidence, confidence, and risk

Biases often become visible when one part of the decision moves faster than the others. Confidence may increase while evidence quality remains unchanged. Risk exposure may rise because the last few outcomes felt encouraging. A prior thesis may keep its emotional force after the supporting evidence has weakened.

| Process area | Balanced version | Biased version |

|---|---|---|

| Evidence | Supportive and conflicting information are reviewed together. | Supportive information is accepted quickly while conflicting information is discounted. |

| Confidence | Confidence reflects evidence quality and uncertainty. | Confidence rises because the idea feels familiar, recent, or emotionally comfortable. |

| Risk | Risk is evaluated before discomfort changes the interpretation. | Risk is adjusted, ignored, or defended because the original plan feels difficult to accept. |

| Review | The review compares the decision record with the information available at the time. | The result rewrites the story and makes uncertainty disappear afterward. |

Awareness of bias is not enough

Knowing the name of a bias does not automatically improve decision quality. A trader can recognize confirmation bias, recency bias, or loss aversion in theory and still repeat the same pattern when uncertainty, pressure, or discomfort returns.

A bias review becomes more useful when it is tied to a record: what evidence was available, what was ignored, how confident the trader felt, what risk was accepted, what would have changed the view, and how the result was interpreted afterward.

This keeps trading psychology from becoming a list of labels. The practical value comes from identifying the step that needs a cleaner check before the next decision.

How to review trading bias without turning it into a signal

Bias review should improve decision discipline, not create a new trading signal. A bias label does not say what the market will do next. It only describes where the trader’s interpretation may have become less objective.

| Review area | Question to ask | What the answer can reveal |

|---|---|---|

| Pre-decision evidence | What evidence supported the idea, and what evidence challenged it? | Whether evidence was handled symmetrically. |

| Confidence level | Was confidence based on evidence quality or on familiarity, recent outcomes, or conviction? | Whether belief strength became larger than the record supported. |

| Risk exposure | Did risk feel acceptable because the plan was clear, or because discomfort was being avoided? | Whether risk handling was process-based or emotion-based. |

| Alternative scenarios | Were reasonable alternatives considered before the result was known? | Whether the decision allowed uncertainty to remain visible. |

| Post-trade review | Did the result change the story more than the pre-trade record justified? | Whether hindsight simplified the original uncertainty. |

The goal is not to remove all emotion or all uncertainty. The goal is to keep the decision record clear enough that evidence, confidence, risk, and review can be judged separately.

Common mistakes when reviewing trading biases

| Mistake | Safer interpretation |

|---|---|

| Calling every losing trade biased | A loss can happen even when the process was reasonable under uncertainty. |

| Calling every profitable trade disciplined | A good result can still come from selective evidence, weak review, or excessive confidence. |

| Using bias labels as blame | The label should identify the distorted decision layer, not act as a judgment of the trader. |

| Trying to fix bias with awareness alone | Awareness needs a review structure, otherwise the same pattern can return under pressure. |

| Treating bias review as a market forecast | Bias review evaluates decision quality; it does not predict the next market move. |

Trading biases FAQ

Are trading biases the same as emotions?

No. Emotions can influence trading decisions, but a bias is the repeatable distortion that changes how evidence, confidence, risk, or review is handled. A trader can feel emotion without becoming biased, and a biased decision can also appear calm or rational on the surface.

Can a profitable trade still involve bias?

Yes. A profitable result does not prove that the decision process was clean. A trade can end favorably even if the trader ignored conflicting evidence, became overconfident, or explained away information that should have triggered reassessment.

Is a losing trade always evidence of bias?

No. A losing trade can come from a reasonable decision made under uncertainty. Bias is better identified by reviewing the process layer that became distorted, not by judging the result alone.

How can traders review bias without judging only the result?

They can compare the pre-decision record with the post-result explanation. The review should ask what evidence was available, what alternatives were considered, how confidence was calibrated, how risk was accepted, and whether the outcome changed the story afterward.