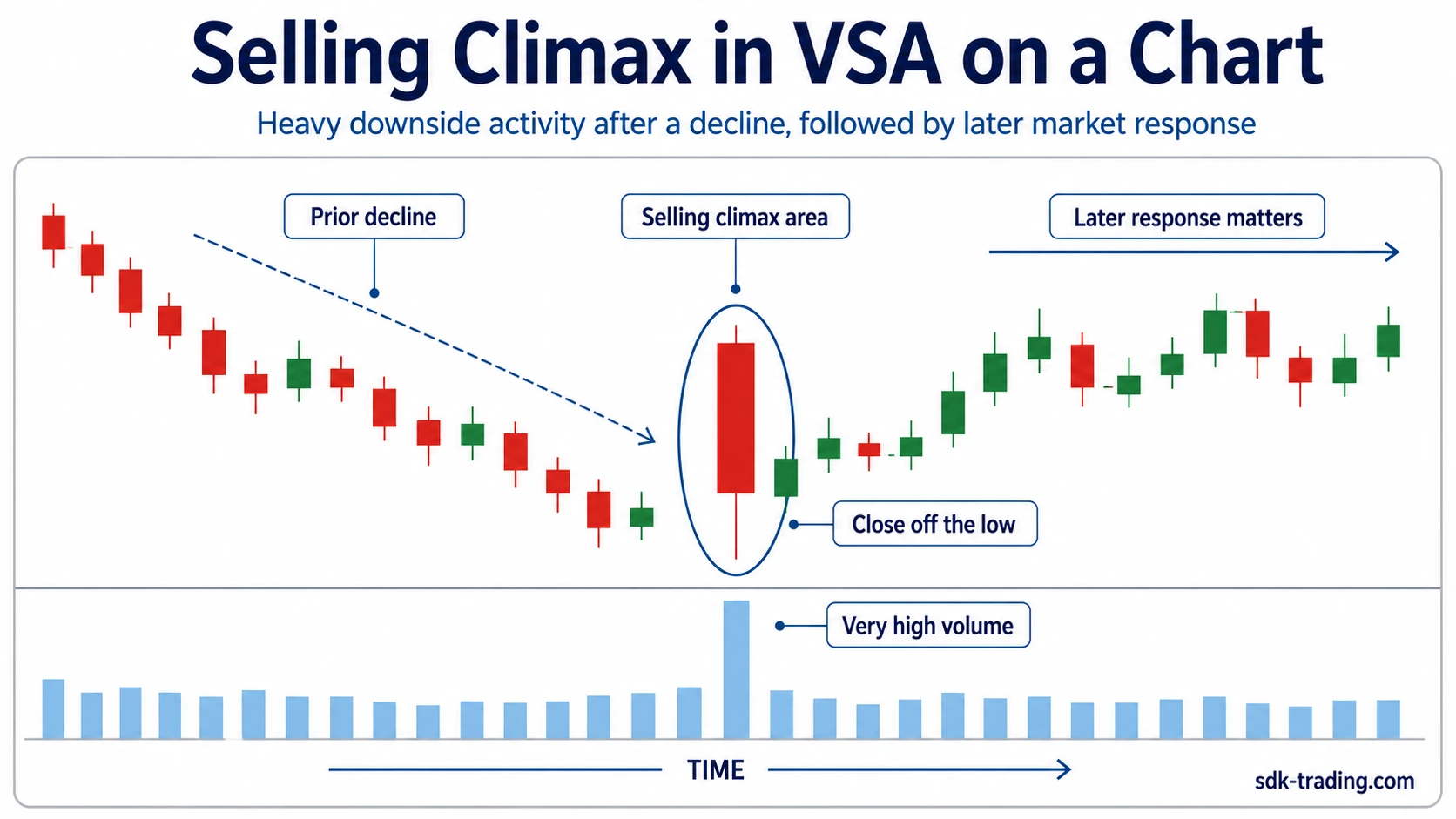

A selling climax is a high-volume downside event in VSA and Wyckoff analysis after a sustained decline. It can show that heavy selling is becoming extreme or meeting demand, but it is not a standalone bullish reversal signal. The reading only gains value when later price and volume behavior shows whether downside continuation is failing or supply still controls the move.

Key Points

- A selling climax is a high-volume downside event, not automatic proof of a bullish reversal.

- Volume, spread, and close location need to be read together rather than in isolation.

- Context matters: prior decline, panic-like activity, possible absorption, and later behavior all affect the interpretation.

- The reading strengthens only when later price action shows reduced downside efficiency, failed renewed selling, or a stronger demand response.

- A selling climax can overlap with stopping-volume logic, but the two terms are not identical.

What Is a Selling Climax?

A selling climax is a Volume Spread Analysis and Wyckoff event where downside activity expands sharply after a period of selling pressure. The market may print unusually high volume, a wide down bar or wide downside range, and a close that starts to show resistance to further downside progress.

The important word is may. A selling climax can suggest that selling pressure is becoming extreme, but the observation itself does not prove that accumulation has started or that the decline has ended. It is a condition to interpret, not a command to act.

In a stronger reading, the market shows heavy downside effort but fails to keep making efficient downside progress afterward. That later failure gives the original event more meaning. Without that follow-through evidence, the same high-volume decline may simply reflect continuing weakness.

Definition: A selling climax is a high-activity downside event after sustained selling pressure. It becomes meaningful only when later behavior shows whether supply is being absorbed, tested, or still driving price lower.

What a Selling Climax Is Not

The safest boundary is simple: high volume shows activity, not intent. A wide down bar shows range, not automatic absorption. A close off the low can matter, but only when the surrounding structure supports that reading.

| What it is | What it is not |

|---|---|

| A possible exhaustion or absorption event after heavy downside pressure. | A guaranteed market bottom. |

| A context-dependent volume and price reading. | A standalone buy signal. |

| A clue that selling may be meeting stronger demand. | Proof that accumulation is already complete. |

| A sequence that needs later confirmation or invalidation. | A pattern that works the same way in every market or timeframe. |

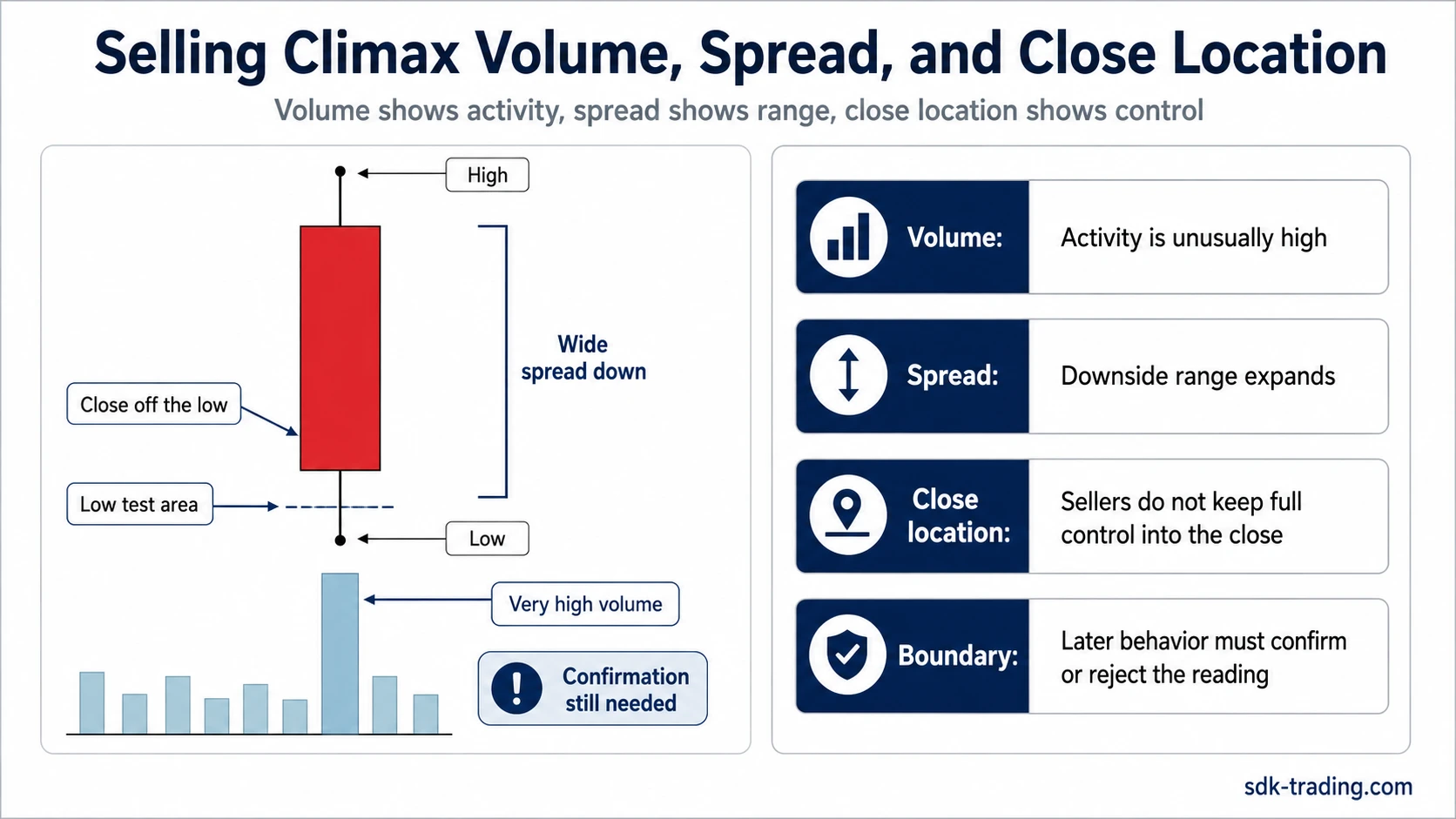

How Traders Read Volume, Spread, and Close Location

A selling climax is usually judged through the relationship between effort and result. Volume shows how much activity is present. Spread shows how far price moved during that activity. Close location shows whether sellers kept control into the end of the bar or whether the market rejected some of the downside progress.

| Observation | Possible read | Confirmation still needed |

|---|---|---|

| Very high volume on a downside move | Selling pressure may be extreme or meeting demand | Later bars should show whether downside continuation fails |

| Wide spread down | The move shows strong activity and urgency | Price must stop making efficient downside progress |

| Close off the low | Some selling may have been absorbed before the close | Subsequent behavior should hold or respond instead of collapsing again |

| Repeated heavy selling with limited progress | Supply may be losing efficiency | The market needs a later test, response, or failure of renewed selling |

None of these observations is enough alone. The reading becomes cleaner when heavy effort produces less downside result, then later selling attempts fail to extend the decline.

Selling Climax in Wyckoff / VSA Context

In the Wyckoff method, a selling climax often appears as an early event in a possible accumulation sequence. It marks the point where aggressive downside activity becomes visible, but the later automatic rally and secondary test are what help clarify whether supply has actually lost efficiency.

In VSA terms, the key question is effort versus result. If very high selling effort produces less downside progress afterward, the event becomes more meaningful. If later bars continue lower efficiently, the high-volume decline is still evidence of weakness rather than absorption.

Selling climax should also stay separate from broader volume climax patterns. It is one specific downside event inside that wider family, not the full framework for every volume climax.

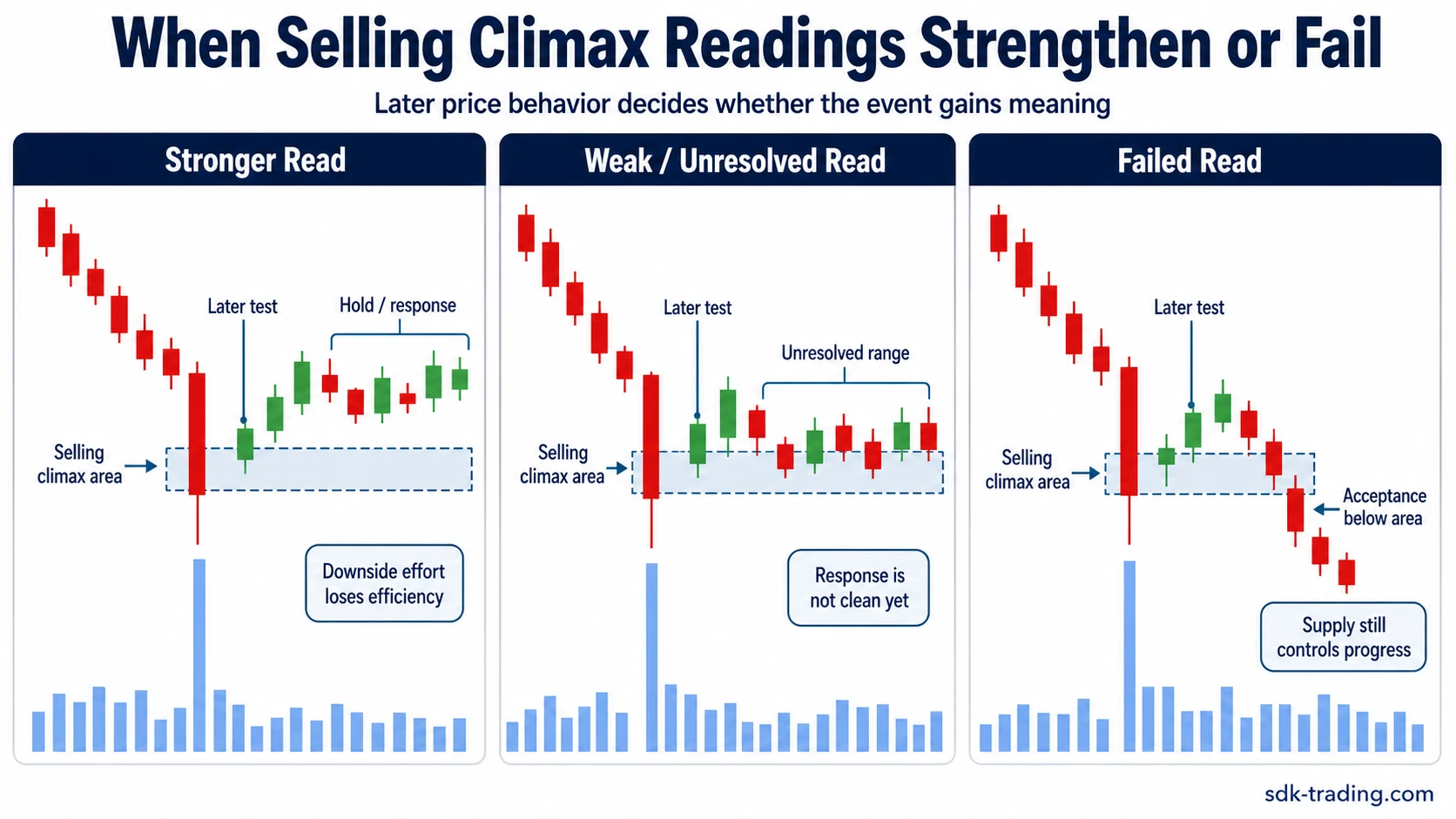

When the Selling-Climax Read Strengthens or Fails

The cleaner selling-climax case appears when heavy downside effort stops producing efficient downside result. Price may make a new low on exceptional activity, but the next push lower struggles, narrows, or attracts less effective selling pressure.

The reading fails when price accepts below the climax area, volume remains heavy on further declines, or every rally from the low area is quickly rejected. In that case, the original event was high activity, but not reliable evidence that supply had lost control.

Important limitation: A selling climax should not be treated as confirmation by itself. The event is only the observation phase. The interpretation depends on whether later price behavior shows reduced selling pressure, failed downside continuation, or renewed weakness below the climax area.

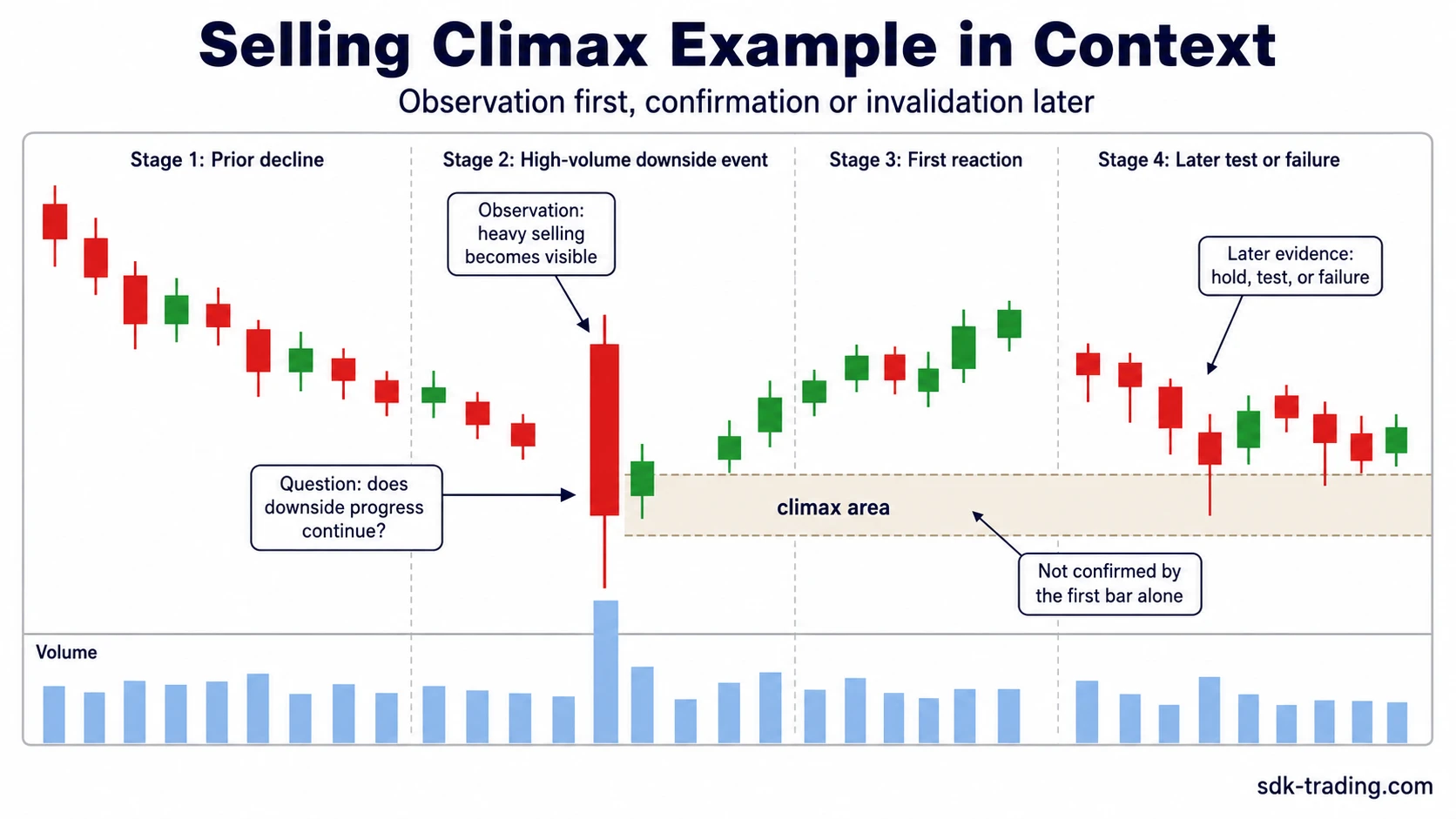

Selling Climax Example in Context

A market has been falling for several sessions, then prints a wide-range down bar on unusually high volume. The close finishes above the low, showing that sellers did not keep full control through the end of the bar.

That observation alone only shows that heavy selling failed to keep full downside control on that bar. The reading becomes stronger if later selling pressure fails to continue and price begins to hold or respond. If the next sequence breaks lower with renewed downside efficiency, the interpretation should be questioned.

Example reading: The event identifies the area to watch, not a completed conclusion. A later hold, weak retest, or renewed breakdown decides whether the original high-volume bar was more likely absorption, temporary pause, or continued supply.

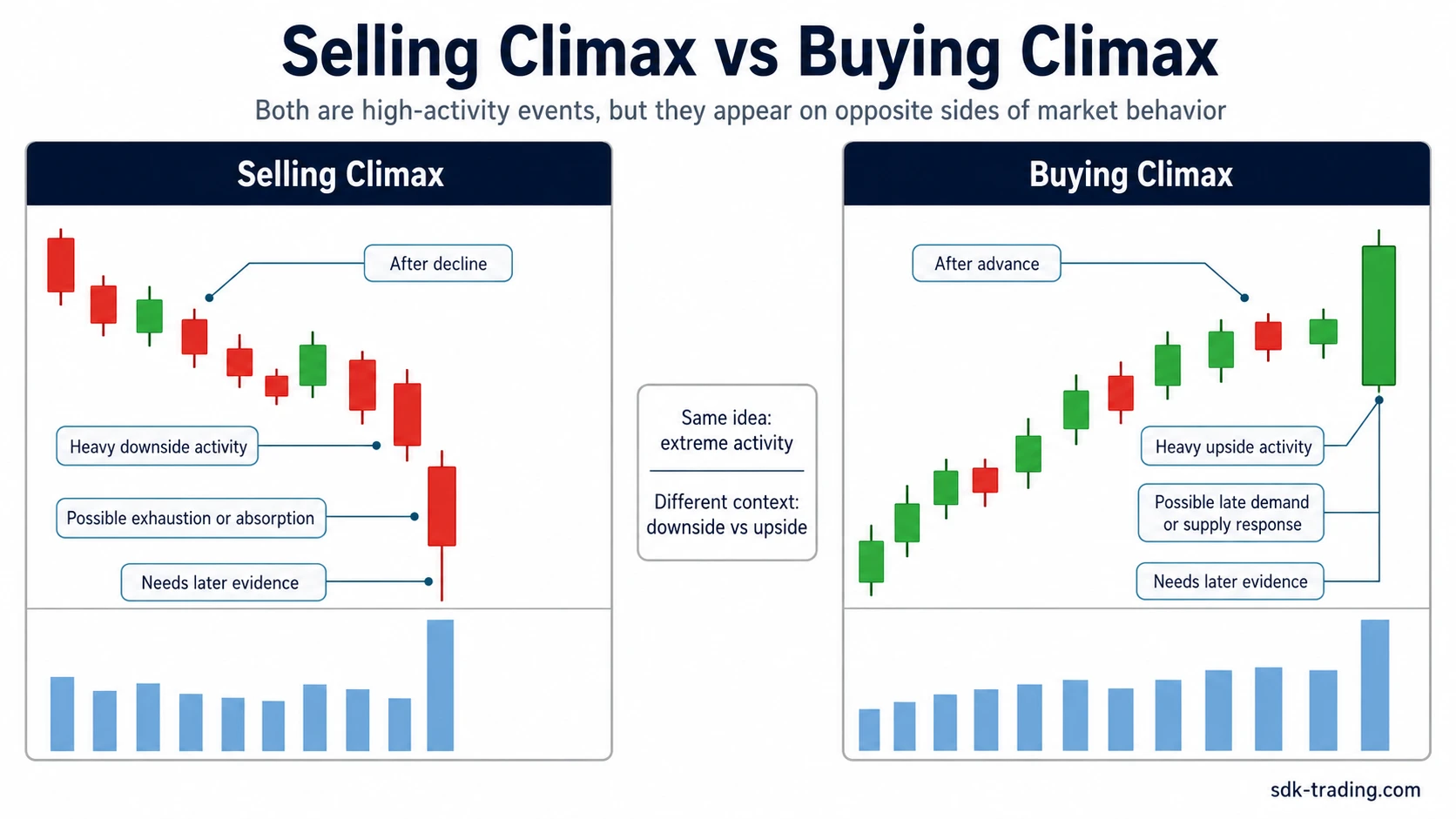

Selling Climax vs Buying Climax

A selling climax and a buying climax both describe extreme activity, but they appear on opposite sides of market behavior. A selling climax is associated with heavy downside pressure after a decline. A buying climax is associated with heavy upside activity after an advance.

| Concept | Typical context | Possible meaning | Main caution |

|---|---|---|---|

| Selling climax | After sustained downside pressure | Selling may be exhausting or meeting demand | It does not prove a reversal without later evidence |

| Buying climax | After sustained upside pressure | Demand may be late, excessive, or meeting supply | It does not prove distribution without later evidence |

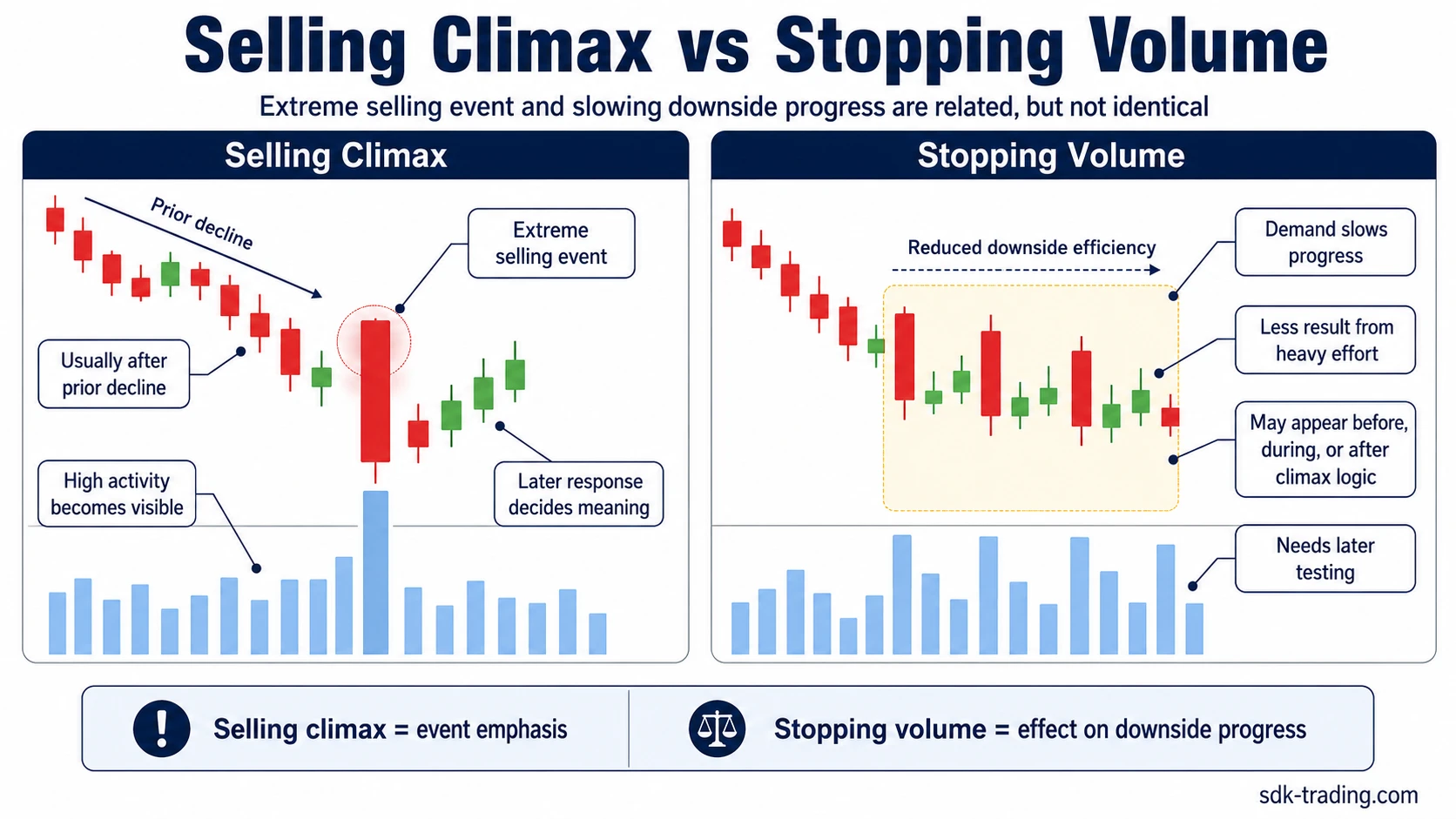

Selling Climax vs Stopping Volume

Selling climax describes an extreme selling event after a decline. Stopping volume describes the appearance of enough demand to slow or interrupt downside progress. The two can appear close together, but they are not identical: a selling climax names the intensity of the selling event, while stopping volume focuses on whether that selling is being absorbed strongly enough to change the immediate result.

A high-volume down bar can belong to a selling climax sequence, but not every high-volume pause is a selling climax. The difference depends on prior decline, range expansion, close location, and whether later behavior shows that renewed selling can no longer produce efficient downside progress.

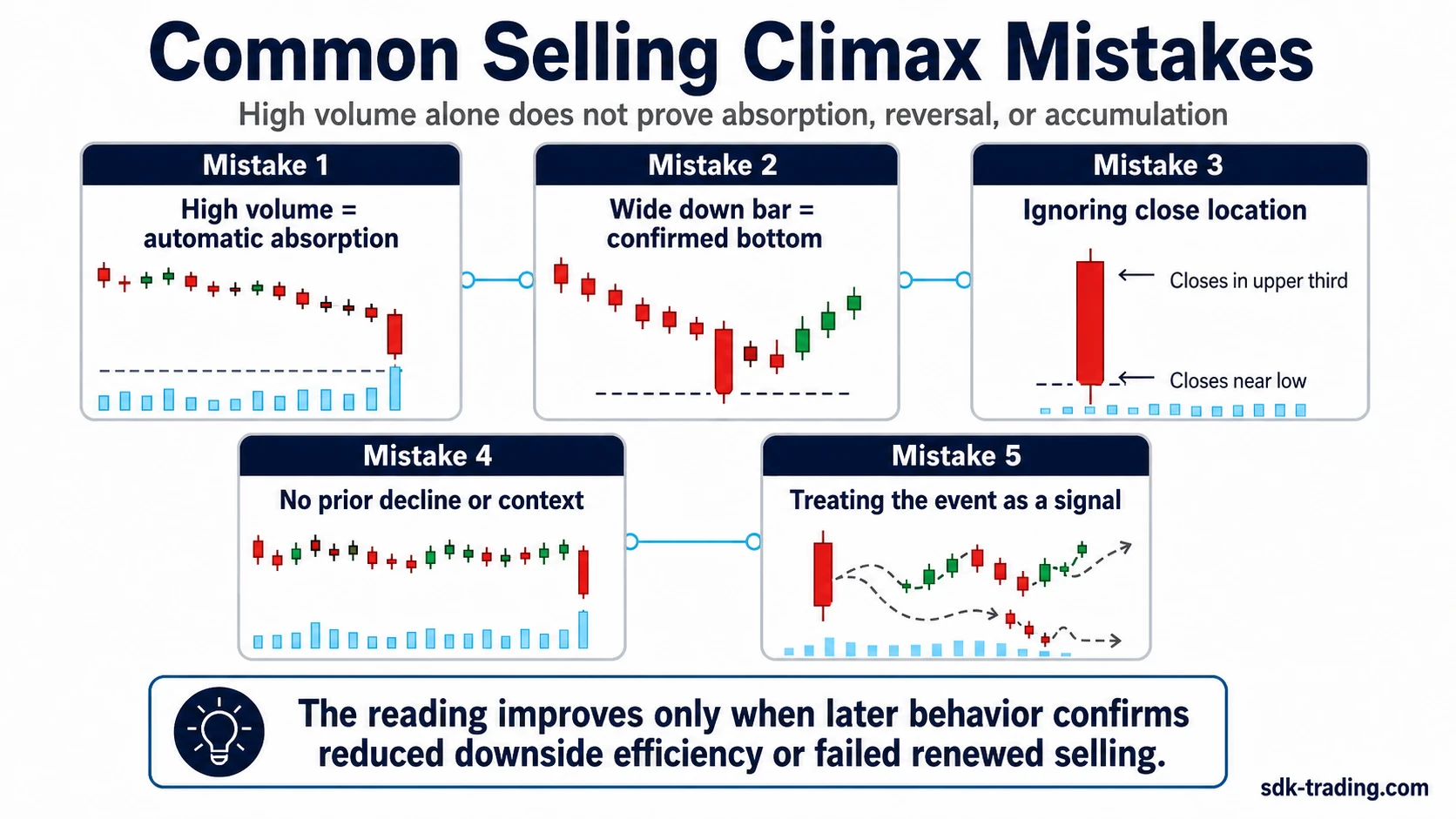

Common Selling Climax Mistakes

The most common mistakes come from reading one visible feature as proof. High volume alone does not prove absorption. A wide down bar alone does not prove a bottom. A close off the low matters only if later price behavior supports the interpretation.

- Reading high volume as automatic proof that stronger hands are absorbing supply.

- Treating a wide down bar as a confirmed bottom before later behavior appears.

- Ignoring the close location and focusing only on volume size.

- Calling every high-volume selloff a selling climax without checking prior context.

- Turning the concept into a trading setup instead of keeping it as a conditional market-reading event.

FAQ

What does a selling climax mean in VSA?

In VSA, a selling climax means heavy downside activity that may show exhaustion or absorption after sustained selling pressure. It is only a possible interpretation until later price and volume behavior confirms or rejects it.

When does a selling climax reading become stronger?

It becomes stronger when renewed selling fails to produce efficient downside progress, a later test holds above or near the climax area, and supply appears less effective than it was during the prior decline.

Does high volume always confirm a selling climax?

No. High volume only shows activity. The meaning depends on prior context, spread, close location, and what happens afterward. High volume can also appear during continued weakness.

How is selling climax different from stopping volume?

Stopping volume focuses on whether heavy selling is being absorbed strongly enough to slow or interrupt downside progress. A selling climax names the broader intensity of the downside selling event after a decline.

What invalidates a selling climax reading?

The reading weakens when the market continues lower with efficient downside movement after the supposed climax. If sellers keep control and price accepts lower levels, the climax interpretation is not supported.